Updated 2/25/26

Artesian Resources Corporation (ARTNA) delivers water, wastewater, and related services across the mid-Atlantic, with a strong presence in Delaware, Maryland, and Pennsylvania. The company has continued its steady operational rhythm into 2026, generating $111.8 million in revenue and $22.5 million in net income over the trailing twelve months. With a 3.61% dividend yield, a payout ratio of 55.85%, and a beta of just 0.36, ARTNA remains a dependable income vehicle for conservative investors. The dividend has continued its measured upward march, with the most recent quarterly payment of $0.314 per share representing another incremental step forward in a streak of consistent increases.

Recent Events

Artesian Resources has maintained its quiet, steady cadence heading into early 2026, continuing to invest in water and wastewater infrastructure across its mid-Atlantic service territory. The company has kept its focus on system reliability and regulatory compliance, both of which underpin its ability to seek and receive rate adjustments from state utility commissions. Capital spending remains elevated as Artesian works through a pipeline of infrastructure improvement projects across Delaware, Maryland, and Pennsylvania, consistent with the long-term investment posture that has defined its approach for years.

The broader regulated water utility sector has faced some attention from investors as interest rate expectations have shifted over the past several months. Rate-sensitive utilities like ARTNA saw some pressure as yields on fixed-income alternatives climbed, but the stock has largely stabilized and currently trades near the upper end of its 52-week range, sitting at $34.76 against a range of $29.97 to $36.19. That resilience reflects growing investor appreciation for the predictability of regulated utility earnings in an environment where economic uncertainty has picked up. Leadership under CEO Nicholle R. Taylor has maintained continuity in strategy, and the management team has continued to execute on the same infrastructure-first approach that characterized the prior administration.

Analyst coverage of ARTNA remains limited relative to larger utility peers, but the company’s operational consistency and dividend reliability have kept it on the radar of income-focused investors. With short interest at just 75,339 shares, there is no meaningful bearish pressure on the stock, which is consistent with the low-drama profile ARTNA tends to project.

Key Dividend Metrics

📈 Forward Dividend Yield: 3.61%

💵 Annual Dividend Rate: $1.24

🧾 Payout Ratio: 55.85%

📆 Most Recent Dividend Payment: $0.314 per share (February 13, 2026)

⛲ Dividend Growth: Consistent quarterly increases maintained through 2025 and into 2026

🔍 EPS (Trailing): $2.18

💰 Operating Cash Flow: $36,583,000

Dividend Overview

What stands out about ARTNA for income-focused investors is the combination of yield and reliability. At 3.61%, the dividend sits comfortably above what many regulated utility peers offer, and that yield is supported by a payout ratio of just 55.85%, which is meaningfully lower than the prior period’s ratio of nearly 60%. That improvement reflects earnings per share growth outpacing dividend increases, which is exactly the dynamic long-term income investors want to see. It means the company has more cushion to sustain and grow the payout even if earnings encounter modest pressure.

Artesian’s dividend is not a marketing tool or an afterthought. It is woven into how the company operates and communicates with shareholders. The quarterly payment has moved higher with each passing year, and the most recent payment of $0.314 per share, paid on February 13, 2026, extended that streak. The annual rate of $1.24 represents a clear step up from the $1.21 rate reported a year ago, giving income investors a tangible increase to point to.

Free cash flow remains negative at roughly negative $15.2 million over the trailing twelve months, which reflects the capital intensity of owning and upgrading water infrastructure. That figure is not a cause for alarm in the regulated utility context, where rate base investments are recoverable through future rate proceedings. The $36.6 million in operating cash flow provides the operational backbone that supports the dividend commitment, and the regulated revenue model ensures a high degree of visibility into future cash generation.

Dividend Growth and Safety

Artesian’s dividend history over the past several years tells a consistent story. Starting at $0.284 per quarter in mid-2023, the company has stepped the payout higher at each opportunity, reaching $0.290, then $0.296, then $0.301, then $0.307, then $0.314 per quarter as of the most recent payment in February 2026. That progression is not dramatic, but it is unbroken, and for dividend growth investors, an unbroken record of increases matters more than the size of any individual step.

The payout ratio of 55.85% gives the dividend a meaningful margin of safety. With EPS at $2.18 and the annual dividend at $1.24, there is $0.94 per share in retained earnings available to fund capital investment and debt service. That ratio has actually improved from prior levels, which reinforces the case that earnings are growing faster than the dividend, building coverage rather than eroding it. A stock like this isn’t designed to double your income in five years, but it is designed to pay you reliably through recessions, rate cycles, and market volatility, which is a different kind of value.

The beta of 0.36 reinforces the low-volatility character of the stock. It moves far less than the broader market on both the upside and downside, which is part of the appeal for investors who need income without the emotional toll of watching a position swing 20% in either direction. At a P/E of 15.94 and a price-to-book of 1.44, the valuation is not stretched, and investors are not paying a premium for the stability they are receiving.

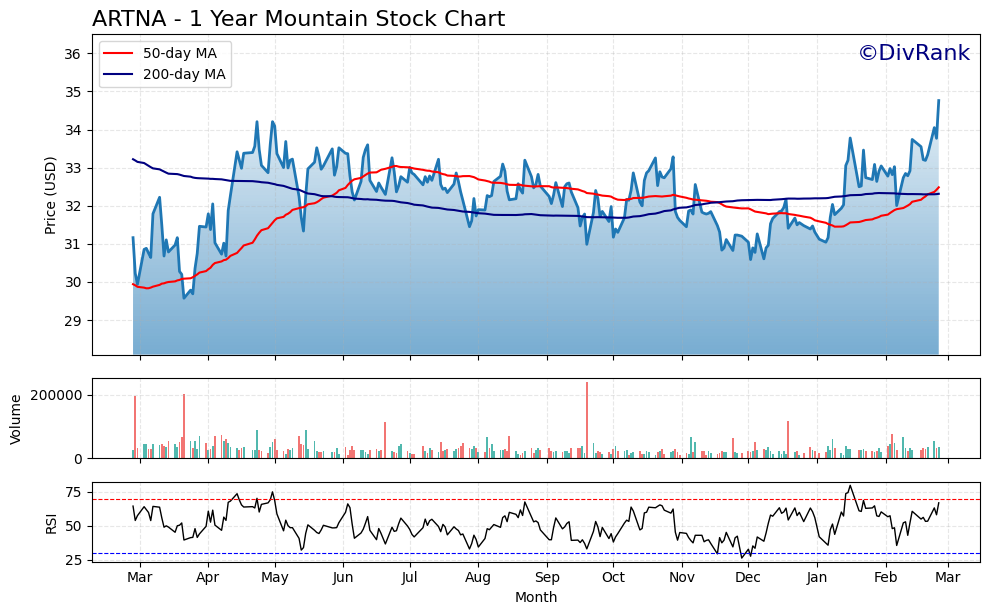

Chart Analysis

Artesian Resources has put together a constructive year of price action, climbing from a 52-week low of $29.57 to its current level of $34.76, a gain of roughly 17.5% from trough to peak. What makes the current setup particularly notable for income investors is that $34.76 also represents the 52-week high, meaning shares are trading at peak annual momentum with no recent overhead resistance to absorb. That kind of price behavior in a regulated water utility is not typical, and it reflects a market that has been actively re-rating the stock upward rather than simply drifting.

The moving average picture reinforces that constructive view. The 50-day moving average sits at $32.48 and the 200-day moving average at $32.31, and the current price of $34.76 clears both levels with room to spare. The 50-day has crossed above the 200-day, forming what technicians call a golden cross, a configuration that historically signals sustained upward trend momentum rather than a short-term bounce. The narrow gap between the two averages also tells you that the recovery off the 52-week low was orderly and broad-based rather than a sharp, unsustainable spike.

The Relative Strength Index reading of 66.86 places Artesian in firm upward momentum territory without yet crossing into the overbought zone above 70. That is a relatively comfortable position for a new or adding investor to be in. A reading in the high 60s suggests the stock has genuine buying pressure behind it while still leaving room for continued appreciation before the chart becomes technically stretched. Dividend investors who focus primarily on yield and payout sustainability should treat the RSI less as a timing trigger and more as a confirmation that the underlying price trend is healthy.

Taken together, the chart presents a straightforward picture for a long-term income investor. Artesian shares are in a confirmed uptrend, trading above both key moving averages, pressing against fresh 52-week highs, and carrying momentum that has not yet overheated. The primary risk the chart introduces is the absence of a nearby support cushion at current prices, since investors entering at or near the 52-week high accept some short-term drawdown risk if broader utility sector sentiment softens. For dividend-focused holders with a multi-year horizon, however, the technical backdrop is about as supportive as a small-cap regulated utility typically offers.

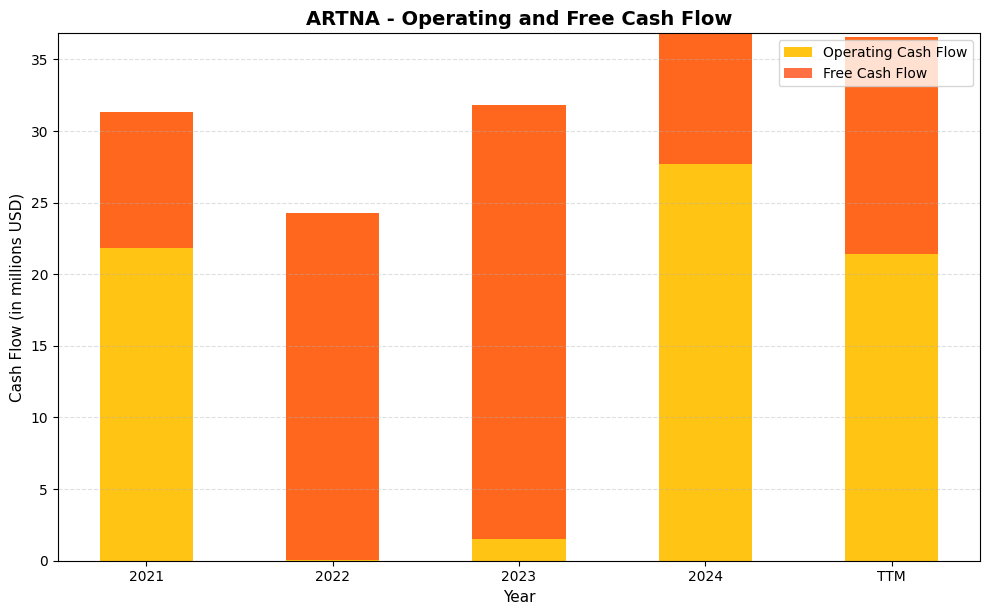

Cash Flow Statement

Artesian Resources generates a steady and growing stream of operating cash flow, rising from $31.3 million in 2021 to $36.8 million in 2024, with the trailing twelve months sitting at $36.6 million. That operational consistency is a meaningful signal for income investors, as it confirms the regulated water utility model is doing exactly what it should: converting rate-base revenue into reliable cash. Free cash flow, however, tells the other side of the story. Capital expenditures routinely outpace operating cash generation, leaving free cash flow deeply negative in every year shown, reaching a trough of negative $30.3 million in 2023 before recovering to negative $9.1 million in 2024. For a regulated utility, negative free cash flow is not inherently alarming, since infrastructure investment is both mandated and recoverable through the rate-setting process, but it does mean the dividend is not being funded from free cash flow in the traditional sense. Instead, Artesian relies on a combination of operating cash, debt issuance, and equity raises to fund both its capital program and its shareholder distributions, a financing structure that is standard across the water utility sector but one investors should monitor closely.

The trajectory over the four-year period reflects the reality of owning and operating regulated water infrastructure in a growing service territory. Capital spending has been elevated and lumpy, with 2023 representing the peak investment year, and the subsequent improvement in free cash flow in 2024 suggests the pace of spending moderated, at least temporarily. Operating cash flow has expanded by roughly 17 percent from 2021 to 2024, which is a constructive trend even if the absolute level remains insufficient to cover both capex and dividends on its own. For shareholders, the key consideration is whether rate case outcomes continue to allow Artesian to earn an adequate return on its growing rate base, since that regulatory compact is ultimately what transforms heavy capital spending into future earnings and cash flow growth. As long as the Delaware Public Service Commission and other state regulators remain supportive, the infrastructure investment cycle that pressures near-term free cash flow today should translate into the expanded earning power that supports continued dividend growth tomorrow.

Analyst Ratings

Formal analyst coverage of Artesian Resources remains limited, and no specific price targets or consensus ratings are currently available from the major research providers tracked in this report. That is not unusual for a small-cap regulated utility with a market capitalization of approximately $359 million. Companies of this size and profile tend to attract fewer Wall Street analysts than larger peers, which can actually work in the favor of patient investors who are willing to do their own work on a name that isn’t crowded with competing opinions.

Based on the company’s current financial profile, the stock appears reasonably valued at $34.76. A P/E of 15.94 on trailing earnings of $2.18 per share is not demanding for a regulated utility with a consistent dividend record and low earnings volatility. The price-to-book ratio of 1.44 reflects a modest premium to tangible equity, which is appropriate given the quality and predictability of the regulated revenue stream. Return on equity of 9.25% is solid for the sector and suggests management is generating adequate returns on the capital it deploys. Investors who follow the regulated water utility space have generally viewed ARTNA as a hold-to-accumulate name at prices in the low-to-mid thirties, with the dividend yield and stability being the primary return drivers rather than multiple expansion.

Earning Report Summary

Artesian Resources has continued to post consistent financial results through its most recent reporting periods, building on the strong 2024 performance that saw net income reach $20.4 million. The trailing twelve-month figures show further improvement, with net income rising to $22.5 million and EPS climbing to $2.18, up from $1.98 in the prior fiscal year. Revenue reached $111.8 million, representing continued growth from the $108 million posted for full-year 2024. These results reflect the cumulative benefit of prior rate increase approvals, steady customer growth across the company’s Delaware service territory, and contributions from its wastewater and non-utility service segments.

Margin Improvement and Operating Discipline

The profit margin of 20.16% is a meaningful improvement from the 18.9% reported in the prior period, and it suggests that revenue growth has outpaced the rise in operating expenses. Higher water sales, driven by rate adjustments and modest customer additions, have provided the top-line fuel while management has kept a disciplined hand on controllable costs. Supply, treatment, and labor costs have continued to rise, as they have across the industry, but Artesian’s regulated pricing mechanism allows it to recover these increases through the rate-setting process over time, which limits the long-term margin risk.

Capital Investment Continues at an Elevated Pace

Capital spending remains one of the defining features of Artesian’s financial story. The company continues to invest heavily in pipeline replacements, treatment facility upgrades, and system extensions, with capital expenditures running well above $45 million annually. That level of investment pressures free cash flow in the near term but builds the rate base that supports future earnings power. It is the kind of spending that regulators understand and reward over time, making it a feature of the business model rather than a cause for concern. Overall, the financial trajectory of Artesian heading into 2026 is one of steady, controlled progress, with improving earnings coverage of the dividend and a growing revenue base underpinning the outlook.

Management Team

Artesian Resources Corporation is led by Nicholle R. Taylor, who serves as Chief Executive Officer and President. She succeeded her aunt, Dian C. Taylor, who had guided the company since 1992, and brought with her more than three decades of experience within Artesian itself, having joined in 1991 and served in a range of executive roles including President of Artesian Water Company and Senior Vice President. Her familiarity with the operational, regulatory, and cultural dimensions of the business has supported a seamless leadership transition and maintained the continuity that long-term investors in a regulated utility tend to value highly.

The broader executive team reflects the same depth and stability. Joseph A. DiNunzio serves as Executive Vice President and Corporate Secretary, providing expertise in governance and regulatory compliance. David Spacht, the company’s Chief Financial Officer, oversees financial planning and capital markets strategy, and has been a consistent presence through multiple rate cycles and capital programs. John Thaeder manages day-to-day operations across the company’s service territory, while Jennifer Finch handles corporate finance and treasury functions. Pierre Anderson serves as Chief Information Officer, overseeing the technology infrastructure that supports billing, customer service, and system monitoring. Together, this team combines deep institutional knowledge with the functional expertise required to operate a capital-intensive, heavily regulated utility efficiently.

Valuation and Stock Performance

As of February 25, 2026, ARTNA is trading at $34.76 per share, within a 52-week range of $29.97 to $36.19. The stock is currently sitting near the upper portion of that range, a sign that investor sentiment toward the name has improved from the lows seen earlier in the past twelve months. The market capitalization stands at approximately $359 million, keeping ARTNA firmly in small-cap territory. The trailing P/E of 15.94 is actually lower than the 16.92 reported a year ago, reflecting earnings growth that has more than kept pace with the modest price appreciation in the stock. That is an encouraging dynamic for valuation-conscious investors.

The price-to-book ratio of 1.44 is consistent with prior periods, indicating that the stock continues to trade at a modest premium to its tangible equity base of $24.13 per share. That premium is well-supported by the company’s regulated revenue model, which provides strong earnings visibility and limits downside risk in a way that purely unregulated businesses cannot match. The dividend yield of 3.61% remains competitive within the regulated water utility space and represents a meaningful income return at current prices. With a beta of 0.36, the stock continues to offer the low-volatility profile that conservative income investors seek, and its current positioning near the top of its 52-week range suggests the market is beginning to reflect the improvement in underlying earnings more fully.

Risks and Considerations

Artesian operates in a capital-intensive environment that requires ongoing and substantial investment in physical infrastructure. Capital expenditures have run well above operating cash generation in recent periods, pushing free cash flow to negative $15.2 million over the trailing twelve months. While this pattern is characteristic of water utilities and is ultimately recoverable through the regulatory rate-setting process, it does require consistent access to debt and equity markets to bridge the funding gap. If credit conditions tighten or the cost of capital rises meaningfully, the company’s ability to fund its investment program on favorable terms could be pressured.

The regulatory environment is both a strength and a constraint. Artesian’s earnings depend on approvals from state utility commissions in Delaware, Maryland, and Pennsylvania to raise rates in line with its growing cost base and rate base investments. There is no guarantee that future rate filings will be approved on the timeline or at the level the company requests, and any unfavorable regulatory outcome could weigh on near-term earnings and cash flow. The lag between when capital is invested and when it earns a return in rates is a structural feature of the business that investors need to understand and accept.

Geographic concentration remains a consideration for long-term investors. The vast majority of Artesian’s revenue comes from its Delaware service territory, which means regional economic conditions, population trends, and environmental factors have an outsized influence on the company’s results. A prolonged period of slow growth or adverse weather patterns affecting water supply and demand in that region could affect revenue more meaningfully than would be the case for a more geographically diversified utility. Return on equity of 9.25%, while solid for the sector, also reflects the bounded nature of returns in a regulated model, where outsized profitability is structurally constrained by the rate-setting process.

Final Thoughts

Artesian Resources enters 2026 in a position of quiet strength. Earnings have grown, the dividend has continued its measured upward march, the payout ratio has actually improved, and the stock has recovered from its earlier 52-week lows to trade near the top of its range. None of this is dramatic, and that is precisely the point. ARTNA is built to be undramatic, to show up reliably, to invest consistently in its infrastructure, and to return a growing stream of income to its shareholders year after year.

The improvement in net income from $20.4 million to $22.5 million over the past year, the expansion of the profit margin to 20.16%, and the continued dividend growth from $1.21 to $1.24 annually are all signs that the business is executing well. The lower payout ratio of 55.85% relative to prior periods adds a layer of safety that income investors should find reassuring. The management team under Nicholle R. Taylor has maintained the operational and cultural continuity that has defined Artesian for decades.

The trade-offs are real. Negative free cash flow, regulatory dependency, and a concentrated geographic footprint all deserve a place in any honest assessment of the stock. But for investors who prioritize income stability, low volatility, and steady dividend growth over high-octane returns, Artesian continues to deliver exactly what it promises, and at a valuation that does not ask investors to pay an unreasonable premium for that reliability.