Updated 2/25/26

This Pennsylvania-based company has carved out a focused and profitable niche in commercial ceiling systems and architectural products, with a strong presence in hospitals, schools, and office buildings across the country. Armstrong World Industries (AWI) isn’t trying to reinvent the wheel—it’s executing a clear strategy built on steady demand, high-margin offerings, and operational discipline. Over the past year, the company delivered $1.62 billion in revenue and generated $355.5 million in operating cash flow, translating into a solid $205.9 million in free cash flow. With a payout ratio under 18% and a dividend that’s both well-covered and quietly growing, Armstrong offers a level of reliability that’s increasingly rare. Even after the stock’s run from last year’s lows, the trailing P/E near 25 reflects a market that continues to reward the company’s durable earnings power. It’s not flashy, but it’s consistent, efficient, and built for long-term investors who value durable cash flow over speculation.

🧾 Key Dividend Metrics

📈 Forward Yield: 0.75%

💰 Annual Dividend: $1.29 per share

📆 Latest Payout Date: November 2025

🔄 5-Year Average Yield: 1.03%

📊 Payout Ratio: 17.68%

📉 Trailing Yield: 0.75%

📅 Most Recent Ex-Dividend Date: November 6, 2025

Recent Events

Armstrong World Industries continues to execute at a high level heading into 2026. The company delivered full-year revenue of $1.62 billion, a meaningful step up from prior-year levels, while net income reached $308.7 million and diluted earnings per share came in at $6.97. Those figures represent continued expansion of the company’s core commercial ceiling and architectural specialties business, underscoring that demand in hospitals, educational facilities, and renovation-driven commercial spaces remains firm. Operating cash flow surged to $355.5 million on a trailing basis, a significant improvement that signals the business is converting its growth into real cash with increasing efficiency.

On the dividend front, AWI raised its quarterly payment to $0.339 per share in the November 2025 distribution, up from the $0.308 it had held steady through most of the year. That brings the annualized dividend to $1.29 per share and continues the company’s pattern of measured, consistent increases. The raise followed similar step-ups in late 2023 and late 2024, reinforcing a pattern of annual fourth-quarter increases that dividend growth investors can plan around. Return on equity stands at an impressive 37.24%, and the company’s 19.05% profit margin reflects the pricing power and operational efficiency that have become defining characteristics of the Armstrong model.

Dividend Overview

Armstrong’s dividend yield, sitting just under 0.8% at the current price of $172.21, isn’t designed to compete with high-yield income plays. This is a dividend you own for growth and consistency, not for immediate income replacement. The annualized rate of $1.29 per share is well-supported by earnings, with the payout ratio coming in at just 17.68% against trailing EPS of $6.97. That gap between what Armstrong earns and what it pays out is substantial, and it gives the company a wide buffer to sustain and grow the dividend even if earnings soften in a given year.

The payment schedule remains predictable and quarterly, with the most recent distribution of $0.339 per share paid in November 2025 following an ex-dividend date of November 6. Investors who value income visibility will find AWI’s rhythm straightforward and reliable. The company has not missed or reduced a payment in recent history, and the trajectory of increases, while modest in dollar terms, reflects a management team that takes the dividend seriously as a component of total shareholder return.

Dividend Growth and Safety

The safety profile of Armstrong’s dividend is among the strongest in the building products space. The company is funding its payout entirely from operating earnings, with no reliance on debt issuance or asset sales to support distributions. At $1.29 annually, AWI spends roughly $56 million per year to cover its dividend obligation. Against $205.9 million in free cash flow, that represents a coverage ratio of nearly 3.7 times, leaving enormous room for capital allocation flexibility.

The growth trajectory is equally encouraging. Starting from $0.254 per quarter in early 2023, Armstrong has raised its quarterly payment twice in that span, reaching $0.308 in late 2024 and then $0.339 in November 2025. That represents roughly a 34% cumulative increase in the quarterly payout over approximately two and a half years, compounding at a pace well ahead of inflation. With a return on equity of 37.24% and return on assets above 10%, the underlying business is generating returns that make continued dividend growth a natural byproduct of normal operations rather than a financial stretch.

Share repurchases continue alongside the dividend, reducing the share count and providing an additional lever for per-share dividend growth even when the absolute dollar amount of payout remains stable. The combination of disciplined buybacks and a sub-18% payout ratio means AWI has meaningful room to accelerate dividend increases if management chooses to do so, and the financial capacity to sustain them through a downturn if conditions change.

Chart Analysis

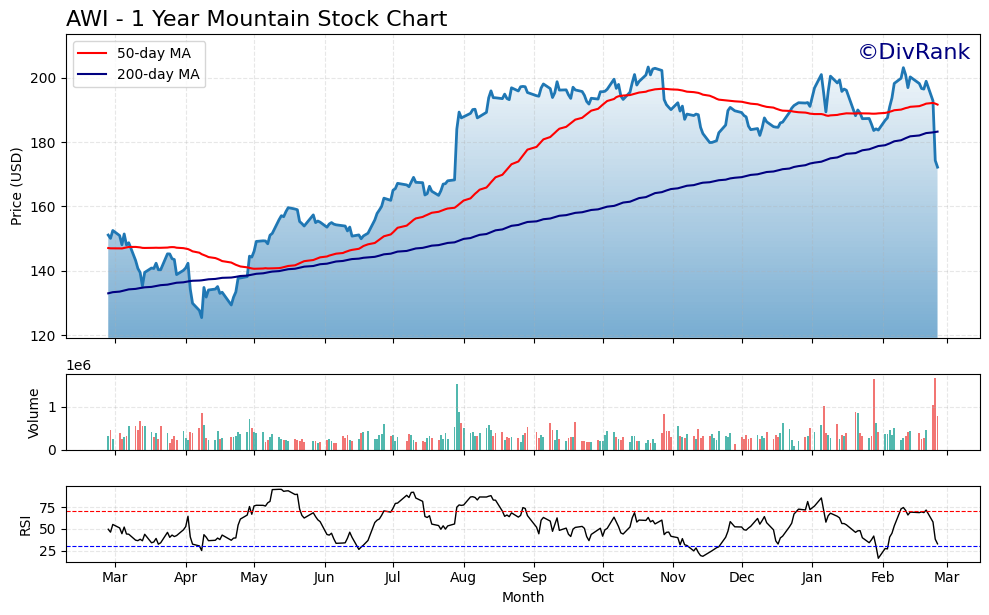

Armstrong World Industries has had an eventful twelve months on the price chart, running from a 52-week low of $125.41 all the way up to a high of $203.35 before pulling back sharply to the current level of $172.21. That round trip tells an important story: the stock attracted genuine buying interest during its advance, nearly doubling off its lows, but the retreat from the peak has been steep enough to erase a meaningful portion of those gains. At roughly 15% below the 52-week high, AWI is now trading in pullback territory rather than breakdown territory, a distinction that matters for income investors trying to separate temporary weakness from something more structurally worrying.

The moving average picture is mixed but not alarming. The 50-day moving average sits at $191.67 and the 200-day at $183.26, and AWI is currently trading below both of those levels, which confirms that near-term momentum has shifted against buyers. What partially offsets that concern is the fact that the 50-day remains above the 200-day, a configuration commonly called a golden cross, which signals that the longer-term trend established over the past year still carries a bullish bias. The risk is that a continued decline could eventually drag the 50-day back toward or below the 200-day, converting that constructive setup into a more cautious one. For now, the stock is in the uncomfortable but not uncommon position of a short-term downtrend living inside a longer-term uptrend.

The RSI reading of 32.8 places AWI right on the doorstep of oversold territory, which is conventionally defined as a reading below 30. Momentum has clearly deteriorated from the levels that supported the stock’s advance toward $203, and the current reading suggests sellers have been firmly in control during the recent decline. However, an RSI near 30 also tends to reflect a point where selling pressure becomes exhausted, and patient investors have historically found that entries made at these momentum extremes often look quite reasonable in hindsight, particularly in quality compounders with durable business models.

For dividend investors, the current setup presents an interesting tension. The pullback has improved the prospective yield and entry valuation relative to where AWI was trading just a few months ago, and the oversold RSI suggests the worst of the near-term selling may be running its course. At the same time, trading below both key moving averages means the technical backdrop has not yet confirmed a bottom, and chasing a recovery before price reclaims at least the 200-day moving average around $183 carries real timing risk. Scaling into a position at current levels while watching for a stabilization signal above $183 is a reasonable approach for long-term income investors who prioritize total return alongside dividend growth.

Cash Flow Statement

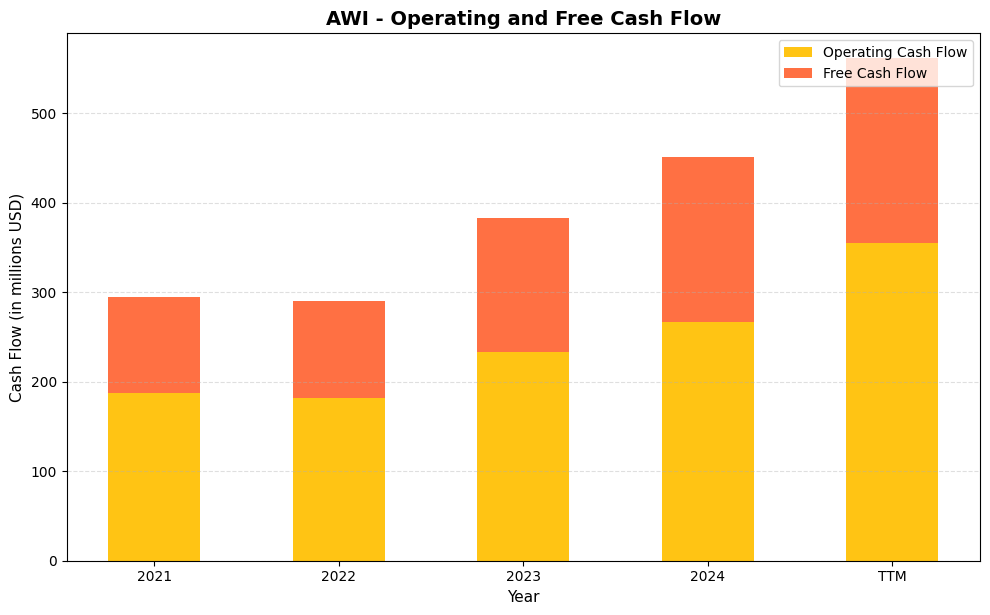

Armstrong World Industries has built an increasingly compelling cash flow profile over the past several years, one that speaks directly to dividend sustainability. Operating cash flow expanded from $187.2 million in 2021 to $266.8 million in 2024, and the trailing twelve months figure of $355.5 million suggests the business is accelerating rather than plateauing. Free cash flow tells a similarly encouraging story, climbing from $107.4 million in 2021 to $184.0 million in 2024 and reaching $205.9 million on a TTM basis. For a dividend investor, that trajectory matters enormously, because dividends are ultimately paid from cash, not accounting earnings. With free cash flow now comfortably exceeding the company’s annual dividend obligation, AWI carries meaningful coverage that leaves room for continued payout growth without straining the balance sheet.

The multi-year trend reveals something more interesting than raw growth alone, which is genuine improvement in capital efficiency. From 2021 to 2024, operating cash flow grew by approximately 42% while free cash flow grew by nearly 71%, meaning capital expenditures consumed a shrinking share of operating cash generation over time. The TTM free cash flow conversion rate reinforces this point, as AWI is now retaining a larger proportion of each operating dollar after reinvestment than it was three years ago. For shareholders, that dynamic translates into a management team that appears disciplined about capital allocation, generating surplus cash that can fund dividends, share repurchases, or acquisitions without relying on external financing. The consistent upward slope across every single year in this dataset is the kind of pattern that income investors should find genuinely reassuring.

Analyst Ratings

The analyst community holds a constructive view on Armstrong World Industries, with a consensus rating of Buy across the ten firms covering the stock. The mean price target sits at $209.30, representing upside of approximately 21.5% from the current price of $172.21. The range of targets is fairly wide, from a low of $185.00 to a high of $240.00, reflecting a spread of views on how quickly the commercial construction and renovation cycle will accelerate. Even at the low end of the target range, analysts see meaningful appreciation from current levels, which suggests the broader sell-side community views the recent pullback from the 52-week high of $206.08 as an opportunity rather than a sign of fundamental deterioration.

The bullish case centers on Armstrong’s pricing power, its dominant position in commercial acoustic ceiling systems, and the structural tailwind from ongoing renovation activity in healthcare and education facilities. Bears, to the extent they exist in this coverage universe, point to valuation as the primary concern rather than any operational weakness. With the stock trading at a P/E of 24.71 and a price-to-book of 8.21, some analysts prefer to wait for a clearer re-rating catalyst before upgrading. The gap between the current price and the consensus target of $209.30 suggests that, on balance, the analyst community believes the fundamentals justify a higher multiple than the market is currently assigning.

Earning Report Summary

Armstrong World Industries delivered a strong full-year performance for the period reflected in the most recent trailing twelve-month financials, building on the momentum established in prior years and demonstrating that the company’s commercial focus continues to generate reliable growth.

Revenue and Earnings Growth

Full-year revenue reached $1.62 billion, a meaningful increase over the prior year’s $1.45 billion and a continuation of the multi-year growth trend in Armstrong’s core commercial segments. Net income came in at $308.7 million, up from $264.9 million in the prior year, reflecting not just higher revenues but also effective cost management and a business model that scales well. Diluted earnings per share reached $6.97, compared to $6.02 in the prior year, representing growth of approximately 16% and underscoring the contribution of ongoing share repurchases to per-share results.

Margins and Operational Efficiency

The profit margin expanded to 19.05%, up from approximately 18% the prior year, a sign that Armstrong is not just growing the top line but doing so with improving efficiency. Operating cash flow of $355.5 million was a particularly strong result, meaningfully above the prior year’s $266.8 million. That kind of cash flow acceleration, in a business already known for its cash generation, reinforces the durability of the company’s earnings quality and its ability to self-fund growth, dividends, and buybacks simultaneously. The results confirm that Armstrong’s focused strategy in commercial ceiling systems and architectural specialties continues to be the right approach for generating consistent, compounding returns.

Management Team

The team steering Armstrong World Industries brings a grounded approach to leadership. Vic Grizzle, who has served as CEO since 2016, has guided the company through a focused evolution, streamlining operations and doubling down on higher-margin product lines. Under his direction, Armstrong has moved away from lower-growth areas and leaned into its strengths in commercial ceiling systems and architectural specialties. The results speak for themselves: revenue has grown steadily, margins have expanded, and the dividend has increased consistently under his tenure.

Brian MacNeal, the CFO, has played a key role in maintaining a strong financial foundation. His focus on cash flow and capital discipline shows up clearly in the company’s ability to fund innovation while still returning capital to shareholders through both dividends and buybacks. Together, the leadership team emphasizes sustainable growth over chasing trends. Their steady communication with the investment community, clarity in strategy, and emphasis on long-term execution give confidence that they’re managing not just for the next quarter but for the next decade. They don’t chase the spotlight. They stick to strategy, execute consistently, and deliver results with minimal drama. That’s a quality not often celebrated, but one that tends to win over time.

Valuation and Stock Performance

AWI shares are currently trading at $172.21, sitting well below the 52-week high of $206.08 but considerably above the year’s low of $122.37. The stock has traveled a wide range over the past twelve months, and the current price represents a meaningful discount to where it was trading at its peak, which may attract investors who were waiting for a better entry point into a business with this quality of fundamentals.

From a valuation perspective, the trailing P/E of 24.71 reflects a moderate premium for a company with consistent margins, strong cash generation, and a dominant market position in commercial acoustics. The price-to-book ratio of 8.21 is elevated in absolute terms, but it is justified by a return on equity of 37.24% and a business model that requires limited tangible capital to generate high returns. Companies that earn this much on their equity base typically deserve to trade at a premium to book value.

The market cap of approximately $7.45 billion puts AWI in a comfortable mid-cap range where institutional ownership is deep and liquidity is solid. The mean analyst price target of $209.30 implies roughly 21.5% upside from current levels, suggesting the current price may represent an attractive entry for investors with a twelve-to-eighteen month horizon. The gap between the current price and both the 52-week high and the analyst consensus target is wide enough to provide a reasonable margin of safety for new positions, particularly given the strength of the underlying cash flow profile.

Risks and Considerations

Armstrong’s business is tightly linked to non-residential construction and renovation activity, which means any sustained slowdown in commercial building, driven by elevated interest rates, tighter credit conditions, or a pullback in corporate capital expenditure, could weigh on demand for ceiling systems and architectural products. Hospitals and schools provide some insulation, but the office segment remains sensitive to broader economic and structural shifts, particularly as hybrid work arrangements continue to reshape demand for traditional commercial interiors.

Input cost inflation remains a consideration even as supply chains have normalized from their pandemic-era disruptions. Armstrong uses materials including mineral fiber, steel, and other industrial inputs, and if commodity costs rise faster than the company’s ability to implement price increases, margin compression could follow. The company has historically managed this well, but it’s a recurring variable that investors should monitor, especially in inflationary environments.

The company’s tight focus on a specific niche within building products is a double-edged quality. The concentration that drives operational efficiency and pricing power also limits diversification. If competitors introduce disruptive alternatives to traditional acoustic ceiling systems, or if architectural preferences shift materially toward open-ceiling designs, Armstrong would need to adapt its product portfolio and go-to-market strategy more quickly than its current model anticipates.

The long-term trajectory of office space utilization also bears watching. Continued growth in remote and hybrid work could dampen the pace of commercial renovation projects, which are a meaningful driver of Armstrong’s recurring demand. While healthcare and education remain structurally stable end markets, they may not fully offset a prolonged softening in the office segment if corporate tenants delay or reduce interior renovation programs.

Finally, at a P/E above 24 and a price-to-book near 8, the current valuation leaves limited room for disappointment. A miss on earnings, a reduction in guidance, or a broader market derating of industrial names could result in a swift pullback from current levels, even if the underlying business remains healthy. Investors entering at current prices should be comfortable with that valuation risk as part of the overall thesis.

Final Thoughts

Armstrong World Industries has carved out a niche that may not be glamorous, but it’s dependable. The company runs a focused, high-margin business with consistent execution and a smart capital return strategy. Management doesn’t overreach, and that measured approach is reflected in the balance sheet, the operating results, and the disciplined pattern of dividend increases that have compounded quietly but meaningfully over the past several years.

The most recent dividend raise to $0.339 per quarter, announced in late 2025, continues a pattern of annual step-ups that have lifted the quarterly payment by roughly 34% since early 2023. With a payout ratio below 18% and free cash flow of $205.9 million covering the annual dividend obligation nearly four times over, the safety margin behind that growing income stream is genuinely impressive. Revenue of $1.62 billion, net income of $308.7 million, and operating cash flow of $355.5 million all represent the strongest results in the company’s recent history.

The stock’s pullback from its 52-week high of $206.08 to the current $172.21 brings it closer to the range where the fundamentals and the valuation feel better aligned. The consensus analyst price target of $209.30 suggests meaningful upside from here, and the underlying business quality supports a patient, long-term hold for investors who prioritize durable cash flow and growing income over short-term price momentum.

There are risks, no doubt. Slower construction activity, inflationary pressures, and long-term shifts in commercial real estate all carry weight. But Armstrong has been navigating these kinds of cycles for decades. It knows its space, and it sticks to its strengths. In a market filled with short-term promises, Armstrong keeps things simple: execute, generate cash, return capital, and repeat. For investors who appreciate that kind of straightforward model, it’s a company that earns its place without needing the spotlight.