Updated 2/25/26

Apple Inc. (AAPL) remains one of the most financially formidable companies on the planet, with a market cap now exceeding $4 trillion and a continued track record of disciplined capital allocation. Revenue has climbed to $435.6 billion over the trailing twelve months, and free cash flow of $106.3 billion gives the company enormous flexibility to grow its dividend, repurchase shares, and invest in the next generation of products and services. The stock trades at a forward P/E of 34.49, reflecting the premium investors continue to assign to Apple’s brand, ecosystem, and services trajectory. With 41 analysts covering the name and a consensus buy rating, the street remains broadly constructive on the story heading into 2026.

Recent Events

Apple has continued to push deeper into artificial intelligence in early 2026, expanding the rollout of Apple Intelligence features across additional languages and regions following its initial U.S. launch. The broader international availability of these AI capabilities has been a key focus for management, with Tim Cook signaling that this expansion is central to driving the next hardware upgrade cycle. Siri’s continued evolution and tighter integration with third-party applications have kept Apple’s AI narrative in the headlines, even as the company faces questions about whether it is keeping pace with competitors in the space.

On the product front, Apple has maintained its cadence of iterative innovation across its core hardware lines. The services segment continues to be the standout growth story, with the App Store, iCloud, Apple TV+, and Apple Pay collectively generating a rising share of overall revenue at margins that are substantially higher than the hardware business. That shift in revenue mix is a meaningful tailwind for profitability over time.

The company also continues to face scrutiny from regulators on multiple fronts. Antitrust investigations into App Store practices remain ongoing in both the United States and Europe, and any adverse rulings could require structural changes to how Apple monetizes its platform. Management has been navigating these challenges carefully, though the uncertainty around outcomes adds a layer of complexity to the longer-term outlook.

Key Dividend Metrics

🍏 Forward Yield: 0.38%

💰 Annual Dividend Rate: $1.04 per share

📈 5-Year Average Yield: 0.57%

📆 Dividend Growth Streak: 13 years and counting

🔁 Payout Ratio: 13.04%

🚀 Free Cash Flow (ttm): $106.3B

💵 Operating Cash Flow (ttm): $135.5B

These numbers don’t scream high yield, but they signal strength, flexibility, and considerable room to grow. That’s precisely the kind of profile that earns attention from serious dividend growth investors.

Dividend Overview

At 0.38%, Apple’s dividend yield is firmly in low-yield territory, and there is no point pretending otherwise. Investors seeking immediate income from a high-yield position will not find it here. But yield alone is a poor framework for evaluating Apple as a dividend holding, and the broader picture tells a more compelling story.

The payout ratio of 13.04% is the number that really matters for dividend investors. At that level, Apple is barely scratching the surface of what it could theoretically pay. The company generates $135.5 billion in operating cash flow annually, and the total dividend obligation is a small fraction of that figure. There is no financial stress in this dividend, and there hasn’t been for years.

Apple raised its quarterly dividend from $0.25 to $0.26 per share in May 2025, bringing the annualized rate to $1.04. That increase continued the company’s unbroken streak of annual raises dating back to the dividend’s reinstatement in 2012. Management has been deliberate and consistent in how it approaches these increases, favoring steady, sustainable growth over large one-time jumps that could create future obligations in a more difficult environment.

The share buyback program remains a critical part of the total return equation for Apple shareholders. By steadily reducing the share count over many years, Apple amplifies earnings per share and dividend coverage per share in ways that don’t always get the attention they deserve. It is a slow-moving but powerful form of capital return that compounds meaningfully over a long holding period.

Dividend Growth and Safety

Apple’s dividend growth record is now 13 years deep, with the quarterly payment rising from $0.24 per share in 2023 to $0.25 in May 2024 and then to $0.26 in May 2025. That steady upward progression reflects a management team that takes the dividend seriously as a component of shareholder return, even if the yield itself remains modest relative to the broader income investing universe.

The safety profile of this dividend is about as strong as it gets. A payout ratio of 13.04% means Apple is retaining the vast majority of its earnings and cash flow for reinvestment and buybacks. Even in a scenario where earnings declined substantially, the dividend would remain well covered. The company generated $106.3 billion in free cash flow over the trailing twelve months, against a total annual dividend obligation that represents a small single-digit percentage of that figure.

Return on equity of 152.02% and return on assets of 24.38% reinforce the picture of a business that converts capital into profit with extraordinary efficiency. A profit margin of 27.04% on $435.6 billion in revenue is a remarkable achievement at Apple’s scale, and it underlies the durability of the cash flows that support the dividend. The most recent ex-dividend date was February 9, 2026, with payment on February 13, continuing Apple’s reliable quarterly cadence that makes reinvestment planning straightforward for long-term holders.

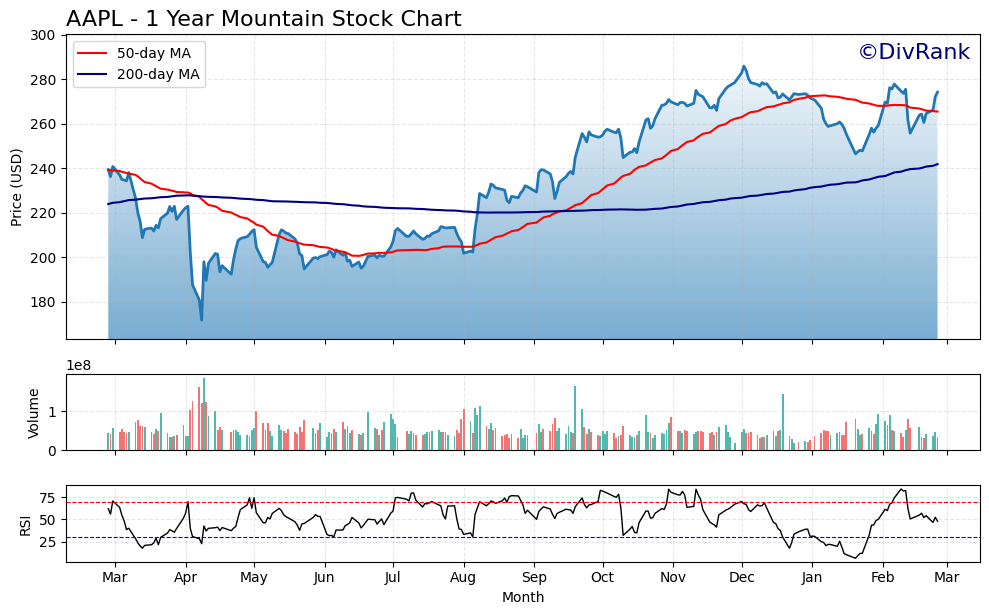

Chart Analysis

Apple’s chart tells a compelling recovery story over the past twelve months. Shares have surged 59.74% off the 52-week low of $171.67, a move that reflects a decisive shift in market sentiment toward the stock after what was a punishing drawdown period. At the current price of $274.23, AAPL sits just 4.09% below its 52-week high of $285.92, meaning the stock has reclaimed the vast majority of lost ground and is knocking on the door of fresh highs. For dividend investors, that kind of price recovery matters because it signals underlying business confidence and reduces the risk of capital impairment that can undermine a long-term income position.

The moving average picture reinforces the bullish trend. AAPL is trading above both its 50-day moving average of $265.50 and its 200-day moving average of $241.85, and critically, the 50-day has crossed above the 200-day to form what technicians call a golden cross. This configuration is one of the more reliable signals that a medium-term uptrend has taken hold and has the longer-term trend behind it. The spread between the current price and the 200-day average is roughly $32, or about 13%, which suggests the trend has meaningful momentum without being so extended that a reversion would immediately threaten the broader structure.

Momentum, as measured by the 14-day Relative Strength Index, is sitting at 48.16, which places AAPL squarely in neutral territory. The stock is neither overbought nor oversold at this reading, which is actually a constructive setup from an entry standpoint. An RSI in the high 40s following a strong price recovery often indicates that early speculative enthusiasm has cooled and the stock is consolidating gains in a healthy way, rather than being stretched into a condition that tends to precede sharp pullbacks.

For dividend investors, the technical picture at these levels is generally supportive. The combination of a confirmed golden cross, a price close to 52-week highs, and a neutral RSI suggests that the path of least resistance remains upward while near-term risk of an overextended correction appears limited. Dividend investors are rarely served well by trying to time bottoms perfectly, and a stock trending above both key moving averages with room to grow toward new highs provides a reasonable backdrop for initiating or adding to an income position.

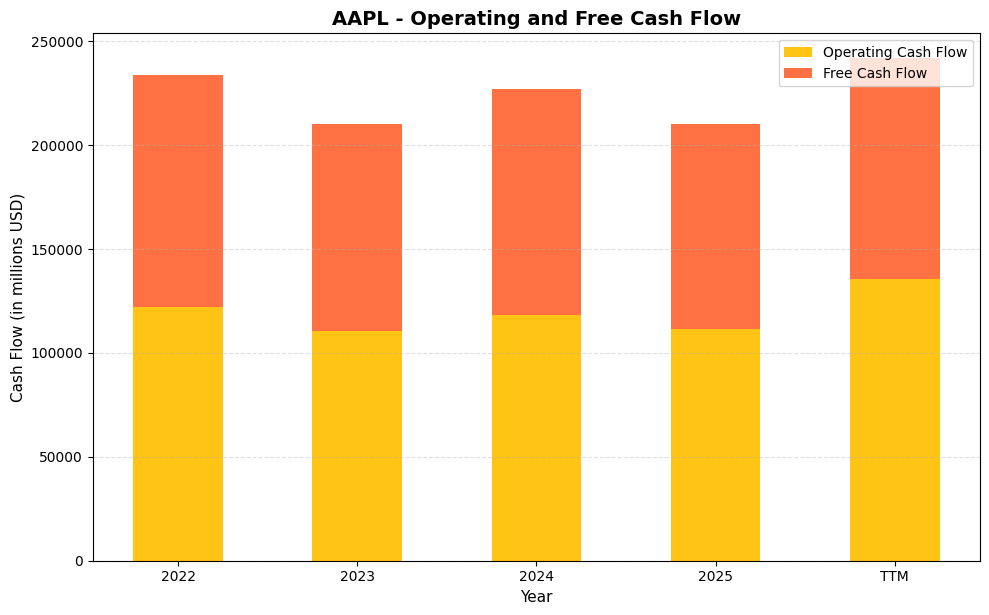

Cash Flow Statement

Apple’s cash generation remains among the most formidable in the equity market, and the trailing twelve month figures underscore that point convincingly. Operating cash flow reached $135,472 million on a TTM basis, the strongest reading in this five year window, while free cash flow came in at $106,312.8 million after accounting for capital expenditures. That free cash flow figure alone covers Apple’s annual dividend obligation many times over, which places the payout on exceptionally firm footing. Even in the softer years, such as fiscal 2023 when operating cash flow dipped to $110,543 million and free cash flow fell to $99,584 million, the company never came close to straining its capacity to reward shareholders. For dividend growth investors, that kind of floor matters as much as the ceiling.

Looking across the full period from 2022 through 2025, operating cash flow has fluctuated in a relatively tight band between $110,543 million and $122,151 million before the TTM surge, which reflects both the cyclical nature of consumer hardware demand and Apple’s ability to offset hardware softness with higher margin services revenue. Free cash flow conversion has remained consistently high, with free cash flow representing roughly 89 to 92 percent of operating cash flow in most years, a testament to the capital light character of the business outside of its ongoing manufacturing and R&D commitments. The fiscal 2025 figure of $98,767 million in free cash flow, while slightly below the 2022 peak, still represents a vast pool of capital available for dividends, buybacks, and balance sheet management. Shareholders collecting Apple’s dividend are drawing from one of the deepest and most durable free cash flow streams available in the large cap universe.

Analyst Ratings

The analyst community remains broadly constructive on Apple heading into 2026, with 41 analysts covering the stock and a consensus buy rating in place. The mean price target of $293.07 sits above the current trading price of $274.23, implying modest upside of roughly 7% from current levels on a price target basis alone, before accounting for dividends and buyback-driven EPS accretion.

The range of analyst opinion is wide, which reflects the genuine uncertainty around several key variables. The low-end target of $205.00 captures the more cautious view, centered on concerns about valuation at a 34.49 P/E multiple, the ongoing regulatory environment, and questions about whether Apple’s AI integration will drive a meaningful upgrade cycle in the near term. The high-end target of $350.00 reflects the bull case, which leans on continued services margin expansion, a successful international rollout of Apple Intelligence, and the compounding effect of the buyback program reducing the share count over time. With the stock trading near the midpoint of that range, the market appears to be pricing in a reasonable base case rather than assigning credit to the most optimistic scenario.

Earning Report Summary

Apple’s most recent reported results showed the company continuing to execute across its core business lines, with revenue of $435.6 billion on a trailing twelve-month basis and net income of $117.8 billion. EPS of $7.95 reflects both the strength of the underlying business and the ongoing benefit of share count reduction through buybacks. The profit margin of 27.04% demonstrates that Apple’s revenue mix continues to shift favorably toward higher-margin services revenue, even as hardware volumes remain the largest single contributor to the top line.

Services Remain the Growth Engine

The services segment has continued to be the standout performer in Apple’s portfolio, growing at a pace that outstrips the broader company and generating margins that are substantially higher than the hardware business. The App Store, iCloud, Apple TV+, and Apple Pay collectively represent an increasingly significant share of total revenue, and the subscription nature of much of this revenue provides a degree of stability and predictability that the hardware cycle alone cannot. Management has consistently pointed to services as the primary lever for long-term margin improvement.

Hardware Holds Steady

iPhone remains the largest single revenue category, and performance has been supported by the gradual international expansion of Apple Intelligence features that had initially been limited to the U.S. market. Mac and iPad have also contributed positively, benefiting from a combination of new product introductions and an enterprise customer base that has proven resilient. Wearables and home products have been a more mixed story, though the category continues to generate meaningful revenue and keeps customers deeper within the Apple ecosystem.

Geographic Diversification

Apple’s revenue base spans the Americas, Europe, Greater China, Japan, and the rest of Asia Pacific, providing a degree of geographic diversification that cushions the impact of weakness in any single region. Greater China remains a closely watched variable given the competitive dynamics from local brands and the sensitivity of that market to broader geopolitical developments. Record performance in the Americas and solid results in Europe have helped offset pockets of softness elsewhere, and Apple’s installed base of active devices now exceeds 2.35 billion globally, providing a vast foundation for services monetization.

Looking Ahead

Management has guided toward continued low to mid-single-digit revenue growth for the coming quarters, with services expected to maintain double-digit growth rates and the hardware business benefiting as Apple Intelligence becomes available to a larger share of the global user base. The longer-term story centers on margin expansion driven by mix shift toward services, continued share count reduction through buybacks, and the potential for new product categories to open incremental revenue streams. The fundamentals remain sound, and the cash flow machine underlying this business continues to run with exceptional consistency.

Management Team

Tim Cook has led Apple since 2011 and continues to set the strategic direction for a company that has grown dramatically in both scale and complexity under his tenure. His operational discipline has been a defining feature of Apple’s financial performance, and his focus on building out the services business while maintaining the premium positioning of the hardware lineup has proven to be a durable strategy. Cook’s measured approach to AI investment and integration reflects his broader style of moving deliberately rather than chasing headlines.

Jeff Williams serves as Chief Operating Officer and is widely credited with keeping Apple’s global supply chain and operations running with the kind of efficiency that underpins the company’s exceptional margins. Kevan Parekh, who was appointed Chief Financial Officer in early 2025, brings deep institutional knowledge of Apple’s financial structure and has stepped into the role at a time when capital allocation decisions, regulatory pressures, and the services growth narrative all demand careful financial stewardship.

Craig Federighi leads software engineering, playing a central role in the development and rollout of Apple Intelligence and the broader software ecosystem that keeps users engaged across Apple’s hardware platforms. Johny Srouji oversees hardware technologies, including the silicon development that has given Apple a meaningful performance and efficiency advantage in its devices. Eddy Cue continues to run the services segment, which has become one of the most important revenue and profit contributors in the entire company. This leadership group has worked together through multiple product cycles and market environments, and their collective experience represents a genuine competitive asset.

Valuation and Stock Performance

Apple trades at $274.23 as of February 25, 2026, representing a market capitalization of just over $4 trillion. The 52-week range of $169.21 to $288.62 reflects a stock that has moved meaningfully over the past year, recovering from a significant trough to trade near the upper end of its range. That recovery has been driven by a combination of improving earnings momentum, the services growth narrative, and renewed investor interest in AI-adjacent stories within the large-cap technology space.

The current P/E ratio of 34.49 is not cheap by historical standards for Apple, and it does demand that the company continue to execute on its growth plan to justify the multiple. A price-to-book of 45.72 reflects both the asset-light nature of the business and the fact that years of aggressive buybacks have compressed the book value per share to $6.00. These are not metrics that traditional value investors will find attractive, but they reflect the reality of owning a business with a 152% return on equity and $106 billion in annual free cash flow.

The mean analyst price target of $293.07 suggests the stock is not dramatically mispriced at current levels, though the high-end target of $350.00 captures the potential upside if the AI-driven upgrade cycle materializes more forcefully than the base case assumes. For long-term dividend growth investors, the valuation question is secondary to the trajectory of cash flow and dividend growth, and on both of those dimensions, Apple continues to deliver.

Risks and Considerations

Apple’s dependence on China as both a manufacturing hub and a major revenue market remains one of the most consequential risks in the story. Geopolitical tensions between the United States and China have already introduced volatility into Apple’s supply chain planning and created revenue headwinds in the Greater China region, where local competitors have gained share. The company has been actively diversifying production into India and Vietnam, but transitioning a supply chain of Apple’s complexity takes years and involves meaningful execution risk along the way.

The regulatory environment is becoming an increasingly material consideration for Apple’s business model. Antitrust investigations in the United States, Europe, and other jurisdictions are focused on App Store practices, the terms Apple imposes on third-party developers, and the broader question of whether Apple’s ecosystem constitutes an anticompetitive structure. Adverse rulings in any of these proceedings could require Apple to change how it operates its platform, potentially affecting the revenue and margins of the services segment that investors have come to rely on as a growth driver.

Competition across Apple’s core markets continues to intensify. In smartphones, Android manufacturers at both the premium and mid-range tiers have become more capable, and in several international markets, local brands have demonstrated an ability to capture share from Apple. In the services arena, Apple competes against well-capitalized platforms in streaming, cloud storage, digital payments, and advertising, all of which are investing heavily to win and retain users. Maintaining the ecosystem’s gravitational pull over the long term requires continuous investment and execution.

The valuation multiple of 34.49 times earnings leaves the stock with limited tolerance for disappointment. If the AI-driven upgrade cycle fails to materialize on the timeline the market is pricing in, or if services growth decelerates more than expected, the stock could re-rate lower even if the underlying business remains fundamentally healthy. Consumer spending sensitivity to macroeconomic conditions is also a factor, as premium hardware purchases are among the first things households defer when budgets come under pressure.

Final Thoughts

Apple enters 2026 from a position of extraordinary financial strength. Revenue of $435.6 billion, free cash flow of $106.3 billion, and a dividend that has grown for 13 consecutive years paint the picture of a company that has institutionalized both operational excellence and shareholder-friendly capital allocation. The dividend yield of 0.38% will never attract income-focused investors looking for a large current payout, but the combination of a 13.04% payout ratio, consistent annual increases, and one of the most powerful buyback programs in corporate history makes Apple a genuine compounder for patient long-term holders.

The risks are real and worth monitoring closely. China exposure, regulatory pressure, and a demanding valuation multiple all require that management continue to execute with the discipline that has characterized Tim Cook’s tenure. None of these risks are new, and Apple has navigated versions of each of them before, but they deserve weight in any honest assessment of the story.

For dividend growth investors with a long time horizon, Apple remains one of the most financially durable names available. It is not a yield story, and it is not a deep value story. It is a story about a business that generates cash with remarkable consistency, returns that cash to shareholders in growing quantities, and has built an ecosystem that keeps billions of users engaged across multiple product and service categories. That combination is genuinely rare, and it continues to earn Apple a place in the conversation.