Updated 2/25/26

Altria has long been a staple for dividend-focused investors, and for good reason. It’s not flashy, it’s not fast-growing, and it certainly doesn’t get much media attention. But when it comes to reliability, MO consistently shows up. This is the kind of stock you buy for one reason: dependable income. And in today’s yield-hungry world, that makes it worth a closer look.

Best known as the maker of Marlboro cigarettes in the U.S., Altria has been around the block. Over the years, it has expanded into smokeless products and even taken swings at cannabis and vaping. Despite that, its core earnings still come from the traditional cigarette business. That might sound dated, but it’s also a cash machine. And for income investors, that consistency matters a lot more than trendiness.

MO’s stock has pushed to new territory lately, trading near $69.70 and sitting just below its 52-week high of $69.98. The share price has climbed sharply from the 52-week low of $52.82, representing a gain of more than 31% from trough to current levels. For a company that doesn’t rely on hype, that kind of move commands attention.

Recent Events

Altria has continued to execute on its core strategy heading into early 2026, with the most meaningful recent development being a fresh dividend increase. In September 2025, the company raised its quarterly dividend from $1.02 to $1.06 per share, a move that brought the annualized payout to $4.24 and reinforced management’s commitment to returning capital to shareholders. That increase, the latest in a long string of hikes, was accompanied by confirmation that the company’s smoke-free portfolio continues to develop, with NJOY remaining a centerpiece of Altria’s long-term product strategy despite persistent headwinds from illicit e-vapor products that have crowded the market.

On the regulatory front, Altria has continued to engage with the FDA around its non-combustible product lineup, and the industry broadly remains in a period of heightened scrutiny as authorities push back against unauthorized vapor products. That dynamic has complicated growth projections for NJOY, though the brand has maintained retail presence and is building incremental share in its authorized category. Meanwhile, the oral tobacco brand on! reached profitability ahead of schedule in late 2024, providing a meaningful contribution to the smoke-free segment’s credibility.

The company also wrapped up its previously announced $1 billion share repurchase program, continuing a pattern of buyback activity that has helped support earnings per share even as cigarette volumes face structural pressure. With shares trading near all-time highs, attention has turned to whether Altria’s premium valuation relative to its own history is justified by the durability of its cash generation and dividend profile.

Key Dividend Metrics

📈 Forward Yield: 6.01%

💵 Annual Dividend (Forward): $4.24

📆 5-Year Average Yield: 7.99%

🔄 Payout Ratio: 100.97%

📊 Dividend Growth (Last Raise): 3.92%

💰 Last Quarterly Payment: $1.06

📅 Last Ex-Dividend Date: December 26, 2025

Dividend Overview

The dividend is why most people own this stock, and at a 6.01% forward yield on a $69.70 share price, it remains one of the more attractive income propositions in the consumer defensive space. The annualized payout now stands at $4.24, supported by a quarterly rate of $1.06 that was established with the September 2025 increase. For investors who have held MO through its recent run-up, the yield on cost is naturally lower, but for anyone buying today, a 6% yield backed by a company with Altria’s cash generation profile is still a compelling starting point.

The payout ratio has climbed to just over 100% on a reported earnings basis, which warrants some attention. However, that figure reflects reported net income of approximately $4.12 in EPS rather than the adjusted earnings the company uses to guide dividend policy. Altria has historically targeted a payout ratio of around 80% of adjusted earnings, and on that basis the dividend remains well covered. The company’s profit margin of 34.49% and return on assets of 21.77% both point to a business that is generating real economic value, not simply borrowing to fund its distribution.

What makes MO especially appealing is how predictable it is. Shareholders have received a dividend every quarter without interruption, and the trajectory of increases over the past several years, from $0.94 per quarter in early 2023 to $1.06 today, reflects a company that takes its income-investor base seriously. In an environment where many high-yield names have cut or suspended payouts, that track record carries genuine weight.

Dividend Growth and Safety

Altria’s most recent dividend increase, announced alongside the September 2025 payment, brought the quarterly rate from $1.02 to $1.06, representing growth of approximately 3.92%. That follows a similar-sized increase a year earlier, when the payout moved from $0.98 to $1.02. The pace is measured rather than aggressive, but it has been consistent, and in the context of a mature business navigating long-term volume declines, steady growth is the appropriate benchmark.

Looking at the dividend history over the past two-plus years, the pattern is clear. Altria has raised its payout twice annually, typically in the second and fourth quarters, and has not missed a beat. From $0.94 per quarter in early 2023 to the current $1.06, the cumulative growth comes to just under 13% over roughly three years. That’s not explosive, but it meaningfully outpaces inflation over the same period and keeps the real value of the income stream intact for long-term holders.

The safety of the dividend rests on the company’s ability to generate cash from its core tobacco operations. With a profit margin above 34% and revenue of over $20 billion, the earnings engine remains intact even as cigarette volumes decline. Free cash flow data was not separately disclosed in the current reporting period, but the company’s capital-light operating model and historically low capital expenditure requirements suggest that cash generation continues to comfortably support both the dividend and the buyback program. The negative book value is a product of accumulated share repurchases and should not be read as a sign of financial distress in a business with Altria’s earnings consistency.

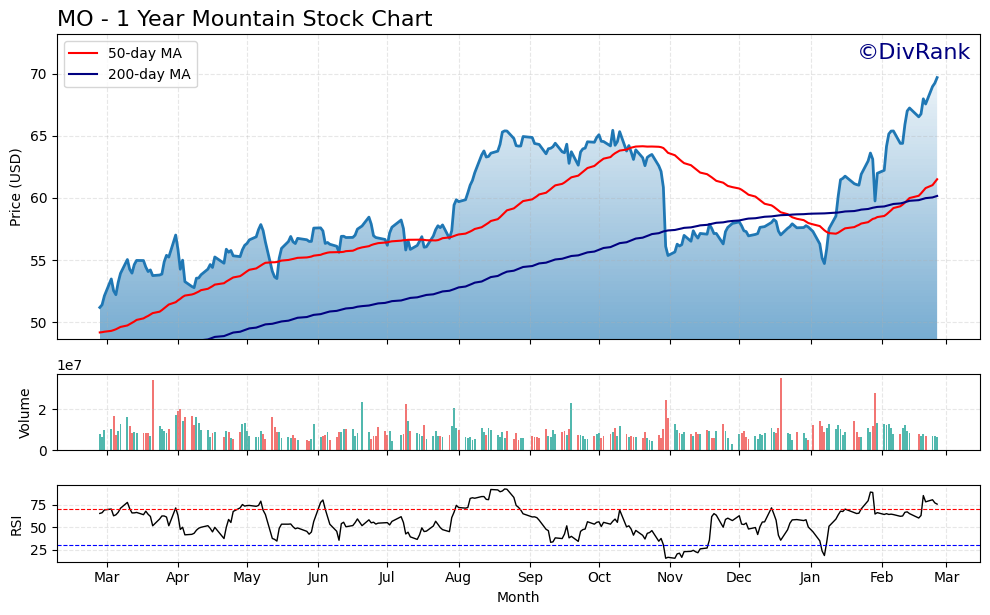

Chart Analysis

Altria’s price action over the past year tells a compelling recovery story. Shares bottomed near $51.18 at the 52-week low and have climbed steadily to reach $69.70, which is exactly where the stock sits today, right at its 52-week high. That 36% move off the trough reflects genuine institutional accumulation rather than a brief speculative pop, and the fact that MO is pressing against fresh annual highs without any meaningful consolidation speaks to the underlying demand for the shares. For income investors who may have trimmed or hesitated near those lows, the chart is now offering a different kind of message entirely.

The moving average picture reinforces the bullish trend. The 50-day moving average sits at $61.51 and the 200-day at $60.16, and MO is trading well above both levels. Critically, the 50-day has crossed above the 200-day, producing what technicians recognize as a golden cross, a configuration that historically signals the transition from a corrective phase into a sustained uptrend. The spread between current price and both moving averages is wide enough to confirm that the trend has real momentum behind it rather than being a marginal or tentative breakout.

The RSI reading of 75.8 deserves honest attention. At that level, MO is firmly in overbought territory by conventional standards, and short-term traders watching that indicator would flag the risk of a near-term pullback or at least a period of sideways consolidation. For dividend investors, overbought conditions in a stock making new highs are less alarming than they would be in a deteriorating name, but the reading does suggest that chasing the position aggressively at current prices carries more timing risk than it did even a few weeks ago.

The overall takeaway for dividend investors is that Altria’s chart is constructive on every intermediate-term measure, with a golden cross in place, price comfortably above both key moving averages, and a clean breakout to 52-week highs. The one legitimate caution is that the RSI is stretched, which means investors adding at current levels should size positions with the expectation that a 5% to 8% consolidation is possible before the next leg higher. For those already holding, the technical trend offers no reason to reduce exposure, and the chart continues to support collecting MO’s generous dividend from a position of relative strength.

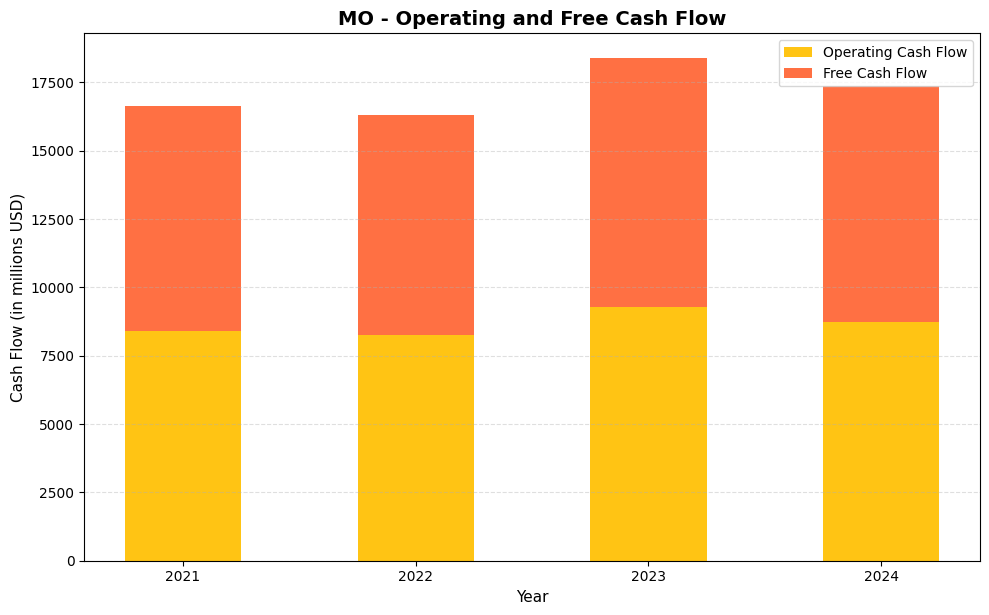

Cash Flow Statement

Altria’s cash flow profile is one of the most compelling arguments for its status as a core dividend holding. Operating cash flow has held in a tight range across the four-year window, coming in at $8,405M in 2021, dipping modestly to $8,256M in 2022, surging to $9,287M in 2023, and settling back to $8,753M in 2024. Free cash flow tracks closely in each year, at $8,236M, $8,051M, $9,091M, and $8,611M respectively, which reflects the minimal capital expenditure demands of a mature consumer staples business. With the company paying out roughly $6.6B in dividends in fiscal 2024, that $8,611M in free cash flow translates to a free cash flow payout ratio comfortably below 80%, giving management meaningful room to sustain and grow the dividend without straining the balance sheet.

The four-year trend tells a reassuring story of durability rather than deterioration. Even in the softer years of 2021 and 2022, free cash flow never fell below $8B, which underscores just how capital-light and cash-generative Altria’s core tobacco franchise remains. The spike in 2023 to over $9B in both operating and free cash flow demonstrated that the business can still produce upside surprises even as cigarette volumes decline, largely because pricing power continues to offset volume pressure with impressive consistency. For dividend investors, the takeaway is straightforward: Altria converts revenue into distributable cash at a rate that few businesses in any sector can match, and the stability of that conversion across varying macro conditions makes the dividend far less speculative than the stock’s high yield might initially suggest.

Analyst Ratings

The analyst community carries a consensus buy rating on Altria as of late February 2026, with 12 analysts contributing to the current consensus. That constructive overall stance reflects the company’s durable earnings profile and continued dividend growth, though the current stock price relative to the average price target introduces some nuance worth examining. The mean price target among covering analysts sits at $64.42, which is meaningfully below the current trading price of $69.70. That gap suggests that at current levels, the stock has traded through the midpoint of analyst expectations, which may explain why sentiment has not moved more aggressively into strong buy territory despite the formal consensus designation.

The range of targets is wide, spanning from a low of $47.00 to a high of $73.00. The upper end of that range at $73.00 is only modestly above where shares are trading today, implying that even the most optimistic analyst on the Street sees limited near-term price appreciation from current levels. The low target of $47.00 reflects the bear case, which typically centers on accelerating cigarette volume declines, regulatory risk around non-combustible products, and the elevated debt load. With the stock sitting near the top of its 52-week range and above the analyst consensus target, income investors should anchor their thesis on the 6% yield and dividend growth trajectory rather than expecting significant capital appreciation in the near term.

Earning Report Summary

A Solid Close to 2024

Altria wrapped up 2024 on a strong note. Adjusted earnings per share came in at $1.29 for the fourth quarter, which marked a 9.3% jump from the same time the prior year. For the full year, the company delivered $5.12 in adjusted EPS, up a respectable 3.4%. Revenue held steady, landing at $5.97 billion for the quarter, and after factoring out excise taxes, net revenue rose slightly to $5.1 billion. The company also kept its operating margin solid at just over 60%, showing that it continues to run a tight and efficient operation.

Leadership Perspective and Outlook

CEO Billy Gifford described 2024 as a year of meaningful progress. He pointed to the strength of Altria’s core tobacco business and noted that the company stayed on course with its long-term vision while balancing short-term results with investments in its smoke-free future. Looking ahead into 2025, Altria had guided for earnings in the range of $5.22 to $5.37 per share, representing 2% to 5% growth over 2024, with that guidance incorporating the continued rollout of its smoke-free product strategy. Full 2025 results will be reported in the coming weeks and will provide an important update on whether that guidance range was achieved.

Smoke-Free Challenges and Wins

The NJOY brand saw meaningful growth through the back half of 2024, with consumable shipments rising over 15% in Q4 to 12.8 million units. NJOY held approximately 6.4% of retail share in its authorized category, building incremental traction. The most significant challenge facing the brand remains the proliferation of illegal e-vapor products, which account for more than 60% of the broader vapor market and make it structurally difficult for FDA-authorized brands to scale as originally anticipated. That competitive dynamic led Altria to revise its original 2028 smoke-free volume and revenue targets, and the recalibration has tempered expectations for how quickly non-combustible products will meaningfully displace cigarette earnings.

The oral tobacco brand on! provided a more encouraging story, reaching profitability in the fourth quarter of 2024 ahead of its original 2025 target. That milestone demonstrated that Altria’s smoke-free investments can generate returns, and it offered some offset to the more complex narrative surrounding NJOY and the vapor category.

Commitment to Shareholders

Altria completed its $3.4 billion share buyback program in 2024 and followed that with a plan for an additional $1 billion in repurchases to be completed in 2025. Dividends returned approximately $6.8 billion to shareholders over the course of the year. That level of capital return remains one of the central attractions of the investment thesis, and the September 2025 dividend increase to $1.06 per quarter confirmed that the company’s commitment to growing the payout has not wavered as shares have moved higher.

Management Team

Altria Group is led by CEO Billy Gifford, who stepped into the role in 2020 after spending decades with the company in progressively senior positions including CFO. His institutional knowledge of the business gives him a grounded perspective on navigating regulatory complexity, managing the transition toward smoke-free products, and maintaining the financial discipline that income investors have come to rely on. Gifford has been consistent in his messaging around prioritizing shareholder returns while making measured investments in the company’s long-term product evolution.

Working alongside Gifford is a leadership team with deep experience across operations, finance, legal affairs, and corporate strategy. Jody Begley, serving as Chief Operating Officer, provides the operational oversight that is particularly important as the company scales its smoke-free portfolio. Sal Mancuso continues as CFO, overseeing a capital allocation strategy that has consistently balanced generous dividend growth with debt management and share repurchases. It is a team that has demonstrated the ability to execute on the core business while managing a genuinely complex transition, and there have been no significant management departures or leadership disruptions that would alter that assessment heading into 2026.

Valuation and Stock Performance

Altria’s stock is trading at $69.70 as of February 25, 2026, with a market cap of approximately $117 billion. The shares are within striking distance of the 52-week high of $69.98, having recovered sharply from the 52-week low of $52.82. That recovery of more than 31% over the past year has compressed the yield from what would have been a notably higher entry point and pushed the stock’s valuation toward the upper end of its recent historical range.

With reported EPS of $4.12 over the trailing twelve months, the current P/E ratio sits at 16.92. That is a meaningfully higher multiple than the single-digit P/E that MO has traded at for much of the past decade, and it reflects a re-rating that has occurred as investors have increasingly embraced consumer defensive names with durable yield profiles. Whether that multiple is sustainable depends largely on whether Altria can continue delivering low-single-digit earnings growth while maintaining the dividend. The forward earnings picture, informed by the company’s own guidance trajectory, suggests the premium is not unreasonable, but it does reduce the margin of safety for new buyers relative to where the stock sat a year ago. The negative price-to-book ratio is a mathematical artifact of the company’s aggressive buyback program reducing book value below zero and should not be interpreted as a valuation concern in isolation.

Risks and Considerations

The cigarette industry continues to face structural volume declines, and Altria remains heavily dependent on traditional combustible tobacco for the vast majority of its earnings. Regulatory pressure has intensified over time, and there is no realistic scenario in which that trend reverses. The company’s ability to offset volume declines through pricing has been a reliable tool historically, but there are limits to how aggressively price increases can be pushed before accelerating the consumer shift away from the category.

The illicit e-vapor market presents a particularly thorny challenge for Altria’s non-combustible ambitions. Unauthorized products now account for more than 60% of the vapor market, creating a structurally uneven playing field for FDA-authorized brands like NJOY. Until enforcement improves meaningfully, NJOY’s ability to reach the market share targets that originally justified Altria’s investment in the brand will remain constrained. This has already forced a revision of smoke-free volume and revenue targets, and further recalibration is possible.

The payout ratio on a reported earnings basis has crossed above 100%, which is a figure that demands context but also cannot be dismissed entirely. While adjusted earnings provide a more accurate picture of the company’s true dividend coverage, any sustained deterioration in core earnings would narrow the margin of comfort. Investors should monitor the full-year 2025 earnings report closely for signs of whether the adjusted EPS trajectory remains on track with prior guidance.

Altria carries a substantial debt load, and while the company has managed that obligation effectively given its stable operating cash flows, a meaningful deterioration in earnings or an adverse shift in the interest rate environment could increase the pressure on the balance sheet. The company’s ability to continue funding dividends, buybacks, and debt service simultaneously depends on the tobacco business continuing to generate cash at historically high levels, which is not guaranteed as volumes decline over time.

Final Thoughts

Altria remains one of the more reliable income-generating names available to dividend-focused investors, and the September 2025 dividend increase to $1.06 per quarter is a reminder that the company continues to prioritize shareholder returns even as its operating environment grows more complex. At a 6.01% yield on a $69.70 stock price, MO offers a meaningful income advantage over most fixed income alternatives, backed by a business that has proven its ability to generate cash through a variety of market conditions.

The re-rating of the stock toward a P/E above 16 is a meaningful change from where MO has historically traded, and it reduces some of the valuation cushion that made earlier entry points so attractive. The mean analyst price target of $64.42 sitting below the current price suggests the market has already priced in a good deal of the positive narrative, which means the total return case from here is more heavily weighted toward income than capital appreciation.

For long-term income investors, that calculus is entirely acceptable. Altria does what it has always done: run a lean, highly profitable business, grow the dividend steadily, and return capital to shareholders in ways that compound over time. The risks around volume declines, illicit competition, and a higher payout ratio on reported earnings are real and deserve ongoing monitoring. But for those who understand the business and are buying primarily for income, MO at current levels continues to offer a compelling, if somewhat fully valued, position in a well-constructed dividend portfolio.