Updated 2/25/26

Allison Transmission Holdings, Inc. (ALSN) is a profitable, well-managed company serving the commercial and defense vehicle markets through its specialty in fully automatic transmissions. With strong fundamentals including a 20.7% profit margin, over $836 million in trailing twelve-month operating cash flow, and a return on equity above 35%, the business continues to generate solid cash while maintaining a conservative 13% payout ratio. Leadership, anchored by CEO David Graziosi, has steered the company with a focus on disciplined capital allocation and innovation. Shares have climbed sharply over the past year, approaching their 52-week high near $124, supported by healthy free cash flow and consistent dividend growth. The current valuation reflects a market that is increasingly pricing in Allison’s earnings quality, with a P/E of 15 and analyst price targets ranging from $95 to $155. For investors tracking financially sound companies with steady income potential, ALSN presents a compelling profile backed by execution, resilience, and strategic focus.

Recent Events

Allison Transmission has continued building on its strong 2024 performance as it moves through the early months of 2026. The company closed out fiscal 2025 with another year of solid execution, posting full-year revenue of approximately $3.0 billion and net income of $623 million, reflecting disciplined cost management and steady demand across its core commercial vehicle and defense segments. Operating cash flow for the trailing twelve months reached $836 million, reinforcing the company’s reputation as a reliable cash generator in an industrial landscape where such consistency is increasingly valued.

On the product side, Allison has continued advancing its electrified propulsion systems, including its eGen Power and eGen Flex electric axle and hybrid solutions targeted at commercial fleets navigating the transition away from conventional drivetrains. These platforms have attracted growing interest from municipalities and fleet operators looking to meet emissions mandates without abandoning the reliability they associate with the Allison name. Defense segment activity has also remained active, with continued production and support work tied to military vehicle programs that provide a degree of revenue stability independent of commercial market cycles.

The company’s share repurchase program has remained a consistent feature of its capital return strategy. Management has continued reducing the share count in a meaningful way, which has supported earnings per share growth and demonstrated confidence in the business’s long-term cash flow trajectory. At the same time, Allison raised its quarterly dividend to $0.27 per share beginning in early 2025, representing an 8% increase over the prior $0.25 rate and continuing the pattern of steady annual dividend growth the company has maintained for several years.

Key Dividend Metrics

📈 Forward Dividend Yield: 0.89%

💵 Annual Dividend: $1.08

🔁 Recent Dividend Growth: 8% (from $0.25 to $0.27 per quarter)

🧱 Payout Ratio: 13.01%

💡 5-Year Average Yield: ~1.50%

🧮 Free Cash Flow (TTM): $500.6M

💪 Return on Equity: 35.42%

📊 Return on Assets: 10.65%

Dividend Overview

At first glance, Allison’s dividend yield might not turn many heads. Sitting at 0.89%, it is not the kind of payout that income investors rush into for immediate cash flow. But the low yield is more a reflection of significant share price appreciation and a conservative distribution philosophy than any lack of underlying earning power. The stock has climbed substantially over the past year, rising from the low $80s toward its current level near $123, which has compressed the yield even as the dividend itself has grown.

The dividend remains exceptionally well covered. With a payout ratio of just 13%, Allison is distributing a small fraction of its earnings to shareholders, leaving substantial room to grow the dividend further or redirect capital toward buybacks, debt management, or business reinvestment. The company generated $836 million in operating cash flow over the trailing twelve months, with free cash flow of approximately $501 million after capital expenditures. That cash generation comfortably supports the annual dividend commitment many times over.

The most recent dividend increase, which lifted the quarterly payment from $0.25 to $0.27 beginning in March 2025, marked an 8% raise and continued the company’s pattern of annual dividend increases. Since 2023, the quarterly dividend has risen from $0.23 to $0.27, representing an increase of roughly 17% over that two-year span. While the yield remains modest in absolute terms, the trajectory of growth is consistent and credible, underpinned by earnings and cash flow that are not under pressure.

Dividend Growth and Safety

The dividend growth story at Allison is one of steady, unhurried compounding rather than dramatic headline increases. The company has raised its quarterly payout in each of the past several years, moving from $0.23 per quarter in 2023 to $0.25 in 2024 and $0.27 in 2025. That pattern of annual 8 to 9% increases is meaningful for investors who reinvest dividends or rely on growing income streams to offset inflation over time.

Safety is rarely a concern given the numbers in play. A 13% payout ratio means the company would need to see earnings fall by more than 85% before the dividend came under any meaningful stress. With profit margins near 21% and operating cash flow well above $800 million, the cushion is substantial. Even in a cyclical downturn scenario, Allison would likely have ample room to maintain its current payout without disruption.

Institutional ownership in the stock remains high, reflecting confidence among large funds in the company’s capital discipline and cash flow durability. Management has demonstrated a consistent preference for returning capital to shareholders through both dividends and buybacks, and the low payout ratio preserves flexibility to accelerate dividend growth if the business environment remains favorable. For long-term investors who prioritize sustainability and upward trajectory in their dividend income, Allison’s approach fits that mold precisely.

Chart Analysis

Allison Transmission has put together a remarkable run over the past twelve months, climbing from a 52-week low of $79.01 to its current price of $122.72, which also happens to be the exact 52-week high. That 55% advance from trough to peak reflects sustained buying pressure rather than a brief speculative spike, and the fact that shares are printing new highs at the time of this writing suggests there is no obvious technical ceiling constraining the stock at current levels. The trend across the full year is unambiguously upward, with higher lows and higher highs characterizing the price structure throughout the period.

The moving average picture reinforces that bullish read. Allison’s 50-day moving average sits at $108.20 and its 200-day moving average at $94.38, meaning the stock is trading a meaningful 13.4% above the near-term average and nearly 30% above the long-term average. Critically, the 50-day has crossed above the 200-day, producing the classic golden cross formation that technical analysts associate with durable intermediate-to-long-term uptrends. For dividend investors, a stock trending well above both major moving averages provides a degree of cushion against short-term volatility without immediately threatening the total return thesis.

Momentum, as measured by the 14-period Relative Strength Index, is running hot at 73.93, which places the stock in technically overbought territory. An RSI above 70 does not by itself signal an imminent reversal, particularly when a stock is emerging from a multi-month breakout, but it does indicate that the recent advance has been rapid enough to absorb a consolidation phase or a modest pullback without any damage to the underlying trend. Investors initiating a new position here should be mentally prepared for the stock to pause and digest recent gains near current levels, even if the longer-term trajectory remains constructive.

Taken together, the technical backdrop for Allison Transmission is as strong as it has been at any point in the past year, which is both an opportunity and a caution for income-focused buyers. The trend, the moving average alignment, and the new-high price action all argue that this is not a deteriorating business being propped up by yield-seekers. At the same time, purchasing any stock at a 52-week high with an RSI near 74 requires patience, as short-term mean reversion is a legitimate near-term risk. Dividend investors with a multi-year time horizon may view any technical pullback toward the rising 50-day moving average, currently near $108, as a more favorable entry point relative to current levels.

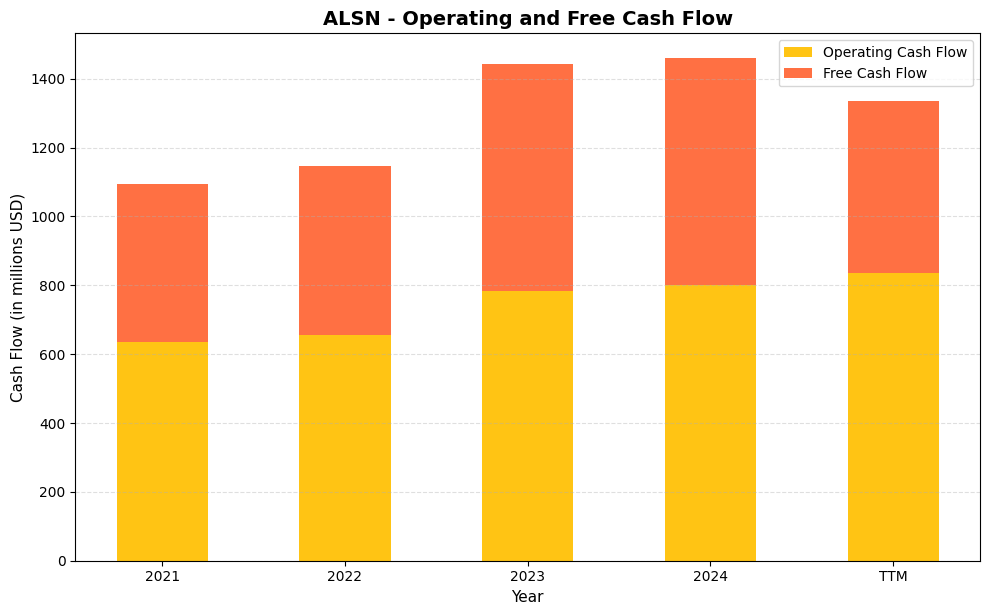

Cash Flow Statement

Allison Transmission’s cash flow profile is one of the cleaner stories in the industrial space, and the numbers make a compelling case for dividend sustainability. Operating cash flow climbed from $635.0M in 2021 to $801.0M in 2024, with the TTM figure pushing even further to $836.0M, representing a gain of roughly 32% over the full period. Free cash flow followed a similarly constructive path, rising from $460.0M in 2021 to a peak of $659.0M in 2023 before settling at $658.0M in 2024. The TTM free cash flow of $500.6M reflects a step down from that peak, which warrants monitoring, but the absolute level remains more than sufficient to cover dividend obligations with meaningful room to spare. For an income investor, the consistency here matters as much as the growth, and Allison has delivered both.

Zooming out across the four-year arc, what stands out is the steady improvement in capital efficiency. The gap between operating cash flow and free cash flow narrowed in 2023 and held tight in 2024, suggesting that capital expenditures have been disciplined rather than expansionary for expansion’s sake. The TTM free cash flow dip to $500.6M against operating cash flow of $836.0M implies a pickup in capex spending, which could reflect reinvestment in manufacturing capacity or product development, and shareholders should track whether that spending translates into earnings growth over the next several quarters. Even accounting for that variability, Allison’s free cash flow generation has been consistently robust enough to fund its dividend program, support share repurchases, and maintain a manageable balance sheet, a combination that gives dividend growth investors a durable foundation to build on.

Analyst Ratings

The analyst community has grown more constructive on Allison Transmission as the stock has moved higher and the company’s earnings quality has become increasingly apparent. The current consensus among the 10 analysts covering the stock is a buy rating, a shift in tone from the more cautious hold stance that prevailed in early 2025 when concerns about near-term revenue growth weighed on sentiment. That change in consensus reflects both the company’s execution over the past several quarters and growing confidence in the durability of its cash flow and margins.

The mean 12-month price target across analysts sits at $123.80, which is essentially in line with the current share price of $122.72, suggesting the stock is viewed as fairly valued at present levels after its significant run higher. The range of targets is notably wide, however, spanning from a low of $95 to a high of $155. That spread reflects genuine disagreement about how much credit the market should assign to Allison’s electrification efforts and the longer-term trajectory of commercial vehicle demand. Bulls point to the company’s free cash flow generation, disciplined buyback program, and expanding product portfolio as drivers of further multiple expansion. The more cautious targets around $95 likely incorporate scenarios where commercial vehicle production softens or where competitive pressure from emerging drivetrain technologies intensifies more quickly than expected.

With the stock trading just below the average target, investors are essentially being asked to pay consensus fair value today for a business generating over $8 in earnings per share and growing its dividend consistently. The upside case to $155 would require either meaningful earnings growth above current expectations or a re-rating of the multiple, both of which are plausible but not assured given where the broader industrial sector trades.

Earning Report Summary

Allison Transmission navigated fiscal 2025 with the steady hand that has come to characterize the company’s recent financial performance. Full-year revenue came in at approximately $3.0 billion, reflecting a modest moderation from the record $3.2 billion posted in 2024, but the profitability profile held up well. Net income for the year reached $623 million, and earnings per share landed at $8.15, supported in part by the ongoing reduction in share count from the company’s buyback activity.

Strong Profits and Efficient Execution

Profit margins remained a standout feature of the results. The net profit margin of 20.7% reflects a business that continues to exercise tight control over its cost structure, even as it invests in next-generation products and expands its international footprint. Return on equity of 35.4% and return on assets of 10.65% both confirm that management is generating strong value from the capital deployed in the business. Operating cash flow of $836 million was particularly noteworthy, reinforcing that the earnings being reported are backed by real cash rather than accounting adjustments.

Leadership’s Take and the Road Ahead

CEO Dave Graziosi has maintained a consistent message through recent communications, emphasizing Allison’s focus on long-term value creation through innovation in both conventional and electrified propulsion systems, operational discipline, and a capital allocation framework that balances investment in the business with meaningful returns to shareholders. CFO Scott Mell has echoed that focus on financial rigor, highlighting the company’s strong free cash flow position as the foundation for continued dividend growth and share repurchase activity. Looking into 2026, management has signaled confidence in the stability of demand across its key end markets, particularly North American on-highway commercial vehicles and defense, while acknowledging that the broader macroeconomic environment warrants ongoing attention. The underlying message from leadership is one of disciplined optimism: the fundamentals are sound, the product portfolio is evolving, and the company is well-positioned to navigate whatever the cycle brings.

Management Team

Allison Transmission is guided by a leadership team with deep industry knowledge and long-standing ties to the company. David Graziosi has been the CEO since 2018, but his connection to Allison dates back to 2007 when he came on board as Chief Financial Officer. His background in finance and steady leadership style have helped Allison navigate multiple market environments with clarity and discipline.

Scott Mell serves as CFO, bringing a strong international perspective and decades of experience in financial leadership roles. His presence has sharpened the company’s focus on operational discipline and long-term strategic planning, and his emphasis on cash flow management has been a consistent theme in recent investor communications.

The rest of the executive team features a blend of expertise in engineering, operations, product development, and global sales. Together, they form a leadership structure that has kept Allison well-aligned with both customer demands and the broader direction of the commercial and defense vehicle markets, including the growing importance of electrified and hybrid propulsion solutions.

Valuation and Stock Performance

Allison’s stock has had a remarkable run over the past twelve months, climbing from the low $80s to its current price near $122.72, approaching the 52-week high of $124.43. That move has meaningfully changed the valuation conversation. The trailing P/E of 15.06 is no longer the deeply discounted sub-10 multiple the stock carried in early 2025, but it remains reasonable for a business generating 20% plus net margins, strong free cash flow, and consistent earnings growth.

The price-to-book ratio of 19.69 reflects the company’s elevated return on equity and leveraged capital structure, which compress the book value per share to $6.23. That metric is less meaningful as a standalone valuation tool for Allison given the nature of its balance sheet, and investors are better served focusing on earnings and cash flow multiples. On those measures, the stock looks fairly valued relative to its intrinsic earnings power, with the mean analyst price target of $123.80 sitting essentially at the current price.

The beta of 0.98 indicates the stock moves roughly in line with the broader market, which is somewhat reassuring for income-oriented investors who might worry about volatility in an industrial name. Short interest of approximately 2 million shares is modest relative to the float, suggesting the bear case is not widely held. For investors who missed the run from the low $80s, the current price demands more confidence in continued earnings growth or multiple expansion, but the underlying business quality remains intact.

Risks and Considerations

The balance sheet carries a meaningful debt load, and while Allison’s strong operating cash flow has kept interest obligations manageable, the leverage does reduce financial flexibility in a scenario where business conditions deteriorate more sharply than expected. The company has demonstrated it can service and reduce debt while simultaneously returning capital to shareholders, but this dynamic bears watching, particularly if interest rates remain elevated for an extended period.

The structural shift toward electric and hybrid drivetrains represents the most significant long-term risk to Allison’s core business model. While the company has invested in electrified propulsion products including its eGen platform, some emerging technologies reduce or eliminate the need for traditional automatic transmissions altogether. The pace at which fleet operators adopt these alternatives will determine how much of Allison’s addressable market is ultimately disrupted, and that timeline remains genuinely uncertain.

Allison operates in markets that are cyclical by nature. Commercial vehicle production in North America, which remains the company’s largest revenue source, is sensitive to freight demand, interest rates, and broader economic conditions. A meaningful slowdown in truck orders or a reduction in defense spending could pressure revenue and margins, even if the company’s diversification across end markets provides some cushion against any single area of weakness. Investors should calibrate their expectations accordingly and recognize that the strong earnings of recent years have benefited from a favorable demand environment that may not persist indefinitely.

Final Thoughts

Allison Transmission is a company that knows its space well. It is not chasing headlines or speculative trends but rather sticking to what it does best: making reliable, high-performance transmissions for essential sectors while carefully evolving its product portfolio to address the changing demands of commercial and defense customers. The financials are sound, leadership is experienced, and the commitment to long-term shareholder value through dividends and buybacks is clear and consistent.

The stock’s significant appreciation over the past year means today’s buyers are paying a fair rather than bargain price, and the sub-1% yield will continue to limit appeal among pure income investors. But for those who take a total return view and appreciate the combination of earnings quality, free cash flow durability, and a dividend that grows reliably each year, Allison remains one of the more quietly compelling names in the industrial space. It may not generate the most excitement, but it continues to deliver where it counts.