Updated 2/25/26

Alliant Energy Corporation (LNT) is a Midwest-based regulated utility serving customers across Iowa and Wisconsin, with a growing focus on clean energy and infrastructure modernization. The company has now raised its dividend for 22 consecutive years, most recently lifting the quarterly payment to $0.535 per share in January 2026. Shares are trading near their 52-week high at $71.26, reflecting a meaningful re-rating from utility investors seeking stable income amid a shifting interest rate environment. With a current dividend yield of 2.83%, solid operating cash flow from regulated operations, and a management team executing steadily on its long-term capital plan, Alliant continues to offer the kind of dependable, low-drama total return profile that dividend growth investors value most.

Recent Events

Alliant Energy has been an active story heading into early 2026, with the company continuing to execute on one of the most ambitious clean energy buildouts in the Midwest. The company has been advancing its multi-year solar and wind expansion program across Iowa and Wisconsin, adding generating capacity that is increasingly reflected in its earnings and regulatory filings. Management has remained vocal about its commitment to the energy transition, and regulators in both states have continued to provide a constructive backdrop for capital recovery on those investments.

On the financial side, Alliant reported full-year net income of $810 million and earnings per share of $3.16, which represents a meaningful step forward from prior-year results and positions the company at the higher end of the guidance range it outlined at the start of fiscal 2025. Operating cash flow came in at approximately $1.17 billion, a notable improvement that reflects the growing contribution of previously commissioned renewable assets and disciplined expense management across both utility subsidiaries.

The January 2026 dividend declaration, raising the quarterly payment to $0.535 from $0.507, marked another milestone in the company’s now 22-year streak of consecutive annual dividend increases. That increase of roughly 5.5% is consistent with the pace management has communicated to shareholders and aligns with the company’s earnings growth trajectory. Shares have responded positively to the combination of earnings delivery and dividend momentum, pushing to within a dollar of their 52-week high near the time of this update.

Key Dividend Metrics

💰 Forward Dividend Yield: 2.83%

🔁 5-Year Average Dividend Yield: 3.12%

📈 Dividend Growth (Trailing Annual): ~5.5%

🧮 Payout Ratio: 62.97%

📅 Most Recent Dividend Payment: $0.535 (paid January 30, 2026)

⏳ Annual Dividend: $2.06 per share

Dividend Overview

Alliant’s current dividend yield of 2.83% sits modestly below the company’s five-year average yield of around 3.12%, which is a natural consequence of the stock’s strong price appreciation over the past year. The annual dividend now totals $2.06 per share, up from $2.028 per share in the prior year following the January 2026 increase to $0.535 per quarter. That raise continues a long tradition of measured, consistent increases that compound meaningfully over time for long-term holders.

What makes Alliant’s dividend picture particularly attractive is the improvement in the payout ratio. The current reading of 62.97% is well below the 71% level from a year ago, driven by earnings per share growth outpacing dividend increases. That healthier coverage ratio gives the company more room to sustain and extend its growth streak without leaning on financing to fund the payout. For income investors, a declining payout ratio paired with a growing dividend is one of the most reassuring combinations available in the utility space.

Alliant does carry a meaningful debt load, as is typical for capital-intensive regulated utilities. That debt supports a multi-year investment program in renewables and grid infrastructure, and the regulated nature of the business ensures those costs can be recovered through rate structures. As long as the regulatory relationships in Iowa and Wisconsin remain constructive, this financing structure does not pose a material threat to dividend continuity.

Dividend Growth and Safety

Alliant’s 22-year consecutive dividend growth streak is one of the more understated achievements in the utility sector. The company has managed to grow its payout through interest rate cycles, commodity swings, weather disruptions, and a full energy transition in progress, without a single year of stagnation. The most recent increase, from $0.507 to $0.535 per quarter, represents approximately 5.5% growth and is consistent with the 5% to 7% earnings growth target management has communicated publicly.

From a safety standpoint, the fundamentals are sound. The payout ratio has improved to just under 63%, which is well within the comfort zone for a regulated utility and leaves meaningful room for continued increases without straining the balance sheet. The company’s beta of 0.67 is low by market standards, which reflects the defensive character of regulated utility earnings and the relative insulation Alliant has from broader economic volatility.

Free cash flow remains negative at approximately -$1.37 billion, which is a function of the company’s aggressive capital expenditure program rather than any weakness in the underlying business. Regulated utilities routinely operate with negative free cash flow during buildout phases because the capital being deployed today is recovered through rate base growth over the coming years. Operating cash flow of $1.17 billion is strong and more than sufficient to cover the $2.06 annual dividend on a per-share basis. Once the current investment cycle begins to moderate, free cash flow should improve materially.

Return on equity of 11.30% reflects a company generating competitive returns on its capital base, and institutional ownership remains high, indicating that long-term investors continue to view LNT as a core holding. Alliant’s dividend story is built on regularity and reliability, not headline yield, and by those measures it continues to deliver exactly what income investors expect from it.

Chart Analysis

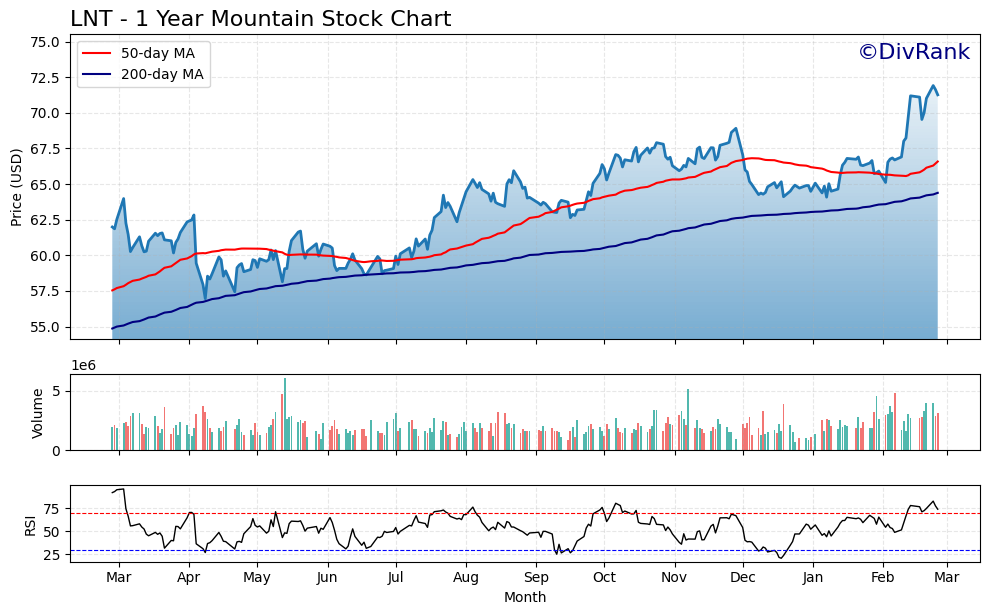

Alliant Energy has put together a strong run over the past twelve months, climbing from a 52-week low of $56.96 to its current price of $71.26, a gain of roughly 25% from trough to present. That kind of recovery in a regulated utility reflects a meaningful shift in sentiment, likely driven by easing rate expectations and renewed appetite for yield-oriented names. The stock is now within striking distance of its 52-week high of $71.91, sitting just 0.9% below that level, which tells you the path of least resistance has been decisively upward for most of the past year.

The moving average picture reinforces that bullish trend structure. LNT is trading above both its 50-day moving average of $66.58 and its 200-day moving average of $64.38, and the 50-day has crossed above the 200-day to form what technicians call a golden cross. For dividend investors who are less concerned with short-term trading signals, the golden cross matters primarily because it confirms that the intermediate trend is aligned with the longer-term trend. There is no ambiguity in the current setup: price, the 50-day, and the 200-day are all stacked in the correct bullish order.

The one metric that warrants attention is the RSI, which sits at 73.96. A reading above 70 places the stock in technically overbought territory, and at nearly 74, LNT has moved into a range where short-term pullbacks or consolidation become more statistically common. This does not imply the trend is broken or that the stock is a poor long-term holding, but an investor looking to establish or add to a position may find a more favorable entry point if the stock digests recent gains and retreats toward the $66 to $68 range near the 50-day moving average.

For dividend investors, the overarching takeaway is that LNT is in a technically healthy uptrend with strong trend confirmation, but the near-term timing of new purchases deserves some patience. Those already holding the stock can take comfort in the price action, which provides a cushion well above key support levels. Anyone building a new position should keep the elevated RSI in mind and consider scaling in rather than committing a full position at current levels just a fraction below the 52-week high.

Cash Flow Statement

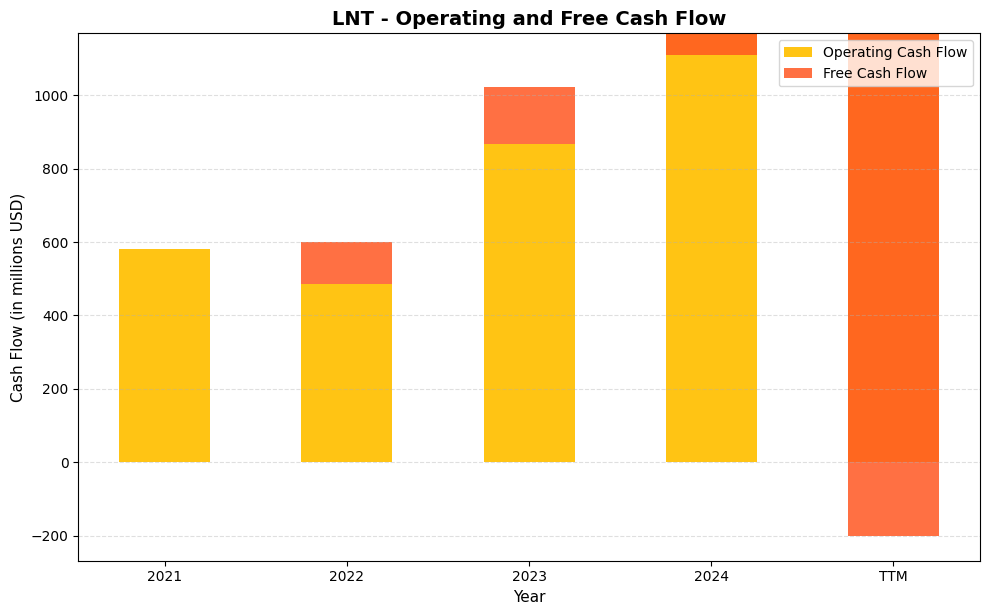

Alliant Energy’s operating cash flow trajectory tells a compelling story for income investors. The company generated $582.0 million in operating cash flow in 2021, saw a dip to $486.0 million in 2022, and then accelerated sharply to $867.0 million in 2023 and $1,167.0 million in 2024, with trailing twelve-month operating cash flow holding essentially flat at $1,169.0 million. That near-doubling of operating cash generation between 2022 and 2024 reflects the earnings power of a regulated utility executing on a substantial capital investment cycle. Free cash flow, however, tells a more nuanced story. After posting $114.0 million in 2022 and $155.0 million in 2023, free cash flow turned negative at $57.0 million in 2024 and deteriorated sharply to negative $1,369.3 million on a trailing twelve-month basis. For dividend sustainability, this means the dividend is not being covered by residual cash after capital expenditures, which is a common and broadly accepted condition for regulated utilities that fund growth spending through a combination of operating cash flow, debt, and equity issuance rather than free cash flow alone.

The context behind these numbers matters considerably for shareholders. Regulated utilities like Alliant Energy routinely run negative free cash flow during periods of elevated infrastructure investment, and the sharp deterioration in the TTM figure points directly to an accelerating capital expenditure program tied to grid modernization, renewable energy buildout, and rate base expansion across Iowa and Wisconsin. The operating cash flow base of over $1.1 billion gives the company meaningful capacity to service its dividend, which consumed roughly $400 million annually in recent years, while leaning on its investment-grade balance sheet to finance the remainder of its capital program. The 2022 to 2023 jump in operating cash flow, from $486.0 million to $867.0 million, suggests improving regulatory recovery and stronger utility earnings feeding through to cash. Shareholders should view the negative free cash flow not as a red flag but as the expected financial signature of a utility actively building the infrastructure that supports future rate base growth, earnings expansion, and continued dividend increases over a multi-year horizon.

Analyst Ratings

Analyst sentiment on Alliant Energy has shifted notably more constructive compared to a year ago, with the current consensus landing at a buy rating across the 11 analysts actively covering the stock. That represents a meaningful upgrade in the aggregate view relative to the hold consensus that characterized coverage through much of 2024 and into early 2025.

The mean 12-month price target of $74.09 implies approximately 4% upside from the current price of $71.26, which is a more modest premium than is typical for a buy-rated utility. That compressed upside reflects the stock’s strong run toward its 52-week high of $72.26 rather than any deterioration in the fundamental outlook. The high target of $80.00 suggests that the more optimistic analysts see room for meaningful further appreciation if earnings continue to track above the midpoint of guidance and regulatory outcomes remain favorable. The low target of $67.00 is modestly below the current price, representing a cautious minority view that the recent re-rating may have run ahead of near-term fundamentals.

With no specific analyst actions available for attribution in this update, the overall picture from the target range and consensus is one of a well-regarded utility that has earned a more positive appraisal from the investment community, trading close to fair value after a strong 12-month price move. Analysts appear to be acknowledging Alliant’s execution on earnings, its renewable buildout progress, and the improving payout ratio as reasons to remain constructive even with limited near-term price target upside from current levels.

Earning Report Summary

Strong Fiscal 2025 Results

Alliant Energy wrapped up fiscal 2025 with a notably strong performance, reporting earnings per share of $3.16 against full-year revenue of approximately $4.36 billion and net income of $810 million. That EPS figure lands above the upper end of the $3.15 to $3.25 guidance range management communicated following the fiscal 2024 close, representing a meaningful year-over-year step up from the $3.04 earned in 2024. The improvement was driven by continued rate base growth from commissioned renewable assets, disciplined operating and maintenance expense management, and constructive outcomes from rate proceedings in both Iowa and Wisconsin.

Operating cash flow of $1.17 billion was a standout number, reflecting the growing cash generation capability of the renewable fleet and improved working capital dynamics. Profit margins improved to 18.57%, which is solid for a regulated electric utility and suggests that cost recovery mechanisms are functioning as intended within the regulatory frameworks governing both utility subsidiaries.

Renewable Buildout Driving Results

A central theme in the fiscal 2025 results is the accelerating earnings contribution from Alliant’s solar and wind investments. The multi-year buildout program has been adding generating capacity that is now fully reflected in rate base and earning regulated returns, which is translating into the kind of predictable earnings growth the company has targeted. Depreciation and financing costs remain elevated as a consequence of that capital activity, but the earnings growth has been sufficient to absorb those headwinds and still deliver EPS expansion.

Committed to Shareholder Returns

Alliant marked its 22nd consecutive year of dividend increases with the January 2026 declaration, reinforcing the company’s long-standing commitment to rewarding shareholders alongside its capital investment program. Management continues to target 5% to 7% annual earnings growth, a range that is consistent with the dividend growth pace and suggests the payout ratio will remain at a healthy and sustainable level for the foreseeable future. The overall picture from the most recent results is one of a company executing cleanly against a well-communicated strategy.

Management Team

Alliant Energy’s leadership is headed by CEO Lisa Barton, who assumed the role in January 2024 after serving as the company’s president and chief operating officer. Barton has built her career around clean energy strategy and utility operations, and her tenure so far has been marked by continued execution on the renewable buildout and a steadiness in stakeholder communication that investors and regulators alike have responded to positively. Former CEO John Larsen remains engaged with the company as executive chairman, providing continuity on long-term strategic direction and key relationships.

The broader executive team brings deep expertise across the disciplines that matter most for a utility at this stage of its evolution. Barbara Tormaschy continues to lead sustainability and regulatory policy efforts, which are central to Alliant’s ability to recover capital costs through rate structures in Iowa and Wisconsin. Michael Luhrs oversees customer strategy and forward-looking operational planning. Together, this leadership group has maintained the consistency and discipline that have defined Alliant’s management culture for more than two decades of uninterrupted dividend growth.

The board of directors includes professionals with backgrounds spanning finance, energy infrastructure, and technology. Their oversight function adds an additional layer of governance accountability as the company navigates one of the most capital-intensive phases of its history.

Valuation and Stock Performance

Alliant Energy shares are trading at $71.26 as of this update, just $1 below the 52-week high of $72.26 and well above the 52-week low of $57.09. That range captures a meaningful re-rating over the past year as investors have returned to regulated utilities with renewed conviction, attracted by stable earnings growth and the relative predictability of rate-based business models in an uncertain macroeconomic environment.

The trailing price-to-earnings ratio of 22.55 places Alliant in line with or at a slight premium to regulated electric utility peers, which is reasonable given the company’s track record of dividend growth and its above-average execution on the energy transition. Price-to-book of 2.50 against a book value per share of $28.52 reflects the market’s willingness to pay a premium for Alliant’s regulated earnings stream and the quality of its asset base. Market capitalization stands at approximately $18.3 billion.

With a consensus analyst price target of $74.09, there is modest upside from current levels, suggesting the stock is approaching fair value after its run. The return on equity of 11.30% is healthy for the sector and supports the case that Alliant is generating competitive returns on its growing rate base. For investors entering or adding to a position at current prices, the valuation is not stretched, but the margin of safety is narrower than it would have been six to twelve months ago. The primary case for owning LNT here rests on the dividend growth trajectory and the compounding effect of a well-managed utility over a multi-year horizon.

Risks and Considerations

The most prominent ongoing risk for Alliant is the sustained negative free cash flow driven by its capital expenditure program. At approximately -$1.37 billion on a trailing basis, the gap between operating cash flow and total capital needs is significant, and the company remains reliant on capital markets access to fund its investment plan. Any material deterioration in debt market conditions or a widening of credit spreads could increase financing costs and put pressure on earnings growth projections.

Regulatory risk is always present for a utility that depends on rate proceedings to recover its investments, and Alliant is no exception. While the regulatory environments in Iowa and Wisconsin have historically been constructive, any shift in the political landscape or a more adversarial posture from regulators in future rate cases could delay cost recovery, compress allowed returns, or create uncertainty around pending capital projects. The company’s ability to earn its authorized rates of return is foundational to the dividend growth strategy.

Interest rate sensitivity remains a consideration given the size of Alliant’s debt load. Higher-for-longer interest rates increase refinancing costs as existing debt matures and can also make utility dividend yields look comparatively less attractive to income investors, which in turn can weigh on the stock’s valuation multiple. The stock’s 2.83% yield is already below its five-year average, meaning there is less cushion on the yield side if rates were to move higher from here.

Weather variability is a routine but real factor in utility earnings. Milder-than-normal temperatures reduce electricity demand and can create headwinds relative to financial plan assumptions, as Alliant experienced in prior periods. Finally, execution risk on the renewable buildout itself deserves mention. Large-scale infrastructure projects carry the potential for cost overruns, supply chain delays, or permitting complications, any of which could push capital recovery timelines to the right and affect near-term earnings.

Final Thoughts

Alliant Energy enters 2026 in a position of genuine strength. Earnings per share of $3.16 exceeded expectations, operating cash flow improved substantially, and the company extended its dividend growth streak to 22 consecutive years with a 5.5% increase. The stock’s move toward its 52-week high reflects a market that has recognized this execution and is willing to pay a fair multiple for it.

For dividend growth investors, LNT offers a compelling combination of characteristics: a regulated earnings base that is largely insulated from economic cyclicality, a payout ratio that has improved to a more comfortable level, and a management team with a clear and credibly communicated capital allocation strategy. The yield of 2.83% is not the highest available in the utility sector, but when paired with a consistent 5% to 7% annual dividend growth target and a 22-year track record of delivering on that commitment, it represents a durable and compounding income stream that serves long-term portfolios well. Investors who are comfortable with the current valuation and the inherent capital intensity of this business phase will find a well-managed, strategically sound utility continuing to evolve in the right direction.