Updated 2/25/26

AGCO Corporation (AGCO) is a global manufacturer of agricultural machinery and precision ag technology, operating brands like Fendt, Massey Ferguson, and Valtra. Based in Georgia, the company serves a broad international market, with a strong presence in Europe and South America. After a difficult stretch marked by sharply lower farm equipment demand and significant restructuring, AGCO has returned to profitability, posting $726 million in net income on revenue of roughly $10.1 billion over the trailing twelve months. Free cash flow of $850 million remains robust, and the balance sheet continues to support a steady dividend. With a current yield of 0.85% and a payout ratio of just 11.9%, the dividend is exceptionally well covered, leaving ample room for future increases. Analyst sentiment is cautious, with a consensus hold rating and a mean price target modestly below the current share price, though the stock has recovered substantially from its 52-week lows.

Recent Events

AGCO’s most visible recent development has been the substantial recovery in its share price, which climbed from a 52-week low of $73.79 to trade near $133.92 as of late February 2026, approaching the 52-week high of $143.78. That kind of move reflects improving investor confidence in the company’s restructuring progress and its ability to return to meaningful profitability after a painful 2024. The sale of the Grain and Protein segment, which weighed heavily on reported earnings in the prior year, is now largely in the rearview mirror, allowing management to focus on its core precision agriculture and premium equipment businesses.

On the operational front, AGCO has continued to push forward with its “Farmer-First” strategy, investing in digital tools, smart farming platforms, and high-margin Fendt equipment across European and South American markets. These segments have held up better than North America through the ag cycle downturn, and management has pointed to them as the foundation for margin recovery. The company also paid its most recent regular quarterly dividend of $0.29 per share on February 13, 2026, consistent with the pattern maintained throughout 2024 and 2025. Short interest has declined meaningfully from prior levels, now sitting at roughly 2.9 million shares, suggesting the heavy skepticism that characterized the 2024 bear case has faded somewhat as fundamentals have improved.

Key Dividend Metrics

📈 Forward Dividend Yield: 0.85%

💵 Annual Dividend Rate: $1.16 per share

🎯 Payout Ratio: 11.90%

⏳ 5-Year Average Yield: 0.84%

🗓️ Most Recent Dividend Paid: February 13, 2026 ($0.29/share)

📉 Free Cash Flow: $850 million (trailing twelve months)

Dividend Overview

AGCO’s dividend yield of 0.85% sits right in line with its five-year average of 0.84%, which tells you that the stock’s recovery has brought valuation back toward historical norms. The yield isn’t the headline attraction here, and income-focused investors should understand going in that AGCO is not a high-yield name. What it does offer is an extremely conservative payout structure: the $1.16 annual dividend per share represents just 11.9% of trailing twelve-month earnings per share of $9.75, making it one of the better-covered dividends in the industrials space.

The regular quarterly payment has been $0.29 per share dating back to mid-2023, and AGCO has maintained that cadence without interruption through the earnings volatility of 2024 and into 2026. That consistency matters. It also bears mentioning that AGCO paid a special dividend of $2.50 per share in May 2024, likely tied in part to proceeds from the Grain and Protein segment divestiture. That kind of capital return behavior, while irregular, signals that management is willing to share windfalls with shareholders rather than simply accumulate cash. Investors should not build that into their income expectations, but it is a positive signal about capital allocation philosophy.

Dividend Growth and Safety

The regular quarterly dividend has held at $0.29 per share since August 2023, meaning there has been no increase to the base payout over that period. At first glance that might seem like stagnation, but context matters. AGCO navigated a severe industry downturn, reported a net loss in its prior fiscal year, completed a major divestiture, and absorbed significant restructuring charges, all while keeping the dividend intact. The fact that management didn’t reach for a cut is itself a meaningful signal of commitment to the income program.

Now that earnings have recovered sharply, with EPS of $9.75 against a $1.16 annual dividend, the payout ratio of just 11.9% creates substantial headroom for dividend growth going forward. Free cash flow of $850 million dwarfs the estimated annual dividend cost of roughly $86 million, meaning AGCO could more than double its dividend tomorrow and still be running at a comfortable payout ratio. Operating cash flow of $988 million further reinforces the picture. The dividend is not under any financial stress, and the more relevant question for growth investors is simply when management will choose to accelerate the increase cadence now that the business has stabilized. Return on equity of 16.69% and a profit margin of 7.21% suggest the underlying business quality supports a more generous payout over time.

For dividend safety purposes, AGCO scores very well. The combination of low absolute payout, strong free cash flow, and recovered earnings creates a buffer that most industrial dividend payers would envy. The primary risk to the dividend is not financial capacity but rather a renewed and prolonged downturn in global farm equipment demand, which could compress earnings again before management has the chance to grow the payout meaningfully.

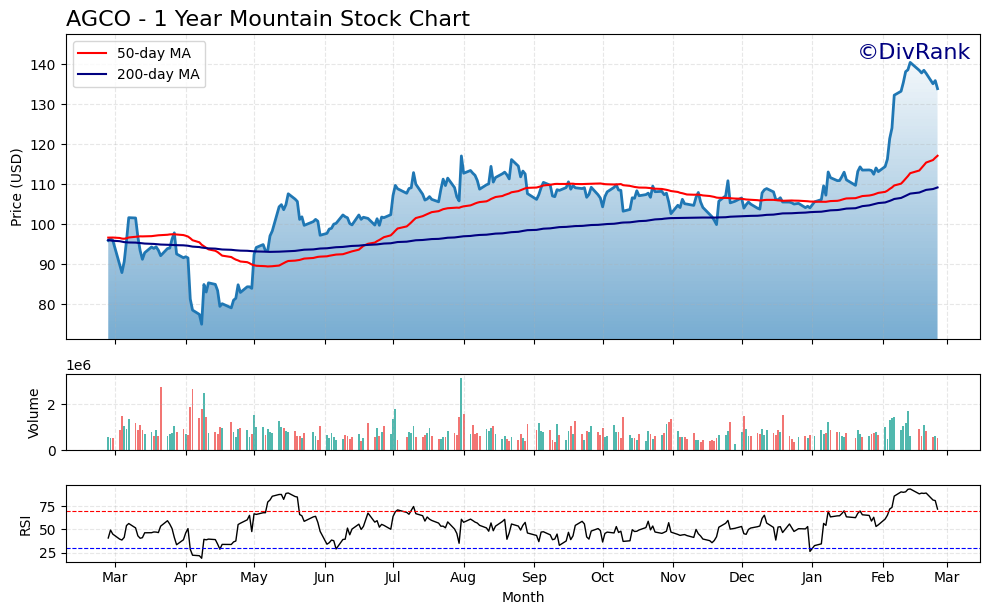

Chart Analysis

AGCO’s price action over the past year tells a compelling recovery story. The stock carved out a 52-week low of $75.00 before staging a sustained advance that has carried shares to $133.92, representing a gain of roughly 78.6% off that trough. That kind of move off a meaningful low reflects a genuine shift in sentiment rather than a routine bounce, and the fact that AGCO is now trading within 4.7% of its 52-week high of $140.49 suggests the bulls have maintained consistent control throughout the recovery. For a dividend growth investor, a stock that reclaims lost ground in an orderly, trending fashion is far more encouraging than one that spikes and fades.

The moving average picture reinforces that constructive read. AGCO’s 50-day moving average of $117.14 has crossed above the 200-day moving average of $109.21, producing a classic golden cross formation that technical analysts treat as a confirmation of a longer-term uptrend. Current price sits comfortably above both averages, which means those moving averages are now functioning as a layered support structure beneath the stock. A pullback toward the $117 area would represent roughly an 12.5% retreat from current levels but would still leave the broader uptrend intact, giving income investors a potential re-entry zone if they are waiting for a better entry on yield.

Momentum is elevated, with the RSI reading coming in at 71.89, which places AGCO just inside overbought territory on a standard 14-period basis. That reading deserves respect but not panic. Stocks in strong uptrends can sustain RSI readings above 70 for extended periods, particularly when the move is being driven by a fundamental re-rating rather than speculative excess. That said, an RSI at this level does reduce the immediate margin of safety for new buyers, and some near-term consolidation or a modest pullback to work off the overbought condition would actually be a healthy development before the next leg higher.

For dividend investors, the technical setup is broadly favorable. The trend is up, the moving averages are aligned bullishly, and price is pressing toward multi-month highs. The primary caution is the stretched RSI, which argues against chasing the stock aggressively at current levels. Investors already holding AGCO for its dividend income have little reason for concern based on the chart alone. Those looking to initiate or add to a position may find better risk-adjusted entry points on a pullback toward the rising 50-day moving average, where the combination of technical support and a slightly improved yield would present a more attractive setup.

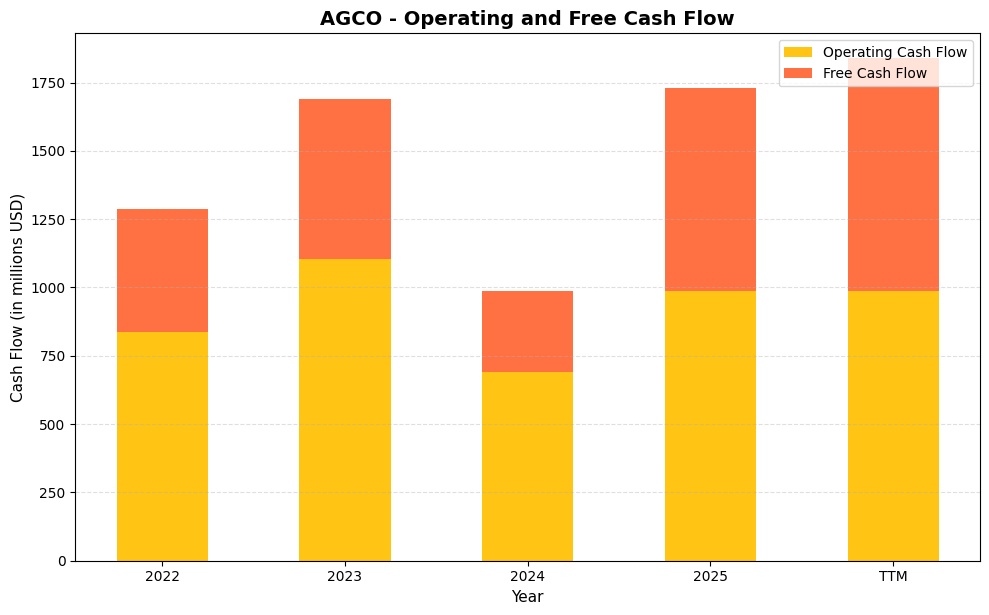

Cash Flow Statement

AGCO’s cash generation profile tells an encouraging story for dividend investors, even if the path has not been perfectly linear. Operating cash flow climbed from $838.2 million in 2022 to a strong $1.10 billion in 2023, then pulled back to $689.9 million in 2024 as the agricultural equipment cycle softened and destocking pressures weighed on the business. The recovery in 2025 has been meaningful, with operating cash flow rebounding to $988.1 million and free cash flow surging to $740.2 million, a figure that compares very favorably to the $296.6 million posted in 2024. On a trailing twelve month basis, free cash flow sits at $850.0 million, which provides substantial coverage for AGCO’s dividend obligations and signals that the 2024 trough was cyclical rather than structural.

Looking across the full period, what stands out is how capital efficiency has improved even as revenue has fluctuated. Free cash flow conversion relative to operating cash flow has strengthened notably in the most recent period, with TTM free cash flow representing roughly 86 cents of every dollar of operating cash flow generated, compared to a conversion rate closer to 54 cents on the dollar in 2022. That improvement reflects disciplined capital expenditure management as AGCO works through its portfolio restructuring and focuses investment on its highest return businesses. For dividend growth investors, the trajectory from 2024 into 2025 is the more important signal, as it demonstrates the company’s ability to rebuild cash generation quickly when operating conditions stabilize, which underpins confidence in both dividend maintenance and the potential for future increases.

Analyst Ratings

The analyst community currently holds a consensus view of hold on AGCO, based on the assessments of 14 analysts covering the stock. The mean twelve-month price target of $128.57 sits modestly below the current trading price of $133.92, which is an unusual setup and suggests the analyst community on balance sees limited near-term upside from current levels after the stock’s substantial recovery from the $73.79 low. The range of targets is wide, spanning from a low of $102.00 to a high of $152.00, which reflects genuine disagreement about how quickly the North American farm equipment cycle will recover and whether AGCO’s precision ag investments will accelerate margin expansion.

With the stock trading above the analyst consensus target, the burden of proof now falls on AGCO to deliver earnings results that justify the current multiple. The bears in the analyst community, reflected in targets near $102, likely believe the stock has gotten ahead of the fundamental recovery and that North American demand remains challenged. The bulls, with targets at $152, are probably pricing in a more accelerated cycle turn and margin improvement from the Fendt and digital agriculture segments. For dividend investors, the practical takeaway is that near-term capital appreciation may be limited, but the income stream is secure and the case for gradual dividend growth over the next two to three years is reasonable.

Earning Report Summary

A Return to Profitability

AGCO’s most recent trailing twelve-month financials show a company that has executed its way back to meaningful profitability after a painful 2024. Revenue of $10.1 billion is down from the $11.66 billion peak but reflects the leaner, more focused business that remains after the Grain and Protein divestiture. Net income of $726 million and EPS of $9.75 represent a substantial turnaround from the prior year’s net loss, demonstrating that the restructuring actions and cost discipline implemented by management are producing results.

Profit margins of 7.21% are respectable for an agricultural equipment manufacturer operating through a demand trough, and return on equity of 16.69% suggests the business is generating solid returns on the capital it deploys. The recovery in operating cash flow to nearly $988 million is perhaps the most reassuring data point, confirming that the income statement improvement is translating into real cash rather than accounting-driven gains. With a price-to-earnings ratio of 13.74, the stock is trading at a modest premium to pure cyclical peers but still at a discount to broader industrials, which seems reasonable given the earnings recovery trajectory.

CEO’s Take and Looking Forward

Eric Hansotia has maintained a consistent strategic message throughout the downturn and into the recovery: invest in Fendt’s premium positioning, expand digital farming solutions, and capture the long-term shift toward precision agriculture that is transforming how large-scale farming operations make equipment decisions. That narrative is becoming easier to tell now that the Grain and Protein distraction has been removed and the balance sheet is in better shape. Management has been disciplined about costs during the downturn, and that discipline is now showing up in margins as revenue stabilizes.

The forward outlook will depend heavily on whether North American and European farmer sentiment improves enough to accelerate equipment replacement cycles. Crop prices, interest rates for farm financing, and government support programs in key markets will all shape demand in 2026. Management has signaled confidence in the medium-term demand recovery while maintaining realistic near-term guidance. The strategic bet on high-margin, technology-enabled equipment and recurring digital revenue streams gives AGCO a path to improved profitability even if the volume recovery is gradual.

Management Team

AGCO’s leadership continues to be guided by Eric Hansotia, who serves as Chairman, President, and CEO. Since taking the helm in 2021, Hansotia has navigated the company through one of the more challenging periods in agricultural equipment history, completing the Grain and Protein divestiture, managing through a steep demand downturn, and maintaining investment in the precision agriculture capabilities that represent AGCO’s long-term competitive differentiation. His operational background and long-term orientation have been evident in the measured way management has handled cost structure and capital allocation through the cycle.

Damon Audia, the Senior Vice President and Chief Financial Officer, has been central to maintaining financial discipline during the revenue compression years and has overseen the return to strong free cash flow generation as conditions have improved. His focus on cash flow quality and conservative capital allocation has kept the dividend secure and the balance sheet manageable. Roger Batkin continues to lead legal and ESG responsibilities, while Kelvin Bennett oversees engineering, a function that is increasingly critical as AGCO competes on technology differentiation through its Fendt and precision agriculture platforms. The leadership team has demonstrated the kind of steady, unsentimental management that dividend investors tend to appreciate in cyclical industrial businesses.

Valuation and Stock Performance

AGCO’s stock has staged a dramatic recovery, rising from a 52-week low of $73.79 to the current price of $133.92, putting it within striking distance of the 52-week high of $143.78. At the current price, the stock carries a price-to-earnings ratio of 13.74 and a price-to-book ratio of 2.28 against book value per share of $58.84. Those multiples are not demanding for a company generating $9.75 in EPS and nearly $850 million in free cash flow, but they do reflect a meaningful re-rating from the distressed valuations that characterized the 2024 lows.

The market cap of approximately $10 billion against trailing free cash flow of $850 million implies a free cash flow yield of roughly 8.5%, which provides a reasonable margin of safety even if the ag cycle softens again modestly. The stock’s beta of 1.17 indicates it moves with some amplification relative to the broader market, which is consistent with its cyclical exposure. With the analyst consensus target at $128.57, the current price of $133.92 sits modestly above the mean target, suggesting the easy money from the recovery trade may have already been made. That said, if management delivers on earnings in 2026 and demand conditions improve, the high-end target of $152 represents meaningful additional upside from current levels. Investors entering at today’s price are buying a recovered business at a fair multiple rather than a distressed one at a deep discount.

Risks and Considerations

Agricultural equipment demand is inherently cyclical, and AGCO has limited ability to insulate itself from the broader swings in farm income, crop prices, and capital spending sentiment that drive replacement cycles. North American and Western European markets have been soft for several consecutive years, and while there are signs of stabilization, a meaningful volume recovery is not guaranteed in the near term. If commodity prices weaken or interest rates on farm equipment financing remain elevated, the demand recovery could be slower and shallower than current earnings expectations assume.

Currency volatility represents a persistent risk for a company that generates the majority of its revenue outside the United States. Unfavorable movements in the euro, Brazilian real, or other key currencies can compress reported revenue and earnings even when underlying unit demand is stable. Geopolitical disruptions in key markets, particularly in South America and Eastern Europe, add another layer of uncertainty to the international revenue base that is difficult to hedge fully.

The strategic pivot toward precision agriculture and digital farming platforms is promising over a multi-year horizon but requires sustained capital investment in a competitive environment that includes both established equipment manufacturers and well-funded technology entrants. Farmers in many markets have been slow to adopt subscription-based digital tools, and the timeline for those investments to generate meaningful recurring revenue remains uncertain. If adoption rates disappoint or competitors close the technology gap, the margin expansion thesis that supports current valuation could take longer to materialize.

Finally, while the dividend is extremely well covered at the current level, the payout has not grown since mid-2023 despite the sharp improvement in earnings and cash flow. Investors hoping for dividend growth need management to prioritize increasing the regular quarterly payment, which is not guaranteed given that capital could alternatively be directed toward debt reduction, acquisitions, or additional special dividends at management’s discretion.

Final Thoughts

AGCO enters 2026 as a meaningfully different company than it was eighteen months ago. The divestiture is complete, profitability has returned, free cash flow is robust, and the stock has recovered sharply from levels that reflected genuine earnings distress. The $9.75 in EPS against a $1.16 annual dividend creates one of the most conservative payout structures in the industrials space, and the $850 million in free cash flow gives management considerable flexibility to grow the dividend, return additional capital, or invest in the precision agriculture capabilities that represent the company’s long-term competitive moat.

The primary challenge from here is one of execution and patience. The stock’s recovery has been substantial, and with the consensus analyst target sitting below the current price, near-term capital appreciation may require positive earnings surprises to materialize. For income investors, the more relevant story is whether management begins to grow the base dividend now that earnings have recovered, and whether the precision agriculture investments eventually produce the higher-margin, recurring revenue streams that would justify a premium multiple.

AGCO is not a set-and-forget high-yield holding, but for investors who understand the agricultural cycle and appreciate a conservatively managed industrial franchise with global reach and real technology optionality, it remains a name worth owning and watching closely as the cycle evolves through 2026 and beyond.