Updated 2/25/26

AES Corporation (NYSE: AES) is a global power generation and utility company operating across 14 countries, with a growing focus on renewable energy. Trading around $16.37 as of February 2026, the stock has recovered substantially from its 52-week low of $9.46, though it remains just below the high of $16.78. With a dividend yield of 4.33% and a conservative payout ratio of 46.08%, AES continues to offer meaningful income while investing heavily in clean energy infrastructure. The company has posted improved net income and strong operating cash flow, with leadership maintaining its commitment to renewable project expansion. Despite ongoing capital intensity, elevated debt levels, and regulatory complexity across its global footprint, AES is executing a long-term strategy built around sustainability, backed by a seasoned management team and a disciplined approach to financial management.

Recent Events

AES has spent much of the past year clawing back from a bruising stretch that sent shares near $9.46, and the recovery to the $16 range reflects a meaningful shift in investor sentiment. The company has continued advancing its renewable energy buildout, with management reaffirming commitments to growing its contracted power capacity across solar, wind, and battery storage platforms. Progress on its multi-gigawatt pipeline has been central to the recovery narrative, as investors have grown more confident that the capital being deployed into these projects will generate durable returns.

On the corporate front, AES has maintained its dividend through this period of transition, with the most recent quarterly payment of $0.176 per share paid on January 30, 2026, consistent with the prior three quarters. The company has also continued its strategy of refinancing and managing its debt obligations as it works to bring new capacity online. Leadership has focused investor communications on the progress of its renewables EBITDA growth targets and cost efficiency programs, keeping the long-term strategy front and center even as short-term market conditions remained choppy through much of 2025.

Short interest in AES stands at roughly 19.6 million shares, a figure worth watching given the stock’s proximity to its 52-week high. Still, the broader trend over the past several months has been one of gradually improving sentiment as execution on renewable targets has continued and the utility sector has attracted renewed interest from income investors.

Key Dividend Metrics

📈 Dividend Yield: 4.33%

💰 Dividend Rate: $0.70 annually

🧮 Payout Ratio: 46.08%

📅 Last Dividend Paid: $0.176 per share (January 30, 2026)

📆 Most Recent Prior Payment: $0.176 per share (October 31, 2025)

💵 EPS: $1.53

These metrics reflect a company maintaining a reliable income stream with a payout ratio that, while higher than a year ago, still leaves room to sustain and grow the dividend over time.

Dividend Overview

At a current yield of 4.33%, AES sits comfortably within the income-generating utility space, offering investors a meaningful return relative to broader market averages. The yield has compressed from the elevated levels seen when the stock was trading near its 52-week low, which is actually a positive signal: it reflects price appreciation rather than any deterioration in the underlying payment.

The quarterly dividend has held at $0.176 per share across the past four payments, consistent through all of 2025 and into the January 2026 payment. Prior to that, the company paid $0.173 per quarter throughout most of 2024, and $0.166 per quarter through mid-2023. That gradual staircase upward, while modest, demonstrates a clear commitment to growing the dividend rather than holding it flat indefinitely.

The payout ratio of 46.08% sits in a more typical range for a utility company compared to the unusually low sub-30% reading from a year ago, largely because EPS of $1.53 reflects current earnings against that $0.70 annual distribution. This remains a comfortable level of coverage, giving management flexibility to maintain the dividend through capital investment cycles without straining the income statement.

Profitability has improved in the trailing period, with net income reaching approximately $1.08 billion and a profit margin of 8.74%. Return on equity stands at 5.11% and return on assets at 2.27%, numbers that are modest but consistent with a capital-intensive utility navigating an aggressive buildout phase.

Dividend Growth and Safety

The dividend history for AES tells a story of deliberate, incremental growth. Starting at $0.166 per quarter in mid-2023, the company stepped up to $0.173 in early 2024 and then to $0.176 in early 2025, where it has remained through the most recent January 2026 payment. Over roughly two and a half years, that represents a cumulative increase of about 6%, which is not aggressive by dividend growth standards but reflects management’s balancing act between income delivery and capital reinvestment.

The safety picture is reasonably solid. The 46.08% payout ratio provides adequate cushion against earnings variability, and operating cash flow of nearly $3.91 billion is more than sufficient to cover the annual dividend obligation, which totals roughly $500 million against the current share count. That operating cash flow figure is actually a notable improvement over prior periods and signals that AES’s core business is generating real cash regardless of the heavy capital outflows on the investment side.

Free cash flow remains deeply negative at approximately -$3.69 billion, which continues to reflect the scale of capital expenditures tied to renewable energy projects. This is a structural feature of the company’s current phase rather than a sign of operational distress, but it does mean AES continues to rely on external financing to fund its growth agenda. Investors should monitor whether the returns on that capital spending begin to close the gap between operating and free cash flow in coming years.

Institutional ownership remains strong, which supports confidence in the dividend’s continuity. AES has shown no inclination to cut the payment even through periods of stock price pressure and earnings volatility, and the gradual upward trend in the quarterly rate reinforces management’s stated commitment to rewarding income investors alongside its growth strategy.

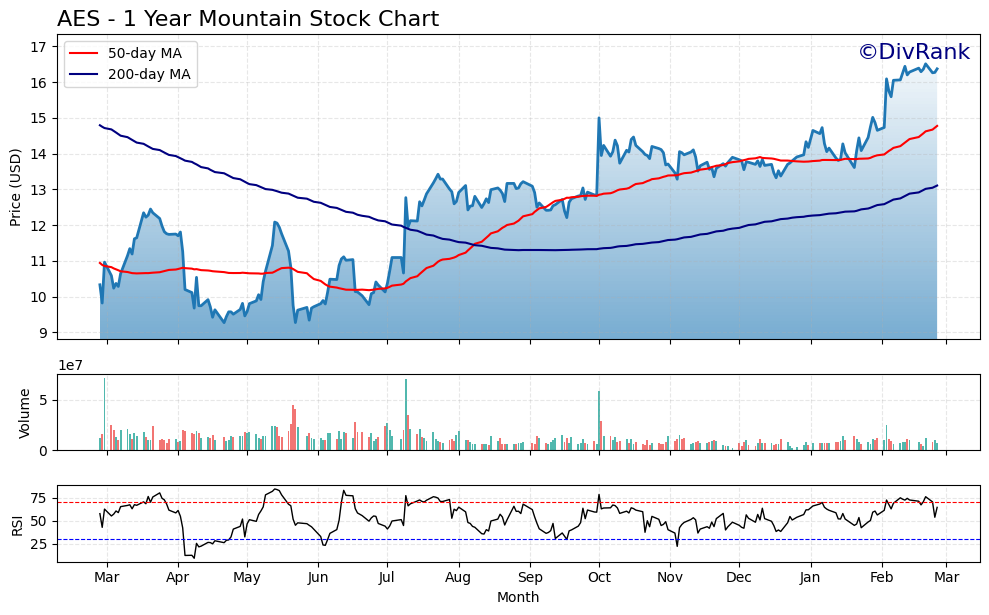

Chart Analysis

AES has staged a remarkable recovery over the past twelve months, climbing from a 52-week low of $9.27 to its current price of $16.37, a gain of roughly 76% from trough to present. That kind of price appreciation in a utility-adjacent power company is unusual, and it reflects a significant shift in market sentiment toward the stock after what was clearly a period of deep pessimism. The shares are now trading just 0.85% below their 52-week high of $16.51, which means the stock is essentially pressing against the top of its annual range. For dividend investors who may have been accumulating shares during the downturn, the positioning here is encouraging, though anyone initiating a new position today is entering near peak-year prices rather than at a discount.

The moving average picture is cleanly bullish. AES is trading above both its 50-day moving average of $14.77 and its 200-day moving average of $13.11, and the 50-day has crossed above the 200-day to form what technicians call a golden cross. This configuration signals that intermediate-term momentum has confirmed the longer-term trend reversal, and it tends to attract systematic and momentum-oriented buyers who can provide additional price support. The spread between the current price and the 200-day average is now more than three dollars, which reflects how far and how fast the recovery has moved. That gap alone warrants some patience from income investors considering a fresh entry, as a pullback toward the $14.50 to $15.00 zone would offer a meaningfully better starting yield without disrupting the broader uptrend.

The RSI reading of 64.62 places AES in firm bullish territory without yet triggering the kind of overbought signal that typically appears above 70. Momentum is clearly on the side of the bulls at this stage, and there is still a narrow band of room for the stock to continue advancing before the technical picture becomes stretched. That said, an RSI approaching 65 while the price sits within 1% of a 52-week high is a combination that historically precedes consolidation or modest short-term weakness more often than sustained breakouts. Dividend investors should interpret this not as a sell signal, but as a reason to size any new position conservatively and leave room to add if the stock digests its gains.

Taken together, the chart tells the story of a stock that has done most of its heavy lifting and is now in a consolidation zone near annual highs. The trend is positive, the moving average structure is supportive, and momentum remains constructive without being reckless. For long-term income investors, the technical backdrop is favorable for holding existing positions and watching for any dips toward the 50-day moving average as a more attractive entry point. The stock’s ability to hold above $14.77 on any near-term pullback would be an important confirmation that the recovery has genuine staying power rather than simply reflecting a short-covering bounce.

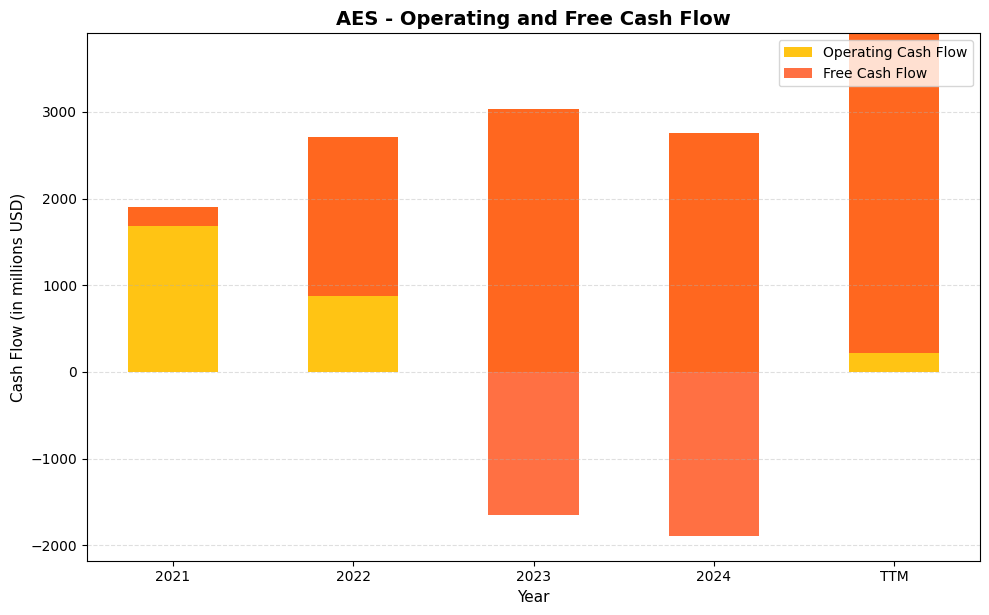

Cash Flow Statement

AES has delivered meaningful growth in operating cash flow over the review period, rising from $1,902.0 million in 2021 to a TTM figure of $3,906.0 million, a gain of more than 100% in just a few years. That trajectory speaks to the underlying earnings power of the business and provides a credible foundation for dividend payments. Free cash flow, however, tells a more complicated story. It has been deeply negative throughout the entire period, moving from -$214.0 million in 2021 to -$4,640.0 million in 2024 before improving modestly to -$3,689.9 million on a TTM basis. For dividend sustainability purposes, this means AES is funding its payout and its capital program through a combination of operating cash flow, asset sales, and external financing rather than through retained free cash flow. That is a structure common among capital-intensive utilities and power companies, but it does require investors to pay close attention to balance sheet leverage and financing conditions.

The widening gap between operating cash flow and free cash flow from 2021 through 2023 reflects an aggressive capital expenditure cycle as AES accelerated investment in renewable energy infrastructure, a strategy that consumed an additional $4,476.0 million in capital between those two years alone. The partial narrowing of the free cash flow deficit in the TTM period, even as operating cash flow reached its highest recorded level at $3,906.0 million, suggests the most intensive phase of that buildout may be cresting. For long-term shareholders, the calculus centers on whether the assets being constructed will generate sufficient contracted cash flows to eventually close that gap. If the renewable portfolio ramps as expected, the operating cash flow base should continue to grow, gradually reducing the reliance on external capital to bridge the shortfall. Until free cash flow turns meaningfully positive, the dividend remains supported by cash flow from operations and financial management rather than organic surplus generation, a distinction that carries real relevance for income investors assessing long-term payout security.

Analyst Ratings

The analyst community holds a consensus buy rating on AES, with 12 analysts contributing to the current coverage picture. The mean 12-month price target sits at $15.54, which is modestly below the current trading price of $16.37, suggesting that at current levels the stock has largely priced in the recovery that analysts were anticipating when the shares were trading closer to their lows. The range of targets is wide, spanning from a low of $8.50 to a high of $23.00, which reflects the genuine dispersion of opinion about how quickly AES’s renewable buildout will translate into earnings and cash flow improvement.

The fact that the stock now trades above the analyst consensus target is worth paying attention to. It does not necessarily mean the stock is overvalued, but it does suggest that near-term upside from analyst upgrades or target raises may be the more likely catalyst for further appreciation than simply closing a gap to consensus. The high end target of $23.00 implies meaningful upside remains possible if execution on the renewables pipeline accelerates and the broader utility sector continues to attract income-seeking capital. For now, the buy consensus reflects a generally positive long-term view tempered by an acknowledgment that the stock has already done significant work off its lows.

Earnings Report Summary

AES Corporation’s most recent earnings reflected a company continuing to work through the tension between near-term capital demands and a long-term strategy that is gradually proving itself out. Full-year revenue came in at approximately $12.09 billion, and net income reached roughly $1.08 billion, representing a substantial improvement in profitability compared to the prior year. EPS of $1.53 on a reported basis reflects the progress being made, even as free cash flow remains pressured by the company’s aggressive investment posture.

Profitability Continues to Improve

The improvement in net income to over $1 billion is a meaningful milestone for AES, which has been working to demonstrate that its renewable energy investments are beginning to pay off in the income statement. Operating cash flow of nearly $3.91 billion is particularly encouraging, as it shows the core business generating real cash at a rate that comfortably covers both the dividend and a significant portion of ongoing operating needs. The profit margin of 8.74% is modest but directionally positive.

Renewables Remain the Growth Engine

Management has continued to highlight progress on the renewable energy front as the central pillar of the company’s growth thesis. AES has been advancing its contracted gigawatt pipeline across solar, wind, and battery storage, and the EBITDA contribution from renewables has grown as projects come online. The company’s ability to sign long-term power purchase agreements provides revenue visibility that supports both the dividend and the case for further investment in clean energy infrastructure.

Capital Allocation and Cost Discipline

The CFO team has maintained focus on cost efficiency programs alongside the growth agenda, recognizing that financial discipline is essential when the balance sheet is carrying the weight of a major infrastructure buildout. Progress on operating cost reduction targets has been part of the earnings narrative, and management has continued to frame the negative free cash flow as a transitional feature tied to a defined investment cycle rather than an open-ended drain. Investors will be watching closely for signs that capital expenditures begin to moderate as major projects reach completion.

Navigating External Pressures

AES has continued to manage operational challenges across its international footprint, including weather-related disruptions in South America and the ongoing complexity of operating under multiple regulatory regimes. Leadership has been consistent in framing these as manageable headwinds rather than structural obstacles, and the improved profitability in the most recent period supports that characterization. The global energy transition remains a tailwind for the company’s strategic direction even as near-term execution requires careful navigation.

Management Team

AES Corporation is led by President and CEO Andrés Gluski, who has held the role since 2011 and has been the architect of the company’s pivot toward renewable energy and operational efficiency. Under his tenure, AES has transformed from a more traditional global power company into one increasingly defined by its clean energy ambitions, with a contracted pipeline spanning multiple continents and technology platforms. Gluski has been the primary voice communicating the long-term strategy to investors and has maintained consistency in that message through periods of significant market volatility.

Supporting him is a leadership team that brings deep operational and financial expertise to the challenges of running a capital-intensive global business. Chief Operating Officer Ricardo Falú oversees the company’s broad international operations, ensuring execution across a diverse set of markets and regulatory environments. Chief Financial Officer Stephen Coughlin manages the financial strategy, balancing the demands of a major infrastructure investment program against the need to maintain financial flexibility and honor the company’s commitment to its dividend. Together, this team has navigated a difficult period for utility stocks and positioned AES for the next phase of its energy transition story.

Valuation and Stock Performance

As of February 25, 2026, AES shares trade at $16.37, representing a remarkable recovery from the 52-week low of $9.46 and placing the stock just below its 52-week high of $16.78. The rebound of more than 70% from the low reflects a meaningful shift in how investors are pricing the company’s renewable energy strategy and improving profitability. The stock’s beta of 0.97 suggests it now moves roughly in line with the broader market, a notable change from the elevated volatility that characterized its selloff period.

Valuation metrics have naturally reset higher with the price recovery. The P/E ratio of 10.70 is still quite modest for a utility with a credible growth narrative, and even compared to the broader market, it suggests the stock is not expensively priced on an earnings basis. The price-to-book ratio of 3.02 is higher, but utilities with significant infrastructure assets and contracted revenue streams often command book value premiums. The current analyst consensus price target of $15.54 sits modestly below the current price, meaning the stock has outrun near-term analyst expectations, though the high end target of $23.00 indicates that longer-term bulls see substantially more room.

The market cap of approximately $11.66 billion reflects the scale of the recovery and the renewed investor interest in AES as both an income vehicle and a beneficiary of the global energy transition. For investors who added shares during the period of maximum pessimism near the lows, the total return including dividends has been compelling. The question now is whether the stock can sustain this level and push higher as renewable EBITDA growth and cost savings flow more visibly through the income statement.

Risks and Considerations

The capital intensity of AES’s renewable energy buildout remains a central risk for investors to monitor. The company continues to spend aggressively on solar, wind, and battery storage projects, which has kept free cash flow deeply negative at roughly -$3.69 billion. If financing conditions tighten, interest rates remain elevated, or contracted project returns disappoint, the gap between operating cash flow and capital spending could create pressure on the balance sheet and, eventually, on the dividend.

Debt levels continue to be a meaningful concern. AES carries a substantial debt load relative to its equity base, and while the company has managed its obligations through careful refinancing and liquidity management, the balance sheet leaves limited room for error. A significant economic downturn, a rise in borrowing costs, or a disruption to revenue from its international operations could constrain financial flexibility in ways that would force difficult capital allocation decisions.

Regulatory and geopolitical risk is inherent to a company operating across 14 countries under varied energy policy regimes. Changes in government priorities, permitting delays, shifts in renewable energy incentives, or currency depreciation in key markets can all affect project economics and earnings visibility. South America in particular has historically presented operational challenges through weather events and regulatory complexity, and that exposure has not diminished as the company continues to operate and invest there.

Finally, with the stock having recovered sharply to near its 52-week high and now trading above the analyst consensus price target, the near-term risk-reward profile is less asymmetric than it was a year ago. Investors entering at current prices are paying for a recovery that has largely already happened, which means execution on the renewables pipeline and continued earnings improvement will need to deliver to justify the current valuation and support further appreciation.

Final Thoughts

AES has traveled a long distance over the past year, from deep uncertainty near $9.46 to a recovery that has brought the stock within striking distance of its 52-week high. The improvement in operating cash flow, the stability of the dividend through a turbulent period, and the continued progress on renewable energy contracts all point to a company that is executing on its stated strategy with reasonable fidelity. The income story remains intact at a 4.33% yield with a manageable payout ratio, and the earnings trajectory supports confidence in the dividend’s continuity.

The more nuanced question at current prices is what the next leg of the thesis looks like. The easy recovery trade has largely played out, and what remains is a longer-term story about whether AES can translate its renewable energy investments into the kind of EBITDA and free cash flow growth that would justify meaningfully higher valuation multiples. Management has consistently pointed toward that outcome, and the improving operating cash flow suggests the foundation is being built.

For income investors with a multi-year horizon, AES offers a reasonable combination of yield, gradual dividend growth, and exposure to the structural tailwind of global clean energy demand. The risks are real and warrant ongoing attention, particularly around debt and capital allocation. But the company’s leadership, contracted pipeline, and improving financial results make it a credible name in the utility income space as it continues its transition into a cleaner energy future.