Dividend investors seeking defensive income with a recognizable consumer staples franchise have long kept Clorox Company (NYSE: CLX) on their radar. The company’s portfolio of cleaning, household, food, and personal care brands has historically generated resilient cash flows through economic cycles, and its 46-year streak of consecutive dividend increases cements its Dividend Aristocrat status. At a current price of $126.24 and a yield of 3.90%, CLX sits meaningfully below its 52-week high of $159.04, prompting fresh questions about whether the pullback represents an opportunity or a warning sign for income-focused portfolios.

Company Overview

Clorox is one of the most recognized consumer staples companies in the United States, with flagship brands including Clorox bleach and disinfecting products, Glad trash bags, Hidden Valley dressings, Burt’s Bees personal care, and Fresh Step cat litter. As a consumer defensive business, Clorox benefits from predictable, recurring demand that tends to hold up during economic stress. The company generated $6.76 billion in revenue over the trailing twelve months and reported net income of $755 million, a meaningful improvement in profitability compared to the loss-heavy period that followed the 2023 cyberattack and operational disruptions. Management has been executing a multi-year cost savings and portfolio streamlining effort, and the early results of those initiatives are beginning to show in the income statement.

Recent Events

Clorox’s most significant recent development has been the continued recovery arc following the devastating cyberattack in August 2023 that disrupted operations, cost the company hundreds of millions in lost sales, and weighed heavily on earnings for several subsequent quarters. By fiscal year 2025, management had largely restored operational continuity and rebuilt retailer relationships strained during the supply disruption period. The company’s IGNITE strategy, which focuses on streamlining the brand portfolio, investing in innovation, and expanding margins through efficiency programs, has gained traction and is now producing measurable results in both gross margin recovery and free cash flow generation.

On the portfolio management front, Clorox has continued evaluating its brand mix, with investor attention focused on whether the company will pursue divestitures of lower-margin or non-core segments to sharpen its focus on household cleaning and health and wellness categories. The company also refreshed several product lines under the Clorox and Pine-Sol brands to address evolving consumer preferences for efficacy-forward cleaning solutions, particularly as post-pandemic hygiene habits remain somewhat elevated compared to pre-2020 baselines. Meanwhile, cost inflation across packaging, logistics, and raw materials has moderated from peak levels, giving Clorox incremental pricing and margin flexibility heading into the back half of its fiscal year.

Key Dividend Metrics

- 💰 Annual Dividend: $4.96 per share

- 📈 Dividend Yield: 3.90%

- 📊 Payout Ratio: 80.52%

- 🔁 Last Dividend Paid: $1.24 per share (January 28, 2026)

- 📅 Payment Frequency: Quarterly

- 🛡️ Consecutive Dividend Increases: 46+ years (Dividend Aristocrat)

- 💵 Free Cash Flow: $1.00 billion

- 📉 Beta: 0.61

Dividend Overview

Updated 2/25/26. Clorox currently pays a quarterly dividend of $1.24 per share, bringing the annualized dividend to $4.96 per share. At the current stock price of $126.24, that translates to a dividend yield of 3.90%, which is well above the company’s historical average and reflects the meaningful price decline from the $159.04 high reached within the past 52 weeks. The payout ratio stands at 80.52% based on trailing EPS of $6.08, a substantial improvement from the unsustainable levels above 130% that characterized the post-cyberattack period when earnings had collapsed. While 80% is still on the higher end for a consumer staples company, it is no longer a red-flag figure given the trajectory of earnings recovery and the strength of free cash flow generation, which reached approximately $1.0 billion over the trailing twelve months.

Free cash flow coverage of the dividend is a more reassuring picture than the earnings-based payout ratio alone suggests. With $984 million in operating cash flow and free cash flow of roughly $1.0 billion, Clorox generates ample cash to service its $4.96 per share annual dividend across approximately 122 million diluted shares, implying total annual dividend payments in the range of $600 to $610 million. That leaves a meaningful cushion for debt service, capital investment, and opportunistic share repurchases, reinforcing confidence that the dividend is not at imminent risk despite the elevated payout ratio on an earnings basis.

Dividend Growth and Safety

Clorox’s dividend growth over the past several years has been deliberate rather than aggressive, which is appropriate given the financial pressures the company navigated following the cyberattack. Looking at the recent dividend history, the per-share quarterly payment increased from $1.18 in April 2023 to $1.20 in August 2023, held at $1.20 through most of 2024, then stepped up to $1.22 in August 2024, and most recently moved to $1.24 per share beginning in August 2025, a level that has been maintained through the January 2026 payment. These incremental increases are modest in absolute terms, but they reflect management’s continued commitment to the dividend growth streak even during a period of financial reconstruction, which is a meaningful signal of intent for long-term income investors.

The annualized dividend of $4.96 represents an approximately 1.6% increase over the prior $4.88 level, a conservative but positive step. Dividend safety has improved considerably as earnings have recovered, with EPS rising to $6.08 on a trailing basis and free cash flow providing more than adequate coverage. The key variable for future dividend growth acceleration is the pace of the IGNITE strategy’s margin improvements. If Clorox can push operating margins sustainably above current levels and continue reducing operating costs, the payout ratio will compress further, creating headroom for more meaningful dividend increases in the years ahead. For now, dividend safety appears solid and the streak of annual increases remains intact.

Chart Analysis

Clorox shares have staged a meaningful recovery over the past year, climbing from a 52-week low of $96.36 to the current price of $126.24, a gain of roughly 31% off the trough. That kind of bounce reflects a market that spent much of the year repricing CLX after a period of significant operational and sentiment pressure, and the stock has clearly found renewed buying interest as investors reassess the company’s earnings trajectory. Still, the current price sits about 16% below the 52-week high of $150.23, which means the recovery, while real, remains incomplete. The price action over the trailing twelve months tells a story of a stock working its way back from a deep oversold condition rather than one riding a fresh breakout to new highs.

The moving average picture is mixed, and dividend investors should read it carefully. CLX is trading above both its 50-day moving average of $110.05 and its 200-day moving average of $115.78, which confirms that near-term and intermediate-term momentum are both positive on an absolute basis. However, the 50-day moving average remains below the 200-day moving average, a configuration technically known as a death cross, which signals that the longer-term trend structure has not fully repaired itself. A golden cross, where the 50-day crosses back above the 200-day, would represent a more convincing technical confirmation that the recovery has legs. Until that crossover occurs, the chart is best described as a stock in recovery mode rather than one in a confirmed uptrend.

The RSI reading of 70.79 places CLX right at the threshold of overbought territory, which warrants some attention for investors considering adding to a position at current levels. Momentum has clearly been strong in the near term, and a reading this elevated after a 31% rally off the lows suggests the stock may need time to consolidate recent gains before the next leg higher can develop sustainably. This does not imply an imminent collapse, but it does suggest that chasing the stock at this precise moment carries more short-term price risk than entering during a pullback toward the $115 to $118 range, where the 200-day moving average and recent support overlap.

For dividend investors, the chart presents a nuanced setup. The recovery from the lows is encouraging and suggests the worst of the selling pressure has passed, which matters for anyone who owns CLX primarily for its income stream and long-term capital preservation. The unresolved death cross and elevated RSI argue against aggressive new buying right now, but neither condition undermines the fundamental income thesis for investors already holding shares. Patience here is likely rewarded, as a pullback toward the moving averages would offer a more favorable risk-adjusted entry point while preserving the opportunity to benefit from what appears to be a genuine, if still developing, price recovery.

Cash Flow Statement

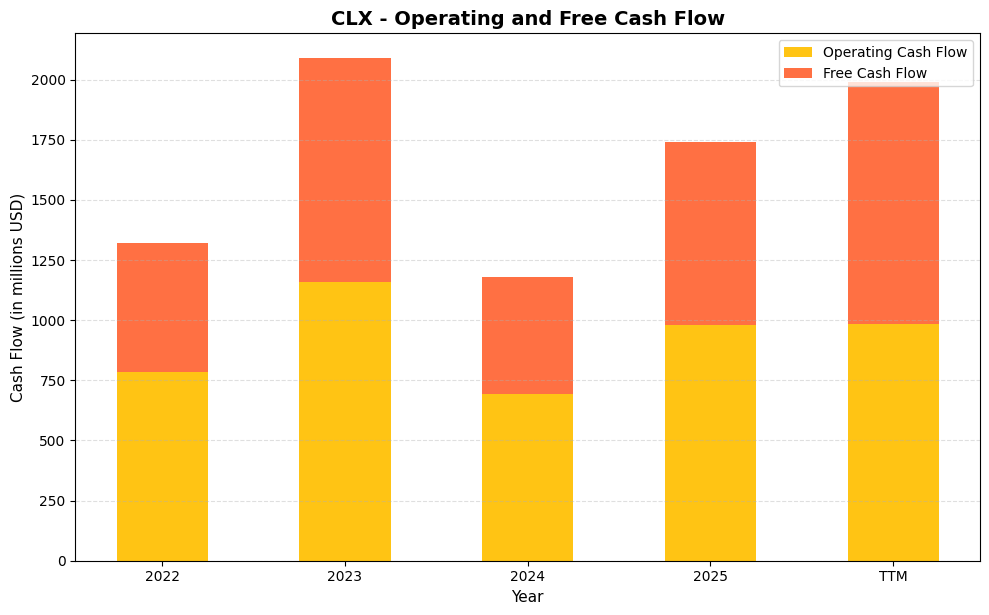

Clorox’s cash generation has been anything but linear, and that volatility is worth understanding in detail before drawing conclusions about dividend sustainability. Operating cash flow peaked at $1,158.0M in fiscal 2023, a strong rebound year following the $786.0M reported in 2022, but then pulled back sharply to $695.0M in 2024 before recovering to $981.0M in 2025. The TTM figure of $984.0M confirms that recovery has held. Free cash flow tells a similar story, moving from $535.0M in 2022 to $930.0M in 2023, then contracting to $483.0M in 2024, and climbing back to $761.0M in 2025. The TTM free cash flow of $1,004.4M is the standout number here, actually exceeding the TTM operating cash flow figure, which reflects a period of relatively lean capital expenditure. Clorox’s annual dividend commitment runs roughly in the $550M to $580M range, and against a TTM free cash flow above $1.0B, the payout looks well covered. The 2024 trough, when free cash flow compressed to $483.0M, was the one year where dividend coverage became genuinely tight, and that context matters for investors who want to stress-test the income stream.

Zooming out across the four-year window, the pattern that emerges is a business with solid underlying cash generation capacity but meaningful year-to-year swings tied to working capital movements, input cost cycles, and the lingering aftermath of Clorox’s well-documented 2023 cyberattack, which disrupted operations and created an unusual earnings and cash flow profile for fiscal 2024. Capital efficiency has improved materially on a TTM basis, with the gap between operating and free cash flow narrowing as capital expenditure moderates relative to prior reinvestment cycles. For dividend growth investors, the core takeaway is that Clorox’s free cash flow floor, even in a down year like 2024, remained positive and capable of funding the dividend without requiring debt issuance for that purpose alone. The 2025 recovery and the TTM trajectory both suggest the business has returned to a more normalized level of cash conversion, which supports management’s ability to sustain the current payout and, over time, resume modest dividend growth consistent with Clorox’s long history as a Dividend Aristocrat.

Analyst Ratings

Wall Street’s current consensus on Clorox is a hold, reflecting a broadly cautious but not bearish view among the 17 analysts who actively cover the stock. The mean price target of $123.47 sits slightly below the current trading price of $126.24, which is an unusual configuration that technically implies modest downside to consensus even as the stock trades near the middle of its 52-week range. The wide dispersion between the low target of $94.00 and the high target of $163.00 tells the real story: analysts are genuinely divided on whether Clorox’s earnings recovery has legs or whether the stock’s pullback from its highs already prices in the improving fundamentals.

Bears in the analyst community point to the premium valuation relative to peers, the still-elevated payout ratio, and ongoing competitive pressures in the household products category as reasons to remain on the sidelines or actively avoid the stock. Bulls anchor their higher targets on the continued progress of the IGNITE cost savings program, the expectation that further margin expansion will drive EPS growth meaningfully above current levels, and the defensive characteristics of the business that make it attractive in a risk-off environment. With the current price of $126.24 sitting above the mean target of $123.47, investors buying today are effectively pricing in a more optimistic outcome than the average analyst currently endorses, which warrants discipline around position sizing and entry price expectations.

Earnings Report Summary

Clorox’s most recently reported financial results reflect a company that has successfully moved past the acute phase of its post-cyberattack recovery and is now demonstrating operating leverage as revenues stabilize and cost reduction efforts flow through the income statement. Revenue for the trailing twelve months reached $6.76 billion, and net income of $755 million translates to EPS of $6.08, a substantial improvement from the deeply negative earnings figures that characterized the 2023 and early 2024 periods. The profit margin of 11.17% represents a meaningful restoration of the company’s earnings power, though it remains below the 13% to 15% range that characterized Clorox at its pre-disruption best.

Operating cash flow of $984 million and free cash flow of approximately $1.0 billion represent some of the strongest cash generation figures Clorox has reported in recent years and validate the narrative that the core business remains a powerful cash compounder even when headline earnings have been distorted by extraordinary items. Management has been executing against three priorities, which are volume recovery in core cleaning categories, gross margin expansion through pricing and cost efficiency, and reinvestment in brand support and innovation to defend market share against both private label competition and branded rivals. The trajectory of all three metrics improved in the most recent fiscal period, providing a constructive setup for the next earnings announcement. Return on assets of 11.31% confirms that capital deployment is generating adequate returns, and with operating leverage likely to build as revenues grow against a partially fixed cost base, the earnings trajectory appears to favor continued improvement through the balance of fiscal 2026.

Management Team

Clorox has been led by Chief Executive Officer Linda Rendle since September 2020, making her one of the longer-tenured CEOs among major consumer staples companies. Rendle’s tenure has been defined by navigating an extraordinary sequence of operational challenges, including supply chain disruptions during the pandemic demand surge, the 2023 cyberattack that temporarily paralyzed the company’s order management and production systems, and a prolonged period of cost inflation that pressured margins across the portfolio. Her response to these challenges has generally been viewed favorably by long-term investors, with the IGNITE strategy providing a coherent framework for restoring profitability and refocusing the company on its highest-return brands and categories.

Chief Financial Officer Kevin Jacobsen has been a steady presence overseeing the financial recovery, managing the company’s capital allocation priorities including dividend maintenance, debt management, and the cost reduction programs central to the margin restoration effort. The management team’s credibility with income investors rests significantly on their decision to continue raising the dividend, even modestly, through the most difficult stretch of the post-cyberattack period rather than cutting the payment to preserve cash. That decision preserved the Dividend Aristocrat streak and signaled confidence in the eventual earnings recovery, which has since materialized. Going forward, the management team’s most consequential decisions will involve the pace of portfolio rationalization, the level of reinvestment in brand marketing and product innovation, and the pace of debt reduction, all of which carry direct implications for the sustainability and growth trajectory of the dividend.

Valuation and Stock Performance

At $126.24, Clorox trades at a trailing P/E of 20.76, a meaningful compression from the elevated multiples that prevailed when earnings were depressed and the market was pricing in a recovery that had not yet arrived. A P/E of approximately 21 times trailing earnings is roughly in line with the broader consumer staples sector and represents a more reasonable entry point than the stock offered at its 52-week high of $159.04. The 52-week low of $96.66 reflects the depth of pessimism that briefly gripped CLX shares, likely during periods of maximum uncertainty about the pace and completeness of the earnings recovery. The current price sits roughly in the middle of that range, suggesting that the market has moved past the worst-case fears without yet fully pricing in an optimistic recovery scenario.

The negative price-to-book ratio, driven by accumulated share repurchases and intangible assets that have reduced reported book value to negative $1.03 per share, makes book value-based valuation metrics uninformative for Clorox, as is common for many capital-light consumer brands companies that have returned substantial capital to shareholders over decades. The more relevant lens for CLX is a free cash flow yield analysis: with approximately $1.0 billion in free cash flow against a market capitalization of $15.4 billion, the stock offers a free cash flow yield of roughly 6.5%, which is attractive for a business with Clorox’s brand durability and income characteristics. The beta of 0.61 confirms that CLX continues to exhibit below-market volatility, a desirable trait for income investors who prioritize portfolio stability. For long-term dividend investors, the current valuation represents a more compelling entry point than the stock has offered in some time, provided the earnings recovery trajectory is sustained.

Risks and Considerations

The payout ratio of 80.52% remains elevated relative to where a conservatively managed consumer staples company ideally operates, typically in the 50% to 65% range. While the ratio has improved dramatically from the unsustainable levels of the past two years, it leaves limited buffer if earnings were to soften due to a revenue reversal, renewed cost inflation, or further extraordinary disruptions. Income investors should track quarterly earnings reports closely for signs of margin pressure that could push the payout ratio back toward uncomfortable territory.

Clorox carries a meaningful debt load that has accumulated over years of share repurchases, acquisitions, and the extraordinary costs associated with the cyberattack recovery. While operating cash flow and free cash flow are now strong enough to service this debt comfortably, the leverage constrains management’s flexibility and amplifies the earnings sensitivity to interest rate movements. In an environment where interest rates remain elevated compared to the pre-2022 era, the cost of refinancing maturing debt deserves monitoring.

Competitive dynamics in the household products category have intensified, with private label penetration increasing at major retailers as price-conscious consumers trade down and as retailers themselves prioritize higher-margin store brands. Clorox’s pricing power, which was a source of strength during the inflationary period, could face headwinds as branded-versus-private-label price gaps attract greater scrutiny from cost-pressured shoppers. Any volume deterioration in core categories like bleach, disinfecting wipes, or trash bags would flow directly into revenue and earnings pressure.

The current stock price of $126.24 sits above the analyst consensus price target of $123.47, which means that consensus does not currently support further near-term appreciation at this level. Investors entering the position today are buying above where the average sell-side analyst sees fair value, and if earnings disappoint relative to the recovery expectations already embedded in the share price, the downside to the $94.00 low analyst target is substantial. Short interest of approximately 7.6 million shares is not alarming in absolute terms but bears watching as a signal of institutional skepticism about the pace of the recovery narrative.

Final Thoughts: Is Clorox Still a Strong Dividend Stock?

Clorox has navigated one of the most turbulent multi-year stretches in its modern history and has emerged with its dividend streak intact, its earnings recovering, and its free cash flow generation restored to levels that provide genuine comfort for income investors. The current yield of 3.90% on an annualized dividend of $4.96 per share is attractive in both absolute terms and relative to the company’s own history, and the free cash flow coverage of approximately $1.0 billion against total dividend payments of roughly $600 million provides a margin of safety that the earnings-based payout ratio of 80.52% alone does not fully convey.

The investment case for CLX as a dividend holding rests on confidence in continued earnings normalization, which would compress the payout ratio further, accelerate dividend growth from the recent incremental pace, and potentially drive the stock back toward the higher end of its 52-week range. The risks are real, including the competitive environment, the debt load, and a valuation that sits modestly above consensus, but none of them appear sufficient to threaten the dividend in the near term given current free cash flow levels.

For conservative income investors with a multi-year horizon, Clorox at $126.24 offers a more balanced risk-reward proposition than it has in some time. The entry yield of 3.90% provides a meaningful income cushion, the Dividend Aristocrat status reflects decades of commitment to shareholders, and the improving earnings trajectory suggests that the worst of the post-cyberattack disruption is behind the company. Investors should size the position appropriately given the above-average payout ratio and monitor quarterly results for continued progress on margins and debt reduction before adding aggressively to existing holdings.