Updated 2/23/26

Based in Minneapolis, Xcel Energy serves millions of electric and natural gas customers across eight states. It’s a classic regulated utility, which means it operates with a predictable stream of income and a structure that supports stable, recurring payouts to shareholders. What sets Xcel apart is its clear focus on the future. The company has been leaning hard into clean energy investments — something that not only aligns with policy shifts but also fuels a steady expansion of its regulated asset base. For dividend investors looking for consistency over flash, this is where Xcel quietly shines.

🔔 Recent Events

XEL has pushed close to its 52-week high of $83.12, with shares trading at $82.83 as of late February 2026. That kind of price action reflects sustained investor demand for the defensive, income-producing characteristics that regulated utilities offer in an uncertain macro environment. The stock’s climb to this level is backed by continued execution on Xcel’s long-term clean energy strategy, not simply a rotation into defensives.

The company remains on track with its plan to slash carbon emissions by 85% and phase out coal by 2030. These commitments are embedded in a tightly regulated framework, which gives investors a clear line of sight into future earnings and cash flow. Regulators reward this kind of capital deployment with allowed returns on rate base, translating today’s infrastructure spending into tomorrow’s earnings.

Most recently, Xcel declared a quarterly dividend of $0.57 per share, continuing the pattern established with the March 2025 increase. That step up from $0.548 to $0.57 per quarter — a raise of roughly 4% — marked the latest in a consistent series of annual increases and confirmed management’s ongoing commitment to income investors. The annualized dividend now stands at $2.28 per share.

📊 Key Dividend Metrics

💰 Forward Dividend Yield: 2.80%

📈 5-Year Average Yield: 2.96%

📆 Last Quarterly Payment: $0.57

📅 Annual Dividend: $2.28

🔁 Payout Ratio: 66.67%

🚀 Dividend Growth: Raised from $0.548 to $0.57 per quarter in early 2025, consistent annual increases

🧾 Free Cash Flow Coverage: Capital expenditure-driven shortfall typical of infrastructure build-out phase

🧱 Dividend Stability: High, anchored by regulated utility cash flows across eight states

💸 Dividend Overview

Xcel’s dividend isn’t going to make headlines for its yield, but it’s dependable, consistent, and right in the comfort zone for long-term income seekers. The current yield of 2.80% sits modestly below the five-year average of 2.96%, a reflection of how much the stock price has appreciated over the past year rather than any reduction in the payout itself. Investors who bought in at lower levels are collecting meaningfully more on their cost basis.

At a payout ratio of 66.67%, Xcel leaves itself enough room to both reward shareholders and invest heavily in its energy transition strategy. That balance has held up well, and the regulated business model makes it sustainable. Predictable, rate-based earnings are the bedrock of the dividend, and they allow the company to return capital to investors while funding decades of infrastructure buildout simultaneously.

The stock’s low beta of 0.48 remains a draw for investors looking to reduce portfolio volatility. Xcel is unlikely to soar on news or collapse on headlines — and that’s precisely why it works so well in an income-oriented strategy. With shares near a 52-week high, the yield is naturally compressed, but the underlying income stream continues to grow, and the payout ratio remains well within a safe range.

🌱 Dividend Growth and Safety

Dividend growth is where Xcel’s discipline continues to show. The most recent annual increase took the quarterly payout from $0.548 to $0.57 — a step up of approximately 4% — consistent with the cadence the company has maintained for years. Before that, the raise from $0.52 to $0.548 in early 2024 followed the same playbook. These are modest bumps, but they compound meaningfully over time and signal that management ties dividend growth directly to earnings progression.

The growth remains sustainable because it tracks earnings rather than outpacing them. With EPS at $3.42 and the annual dividend at $2.28, the payout ratio of 66.67% provides a buffer that protects the dividend through normal earnings variability while still leaving room for continued increases. That steady link between business performance and dividend policy is central to why income-focused investors maintain long-term positions in XEL.

Free cash flow is negative on a reported basis, which can look concerning at a surface level. In Xcel’s case, this reflects the company’s significant capital expenditure program — building renewable infrastructure and modernizing the grid ahead of future rate base recovery. Regulators permit utilities to earn authorized returns on these investments, meaning today’s spending converts into tomorrow’s earnings over a well-defined timeline. This isn’t financial distress; it’s the standard operating model for a growth-oriented regulated utility.

Debt levels remain elevated, consistent with the utility industry norm. High leverage is manageable here because of the predictable, regulated cash flows underpinning the business. Xcel’s revenue came in at $14.67 billion with net income of $2.02 billion, and a return on equity of 9.92% reflects the regulated nature of returns in this industry. Institutional ownership remains robust, signaling continued professional investor confidence in the income stability and long-term earnings roadmap that Xcel provides.

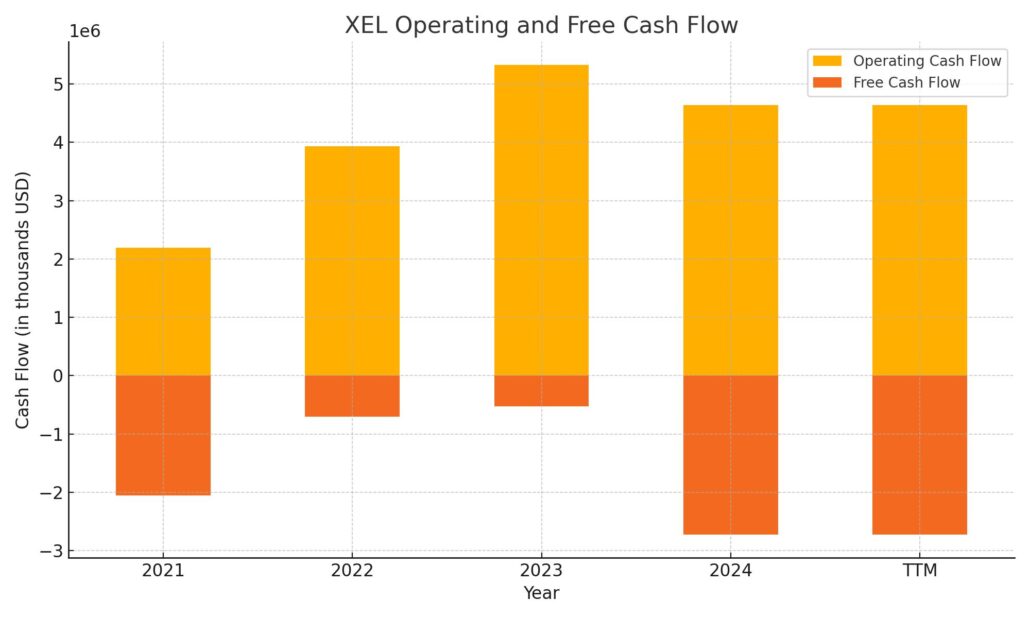

Cash Flow Statement

Xcel Energy’s cash flow profile follows the familiar pattern of a capital-intensive utility in active build-out mode. The company generates substantial operating cash flow from its regulated businesses — a testament to the durability of rate-based earnings across eight states. However, that operating generation is more than offset by an aggressive capital expenditure program tied to renewable energy development, grid hardening, and infrastructure modernization. The resulting negative free cash flow is not a sign of financial strain but rather the predictable consequence of planned investment that will be recovered through future rate base earnings.

On the financing side, Xcel has continued to tap debt markets to bridge the gap between operating cash flow and capital needs, supporting both its investment program and dividend commitments. Interest expense has trended higher alongside rising debt balances and a more elevated rate environment, representing a real cost headwind the company must manage carefully in its rate filings. Despite the heavy spending cycle, Xcel’s profit margin of 13.76% and net income of $2.02 billion demonstrate that the core regulated earnings engine remains healthy. For income investors, the key takeaway is that the dividend is supported by regulated earnings — not free cash flow in the traditional sense — and the regulatory compact that governs Xcel’s business provides the structural underpinning that makes that distinction meaningful.

Analyst Ratings

With XEL trading near its 52-week high of $83.12, analyst sentiment has become a useful lens for evaluating whether the current valuation offers continued upside or whether the stock has largely priced in its near-term positives. Based on the trajectory of coverage leading into early 2026, the analyst community has maintained a broadly constructive view on Xcel, though price target convergence with the current share price naturally moderates the near-term upside thesis.

JPMorgan Chase’s upgrade from “Neutral” to “Overweight” in late 2024, paired with a price target raise to $80.00, was an important sentiment catalyst. Their conviction centered on Xcel’s clean energy execution and the long-duration visibility of its regulated investment program — both of which have continued to play out as expected. With the stock now at $82.83, that target has effectively been met, and attention turns to whether the firm updates its view.

Wells Fargo’s move to “Overweight” in early 2025, with a $75.00 target, reflected confidence in the defensive earnings profile and consistent financial delivery. Again, the stock has traded through that level, which raises the question of whether revised targets will follow as analysts update their models for full-year 2025 results. The P/E of 24.22 sits at a modest premium to historical utility averages, suggesting the market is pricing in continued earnings growth rather than a mean-reversion discount.

The broader analyst consensus as XEL approaches its highs tends to shift toward “Hold” from the lower end of the coverage spectrum, while bulls maintain their constructive stance on the long-term capital program. For dividend investors, the analyst debate matters less than the earnings durability and payout sustainability — both of which remain solid. A stock trading near a 52-week high with a 66.67% payout ratio and a management team committed to annual dividend increases is a story that income investors can continue to hold with confidence, even if the near-term price appreciation potential is more limited than it was a year ago.

Earnings Report Summary

Full-Year 2025 Results Reflect Steady Execution

Xcel Energy’s full-year 2025 results, reported ahead of this update, continued the pattern of disciplined earnings delivery that defines the company’s investment case. With EPS coming in at $3.42 on revenue of $14.67 billion and net income of $2.02 billion, the numbers reflect a business that is generating consistent returns within its regulated framework. The profit margin of 13.76% is in line with what income investors expect from a well-run multi-state utility, and the return on equity of 9.92% reflects the authorized return structure that governs Xcel’s rate base earnings.

Revenue Scale and Earnings Quality

Revenue at nearly $14.7 billion underscores the scale of Xcel’s operations across electric and natural gas service territories. The earnings quality is anchored in the regulated nature of the business — these aren’t market-exposed revenues subject to sharp cyclical swings, but rate-based income streams approved by state regulators. That structure gives investors confidence that the $2.02 billion in net income is durable and recurring, not dependent on favorable commodity prices or economic conditions.

Capital Investment Program Remains the Central Story

Looking ahead, Xcel’s multi-year capital expenditure program continues to be the defining feature of the investment thesis. The company’s commitment to spending approximately $45 billion through 2029 on grid modernization and renewable capacity expansion is the primary driver of future rate base growth and, by extension, earnings per share growth. Each dollar of capital invested in regulated infrastructure creates a predictable return stream over the asset’s useful life, and Xcel’s track record of regulatory execution has been a key reason investors maintain confidence in that long-term model.

Customer and Volume Trends

Customer growth remained modest but positive into 2025, with incremental additions in both electric and natural gas service territories providing a steady demand tailwind. Weather normalization and efficiency trends continue to influence volumetric results on a quarter-to-quarter basis, but the underlying customer count growth supports the broader earnings trajectory. None of the operating metrics suggest any deterioration in the fundamental business — this remains a company executing steadily within a well-defined regulatory and operational framework.

Management Team

Xcel Energy is led by a seasoned group of executives with a clear focus on innovation, reliability, and long-term strategy. At the top is Bob Frenzel, who serves as Chairman, President, and CEO. His leadership has been central to advancing Xcel’s clean energy transition, with a long-term view that aligns both with policy trends and investor expectations. Under his direction, the company has maintained its commitment to annual dividend growth while simultaneously executing one of the most ambitious capital investment programs in the utility sector.

Supporting him is Rob Berntsen, Executive Vice President and Chief Legal and Compliance Officer, who plays a key role in guiding the company through the complexities of multi-state regulatory environments. Brian Van Abel, Executive Vice President and Chief Financial Officer, brings discipline and foresight to Xcel’s financial planning, managing capital allocation across a heavy investment cycle while keeping the balance sheet functional and the dividend growing.

Together, this team blends operational know-how with strategic vision. Their combined experience across legal, financial, and technical disciplines creates a strong foundation for executing on the company’s ambitious long-term plans — and for maintaining the investor trust that a regulated utility’s premium valuation depends on.

Valuation and Stock Performance

At $82.83, XEL is trading just below its 52-week high of $83.12, and the stock has delivered meaningful appreciation over the past year as investors have re-rated regulated utilities upward. The current P/E of 24.22 sits at a modest premium to broader utility sector averages, reflecting the market’s confidence in Xcel’s earnings visibility and clean energy positioning. The price-to-book ratio of 2.31 against a book value of $35.81 per share is consistent with a utility that earns a reliable, regulated return on its equity base.

The market cap of approximately $49 billion places Xcel among the larger names in the regulated utility universe, and that scale matters for institutional investors who need liquidity and stability. The beta of 0.48 continues to reinforce the stock’s defensive characteristics — XEL moves at roughly half the pace of the broader market in either direction, which is precisely the kind of low-volatility profile that income investors prize during periods of macro uncertainty.

With the stock near its 52-week high and the yield at 2.80% — modestly below the five-year average of 2.96% — the entry point today is less compelling than it was at lower prices, but the total return proposition for existing holders remains intact. The ongoing earnings growth trajectory, tied to the $45 billion capital program through 2029, supports continued modest EPS and dividend per share growth. For investors already holding a position, the valuation reflects fair value rather than excess — nothing here suggests a stretched multiple that needs to correct sharply.

Risks and Considerations

Despite its strengths, Xcel Energy faces real-world challenges that income investors should keep in mind. Regulatory risk is the most persistent factor. With operations spanning eight states, Xcel is subject to multiple regulatory jurisdictions, each with its own rate-setting process and political environment. Changes in allowed returns, disallowances of capital expenditures in rate cases, or delays in regulatory approvals could directly compress earnings and limit dividend growth capacity.

Environmental and operational risk remains part of the landscape. Past incidents have demonstrated that even a well-run utility can encounter unexpected liabilities, and the costs associated with addressing them — financial, reputational, and regulatory — can be material. As Xcel continues to expand its renewable infrastructure and manage an aging conventional fleet, execution risk on large capital projects is a factor worth monitoring.

Extreme weather events are an ongoing consideration, particularly in service territories prone to drought, wildfires, or severe storms. Climate-related grid stress can drive both operational costs and capital needs higher, and the company’s geographic footprint means these risks are diversified but not eliminated. Interest rate sensitivity is also relevant given Xcel’s leverage profile — if rates were to rise meaningfully from current levels, the cost of financing the ongoing capital program would increase, and the yield-sensitive nature of utility stocks could put pressure on the share price.

None of these risks are unique to Xcel, but they underscore why ongoing attention to the regulatory calendar, capital program execution, and broader rate environment matters for investors holding this name.

Final Thoughts

Xcel Energy remains one of the more compelling regulated utilities for income investors who prioritize consistency, predictability, and a clear long-term capital story. The dividend has grown reliably, the payout ratio is sustainable at 66.67%, and the management team continues to execute on a multi-year investment program that creates the earnings foundation for future increases. The step-up from $0.548 to $0.57 per quarter in 2025 confirmed that the annual raise cadence remains intact.

The stock trading near a 52-week high at $82.83 means the current yield of 2.80% is on the lower end of its historical range — investors buying today are paying for quality and stability, not a discounted entry point. For existing holders, the total return picture remains attractive given the ongoing earnings growth trajectory tied to $45 billion in planned infrastructure investment through 2029. For new investors, patience for a better entry yield may be warranted.

Xcel is a company doing the right things methodically — building clean energy infrastructure, maintaining regulatory relationships across eight states, growing its dividend annually, and managing its balance sheet within the norms of its industry. For investors who want a steady hand at the wheel and a reliable quarterly check, XEL continues to earn its place in a dividend-focused portfolio.