Updated 2/23/26

Williams-Sonoma, Inc. (WSM) continues to present a compelling case for long-term income investors who appreciate operational excellence wrapped inside a recognizable consumer brand. Known for its premium home furnishing brands like Pottery Barn, West Elm, and its namesake kitchenware stores, Williams-Sonoma has maintained its relevance in a crowded retail space with enviable consistency.

Shares have recovered meaningfully from their prior lows, now trading near $202.43 — well off the 52-week low of $130.07 and approaching the upper end of the 52-week range of $222.00. That kind of recovery reflects renewed investor confidence in the company’s business model and its ability to sustain profitability even amid macroeconomic headwinds. This isn’t a story of speculative momentum — it’s a steady build rooted in performance and shareholder returns.

Recent Events

The headline story coming into early 2026 is the stock’s strong rebound from its lows and the business’s continued demonstration of financial discipline. Revenue for the trailing twelve months reached $7.91 billion, and net income came in at $1.13 billion — a profit margin of 14.3% that remains the envy of most specialty retailers. These aren’t cosmetic numbers propped up by accounting. The company is generating real, high-quality earnings.

Return on equity has climbed to 56.92%, and return on assets sits at 17.87% — exceptional metrics in any sector, let alone retail. Management has continued to run a tight ship on expenses while preserving the brand’s premium positioning. The most recent quarterly dividend payment of $0.66 per share remains consistent with the step-up introduced in April 2025, when the company raised its quarterly payout from $0.57 to $0.66 — a 15.8% increase that sent a clear signal about management’s confidence in the business. Operating cash flow of $1.35 billion and free cash flow of $930 million confirm there is ample firepower to sustain and grow that payment.

Short interest sits at approximately 8.5 million shares, a level worth monitoring but not alarming given the stock’s current trading volume and underlying strength. With a beta of 1.64, WSM moves with some volatility relative to the broader market, but investors with a longer time horizon can look past those swings toward what the income and return profile truly represents.

Key Dividend Metrics

📈 Forward Dividend Yield: 1.18%

💸 Forward Annual Dividend Rate: $2.64

📊 Payout Ratio: 28.11%

📆 Last Ex-Dividend Date: January 16, 2026

🎁 Last Dividend Payment: $0.66 per share

🧮 EPS (TTM): $9.07

💥 Free Cash Flow: $930.4 million

📉 Operating Cash Flow: $1.35 billion

🏦 Return on Equity: 56.92%

Dividend Overview

At 1.18%, Williams-Sonoma’s yield won’t turn heads among investors scanning for high-income names. But that headline number undersells the full picture. What really matters for dividend-focused investors is the security and trajectory of that income stream — and on both fronts, WSM is in excellent shape.

The payout ratio of 28.11% against trailing EPS of $9.07 reflects a company that is paying its dividend with enormous ease. Management raised the quarterly dividend from $0.57 to $0.66 in April 2025, and that new rate has been sustained through the January 2026 payment. That 15.8% raise wasn’t a one-time gesture — it fits the company’s multi-year pattern of meaningful, consistent dividend increases. Looking back at the recent dividend history, the quarterly payment moved from $0.45 in early 2023 to $0.565 in April 2024, then to $0.57 by mid-2024, and finally up to $0.66 starting in April 2025, where it has held steady through the most recent payment.

The low yield relative to broader market alternatives is partly a function of the stock’s price appreciation. Investors who purchased shares at lower price points are enjoying meaningfully better yields on cost. For new buyers at today’s price near $202, the income component is modest, but it comes attached to a company with demonstrated willingness and ability to grow that payment over time.

Williams-Sonoma has also been an active repurchaser of its own shares, which amplifies per-share metrics even when top-line revenue growth is measured. Shareholder-friendly behavior here runs deeper than just the quarterly dividend check.

Dividend Growth and Safety

Dividend safety at Williams-Sonoma is about as solid as it gets for a consumer cyclical name. Free cash flow of $930.4 million against an annualized dividend commitment that represents a fraction of that total gives the company a runway most retailers would envy. Even in a meaningful revenue slowdown, the dividend would remain protected at current payout levels.

Operating cash flow of $1.35 billion is the engine behind all of this. It funds capital expenditures, share repurchases, dividends, and still leaves the balance sheet in healthy shape. The company has consistently demonstrated that it can prioritize shareholder returns without sacrificing operational investment or financial flexibility.

The dividend growth trajectory since 2023 tells a clear story. Starting at $0.45 per quarter in early 2023, the company raised its payout meaningfully at the start of fiscal 2024, bumped it again mid-year, and then delivered a substantial step-up to $0.66 in April 2025. That brings the annualized rate to $2.64 — up significantly from the $1.80 annualized rate of early 2023. Over roughly three years, the dividend has grown by 46.7%, a pace that meaningfully outstrips inflation and rewards long-term holders.

Institutional ownership is close to the high nineties percentile of the float, a signal that sophisticated, research-driven capital remains heavily committed to this name. Insider ownership is modest, but the management team’s track record of capital allocation speaks louder than any insider share count. The combination of strong free cash flow, conservative payout ratios, and a demonstrated willingness to raise the dividend paints a reassuring picture for anyone depending on this income stream.

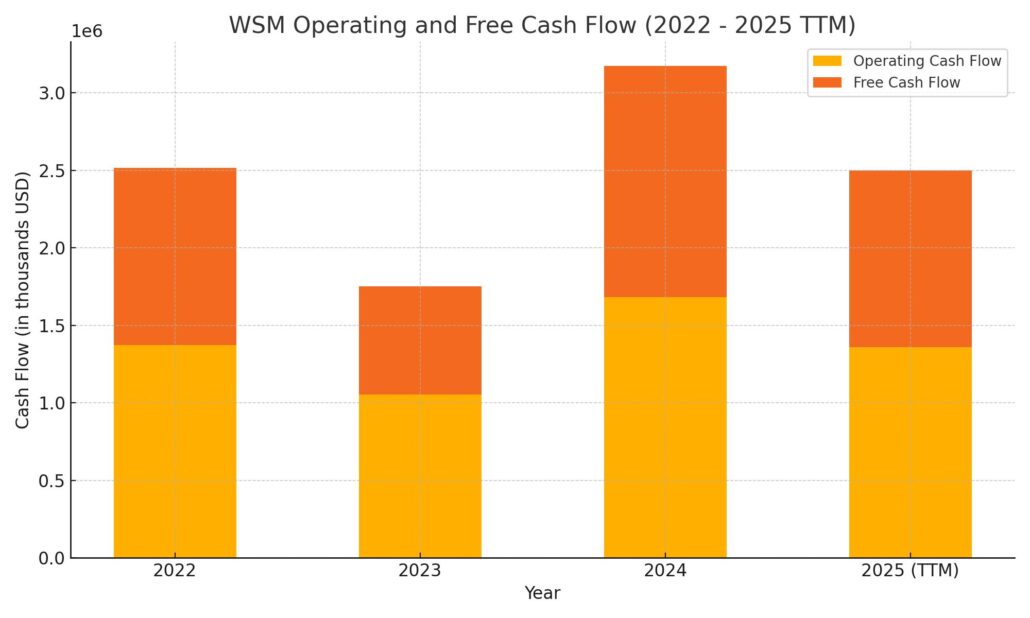

Cash Flow Statement

Williams-Sonoma’s cash flow profile remains one of the most attractive in specialty retail. Trailing twelve-month operating cash flow came in at $1.35 billion, a level that comfortably funds dividend payments, capital expenditures, and share repurchases while still preserving liquidity. Free cash flow of $930.4 million confirms the company’s ability to convert reported earnings into tangible cash — a distinction that matters when evaluating dividend sustainability.

Capital expenditures remain disciplined, with the gap between operating cash flow and free cash flow implying approximately $421 million in capex — reasonable for a retailer investing in its digital infrastructure and store base. The company has continued returning capital to shareholders through buybacks alongside its growing dividend, reflecting a balanced allocation philosophy. Net income of $1.13 billion against operating cash flow of $1.35 billion shows healthy cash conversion, with non-cash charges and working capital movements contributing positively. The overall picture is one of a business that generates cash reliably, spends it thoughtfully, and keeps its financial position strong enough to sustain shareholder returns through varying economic conditions.

Analyst Ratings

Analyst coverage of Williams-Sonoma heading into early 2026 reflects a community that respects the company’s operational track record but remains measured in its enthusiasm at current price levels. With shares trading near $202 and the 52-week high sitting at $222, the stock is not deeply discounted, and most analysts have calibrated their targets accordingly.

The general tone from the analyst community has been one of cautious optimism. Those with constructive views point to the company’s exceptional return on equity above 56%, its ability to sustain high margins in a competitive retail environment, and its consistent dividend growth as evidence that WSM deserves a premium multiple. Critics of the current valuation point to the 22.32x trailing P/E, a price-to-book of nearly 12x, and ongoing macro sensitivity in discretionary consumer spending as reasons to stay on the sidelines rather than chase the stock higher from current levels.

The near-term debate centers on how WSM navigates any softness in housing-related demand and whether its pricing power holds as consumers continue to face cost pressures in other areas of their budgets. Longer-term, the bull case rests on the company’s direct-to-consumer strength, its multi-brand platform, and a management team with a strong history of protecting margins through cycles. Given the company’s profit margin of 14.3% and its free cash flow generation, the fundamental underpinning for the stock remains intact even if near-term upside is more limited than it was at the 52-week lows.

Earnings Report Summary

Williams-Sonoma’s most recently reported financials confirm that the business continues to perform at a high level. Revenue for the trailing twelve-month period reached $7.91 billion, net income came in at $1.13 billion, and earnings per share clocked in at $9.07. A profit margin of 14.3% represents strong execution in a retail segment where many peers struggle to sustain double-digit margins.

Revenue and Profitability

The company’s ability to sustain revenue above $7.9 billion while preserving a 14.3% net profit margin speaks to the effectiveness of its multi-brand strategy and its disciplined approach to pricing. Rather than chasing volume through aggressive discounting, Williams-Sonoma has leaned into its premium positioning — a strategy that protects margins even when unit volumes fluctuate. Return on equity of 56.92% is exceptional and reflects both the profitability of the underlying business and the impact of ongoing share repurchases reducing the equity base.

Cash Generation

Operating cash flow of $1.35 billion and free cash flow of $930.4 million confirm that the earnings quality is high. Cash is flowing in at a pace that fully funds the dividend, supports continued buybacks, and keeps the balance sheet stable. Return on assets of 17.87% indicates the company is deploying its asset base efficiently, which is particularly impressive given the capital-intensive nature of retail operations.

Shareholder Returns

The April 2025 dividend increase to $0.66 per quarter — a 15.8% raise over the prior $0.57 rate — was the headline shareholder-return event of the past year. That payment has been maintained consistently through the January 2026 distribution. Combined with ongoing share repurchases, Williams-Sonoma has continued to demonstrate that returning capital to shareholders is a core priority rather than an afterthought. The annualized dividend of $2.64 represents a 46.7% increase from the $1.80 rate in early 2023, a meaningful acceleration that income-focused investors can appreciate.

Looking Ahead

With EPS of $9.07 and a payout ratio of 28.11%, there is considerable room for further dividend growth without straining the business. The company’s ability to sustain high margins and generate free cash flow well in excess of its dividend commitment positions it to continue raising the payout even if revenue growth remains measured. The combination of operational discipline and financial strength makes the forward income story here more attractive than the headline yield alone might suggest.

Management Team

Williams-Sonoma’s leadership continues to be one of the most credible management teams in specialty retail. Laura Alber, who has served as President and CEO since 2010, has been with the company since the mid-1990s. Her leadership style is rooted in a deep understanding of the customer and the brand, and her track record includes successfully navigating the company through multiple economic cycles while expanding its digital footprint and direct-to-consumer capabilities. Under her watch, the company has built one of the most impressive margin profiles in retail while continuing to invest in long-term competitive advantages.

Jeff Howie serves as Executive Vice President and CFO, bringing decades of internal experience across multiple Williams-Sonoma brands including Pottery Barn and Pottery Barn Kids. His familiarity with both the financial and operational dimensions of the business gives him a grounded perspective on capital allocation decisions. The CFO role at a company this disciplined about margins and shareholder returns matters enormously, and Howie has demonstrated the right instincts. Together, Alber and Howie represent a leadership pairing with genuine institutional knowledge and alignment around long-term value creation.

Supporting them is a deep bench of merchandising, logistics, and digital leaders who have helped the company build and sustain its multi-brand platform. The consistency of Williams-Sonoma’s financial performance is not accidental — it reflects deliberate decisions made by a team that understands both the brand and the balance sheet.

Valuation and Stock Performance

At $202.43 per share, Williams-Sonoma trades at a trailing P/E of 22.32x against EPS of $9.07. That is a fair-to-full valuation for a specialty retailer, though it is arguably justified by the company’s exceptional return on equity of 56.92%, its consistent free cash flow generation, and its demonstrated ability to grow the dividend meaningfully over time. Price-to-book at 11.79x reflects the asset-light nature of its earnings power rather than a speculative premium — the company earns its returns on a relatively lean asset base.

The 52-week range of $130.07 to $222.00 tells a story of significant volatility. Investors who acted on the dip toward the lower end of that range have been rewarded handsomely. At current levels near $202, the stock has recovered most of its lost ground and sits closer to the upper end of the range. Upside from here is more measured, and the investment case at this price relies more on the quality of the business and the growing income stream than on a deep value argument.

The stock’s beta of 1.64 is a reminder that this is a consumer cyclical name with meaningful sensitivity to broader market moves. In a risk-off environment, WSM can reprice quickly, as last year’s lows demonstrated. For dividend-focused investors with a multi-year horizon, those periods of volatility have historically presented better entry points than today’s price, but they also don’t negate the long-term income and total return case. The company’s pricing discipline, brand strength, and financial consistency remain intact at any point in the cycle.

Risks and Considerations

Despite its strengths, WSM carries a meaningful set of risks that income investors should keep in focus. The company operates in consumer discretionary retail, a space acutely sensitive to shifts in household spending confidence. With a beta of 1.64, the stock amplifies broader market moves, and any deterioration in consumer sentiment tied to employment, interest rates, or broader economic conditions could weigh on both revenue and the stock price.

The housing market connection remains relevant. While Williams-Sonoma doesn’t sell homes, demand for its furniture, kitchenware, and home décor products is closely tied to renovation activity, new household formation, and homeowner confidence. A prolonged cooling in housing could translate into softer demand across its brand portfolio, particularly in higher-ticket categories.

Supply chain and tariff exposure is another consideration. The company sources products globally, and any escalation in trade tensions or input cost inflation could pressure margins, particularly if management chooses to absorb rather than pass through those costs to preserve its premium brand positioning. Short interest of approximately 8.5 million shares reflects that a meaningful number of market participants remain skeptical of the stock at current levels.

Competitive intensity in the home furnishings space has not abated. Online entrants continue to pressure pricing and convenience expectations, while off-price channels offer alternatives to budget-conscious consumers. Williams-Sonoma’s strategy of staying premium and direct-to-consumer has served it well, but maintaining that positioning requires continuous investment and execution. Finally, the pace of digital transformation and evolving sustainability expectations from consumers means the company must keep investing in its customer experience to protect its competitive moat over the long term.

Final Thoughts

Williams-Sonoma offers income investors a package that doesn’t announce itself loudly but holds up well under scrutiny. The yield of 1.18% is modest, but behind it sits a company with a 28% payout ratio, free cash flow nearly four times the annual dividend commitment, and a track record of raising its payment by nearly 47% over the past three years. That is the profile of a dividend that is not only safe but likely to keep growing.

The business itself is firing well. A 14.3% profit margin, 56.92% return on equity, and $1.35 billion in operating cash flow are not metrics that suggest a company struggling to find its footing. Laura Alber and her team have built something durable — a multi-brand platform with real pricing power and a direct-to-consumer model that gives them both margin control and customer data advantages. At $202.43, the stock is not cheap by traditional retail standards, but the premium reflects genuine quality. For patient investors building income over time, Williams-Sonoma remains a name worth owning.