Updated April 2025

WEC Energy Group is one of those names that quietly delivers year after year, making it a favorite among income-focused investors. Headquartered in Milwaukee, this utility giant serves millions of customers across the Midwest through its collection of subsidiaries like We Energies and Peoples Gas.

It’s the kind of business that doesn’t need flashy headlines to get noticed by dividend investors. WEC is built around the simple, reliable business of keeping the lights on and the heat flowing. And for shareholders, that translates into consistent cash flow and a rock-solid dividend that’s grown steadily over time.

Recent Events

In the past year, WEC Energy has made a solid move, with shares climbing more than 34%. That’s a notable run for a utility, especially when compared to the broader market’s more modest gains. For investors who value consistency and income over speculation, that’s exactly the kind of quiet strength you like to see.

Much of this performance has been backed by strong fundamentals. The company recently posted a 107% increase in quarterly earnings year over year. That kind of jump isn’t common in the utility world, and it shows WEC’s ability to control costs and boost margins even in a tough environment.

With interest rates remaining high, many investors are rotating back into sectors that offer dependable income. Utilities like WEC, which offer steady dividends and operate in highly regulated environments, have started to catch more attention. Its earnings growth, reasonable valuation, and stable financials all make it a compelling play for those looking to park their capital in a safe, income-generating spot.

Key Dividend Metrics 💸

📈 Forward Yield: 3.28%

💵 Annual Dividend: $3.57 per share

📊 Payout Ratio: 69.15%

📆 Dividend Growth Streak: 20+ years

⏱ Dividend Date: March 1, 2025

❌ Ex-Dividend Date: February 14, 2025

📉 5-Year Average Yield: 3.15%

🧱 Debt/Equity: 159.11%

🔍 Beta (5Y Monthly): 0.43

Dividend Overview

For income investors, WEC Energy checks a lot of the right boxes. The stock currently yields 3.28%, which is slightly above its five-year average. That suggests you’re getting a decent return on your investment without having to overpay for the shares.

The annual payout of $3.57 per share is well covered by earnings, with a payout ratio just shy of 70%. That’s right in the wheelhouse for a utility—high enough to deliver real income, but still responsible enough to maintain flexibility. This isn’t a company stretching itself thin to please shareholders. It’s running a stable, sustainable playbook.

WEC has a long track record of paying out dividends consistently, and the March 1 payment is just the latest in a string that goes back decades. Investors can rely on that cash hitting their accounts on schedule—something that’s become increasingly valuable in today’s unpredictable markets.

There’s also no need to worry about this being a recent pivot to please Wall Street. WEC’s dividend culture is deeply embedded in how the business operates. That kind of stability is tough to fake.

Dividend Growth and Safety

What really sets WEC apart is its dividend growth. While it’s easy to find stocks that pay a high yield, it’s harder to find those that consistently raise their dividends year after year. WEC has done just that, with its most recent increase coming in at 6.3%. That continues a more than two-decade streak of annual hikes.

For investors thinking long-term, that steady growth adds up. Even modest increases, when compounded over years, can make a big difference in total returns—especially when reinvested.

From a safety perspective, WEC is in solid shape. The company does carry a fairly large debt load—over $20 billion—with a debt-to-equity ratio above 159%. But for a utility, that’s not unusual. These businesses are capital intensive, and they rely on consistent revenue from regulated operations to service that debt.

WEC’s financials reflect that strength. It generated over $3.2 billion in operating cash flow last year, which provides a solid base to support its dividend. Levered free cash flow did come in negative at around -$579 million, which likely reflects investments in infrastructure and long-term projects. It’s worth watching, but not yet a red flag given the company’s track record.

The company also carries a low beta of just 0.43. That means the stock tends to move much less than the overall market—a trait income investors often appreciate, especially when volatility picks up.

Return on equity sits at 12.25%, and return on assets is 2.85%. For a utility, those are respectable numbers that show management is making efficient use of capital while maintaining the reliability shareholders count on.

And then there’s the shareholder base—over 83% of shares are held by institutions. That kind of backing usually means large investors see long-term value in the company’s consistent dividend performance.

All told, WEC Energy offers a balanced mix of yield, stability, and growth that fits neatly into a dividend-focused portfolio. Whether you’re retired and living off the income or reinvesting for the future, this is a company that continues to do the simple things well—generate cash, pay dividends, and repeat.

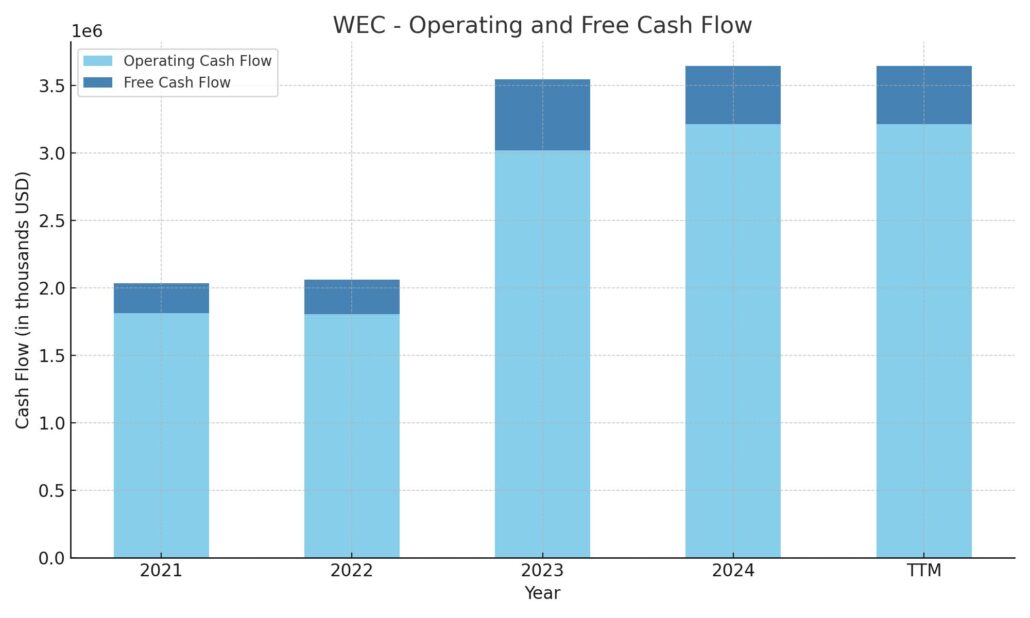

Cash Flow Statement

WEC Energy Group’s cash flow over the trailing 12 months reflects the stable nature of its utility operations, with operating cash flow coming in at $3.21 billion. That’s a modest increase over the previous year and a meaningful improvement from 2021 and 2022 levels, which hovered just above $2 billion. This steady rise shows the company’s core operations are healthy and generating reliable cash even in a capital-heavy environment. However, the capital expenditure remains significant, at $2.78 billion for the period, as the company continues investing in infrastructure and system upgrades.

Investing cash flow remains deep in negative territory at -$3.8 billion, driven largely by those ongoing capital projects. Financing activities contributed a net inflow of $467.7 million, as WEC leaned into the bond market, issuing over $4.4 billion in new debt while repaying $2.14 billion. The result is a modest $430.7 million in free cash flow—positive, but down from the prior year. While the ending cash position fell to just $42.2 million, WEC’s consistent cash generation suggests this isn’t concerning. The firm continues to prioritize long-term infrastructure development while maintaining the ability to fund its dividend from internal cash flows.

Analyst Ratings

📈 WEC Energy Group has recently seen some movement in analyst sentiment. Wells Fargo raised its price target from $112 to $115 while keeping an “overweight” rating in place. That kind of upgrade usually reflects confidence in stable earnings and a well-managed balance sheet. Analysts there seem to see room for more upside, driven by the company’s predictable cash flow and steady dividend growth.

🔄 Over at Barclays, the stock got a modest lift in sentiment as well. They bumped their rating from “underweight” to “equal weight” and lifted their price target from $89 to $93. While not a glowing endorsement, it’s a noticeable shift that likely reflects stronger-than-expected earnings and better positioning in the current interest rate environment.

🟢 KeyCorp echoed a similar tone, tweaking its price target upward from $108 to $109 while reiterating an “overweight” rating. That suggests they still see solid fundamentals supporting WEC’s long-term outlook.

📊 Bank of America also adjusted its stance, moving WEC from “underperform” to “neutral” with a revised price target of $98, up from $90. It’s a meaningful shift that hints at improved expectations around free cash flow and rate-based earnings growth.

💬 BMO Capital Markets moved their target slightly higher as well, from $95 to $100, keeping a “market perform” rating. That signals they expect WEC to perform roughly in line with the broader sector.

🧭 The current consensus price target sits at $101.88. That reflects a relatively balanced view from the analyst community, with the stock currently trading slightly above that average, suggesting some see it near fair value for now.

Earning Report Summary

Strong Year-End Numbers

WEC Energy Group closed out 2024 on a high note. Full-year net income came in at $1.5 billion, translating to $4.83 per share. That’s a solid step up from the $4.22 per share they posted the year before. When you strip out a few one-time items, adjusted earnings hit $4.88 per share, showing a healthy 5.4% year-over-year gain. It’s the kind of consistent progress investors like to see—steady, dependable, and without unnecessary drama.

The fourth quarter was particularly strong. Net income surged to $453.5 million, or $1.43 per share, compared to just $218.5 million and $0.69 per share in the same quarter the previous year. That’s a significant jump, driven by better operational performance across their utility businesses. While revenue for the quarter landed at $2.28 billion—just a hair below what analysts were hoping for—the overall earnings strength helped more than make up for it.

Dividend Boost and Future Plans

One of the standout announcements was a bump in the dividend. WEC raised its quarterly payout by 6.9% to $0.8925 per share. That marks the 22nd consecutive year of dividend increases, which is no small feat. For income investors, that kind of track record builds real confidence.

The company also laid out a bold $28 billion capital plan stretching over the next five years. It’s the biggest investment program in WEC’s history, aimed at upgrading infrastructure and adding more renewable energy projects to its portfolio. It shows the company is thinking long term while staying committed to sustainability and growth.

Looking Ahead

As for the road ahead, WEC expects earnings in 2025 to land somewhere between $5.17 and $5.27 per share. It’s a forecast that signals stability, especially considering how much capital they’re planning to deploy. The company seems confident in its direction, balancing investment in future capacity while still returning value to shareholders.

All in all, WEC’s latest results paint a picture of a company that’s doing exactly what it set out to do—deliver reliable service, reward its shareholders, and make smart investments for the future.

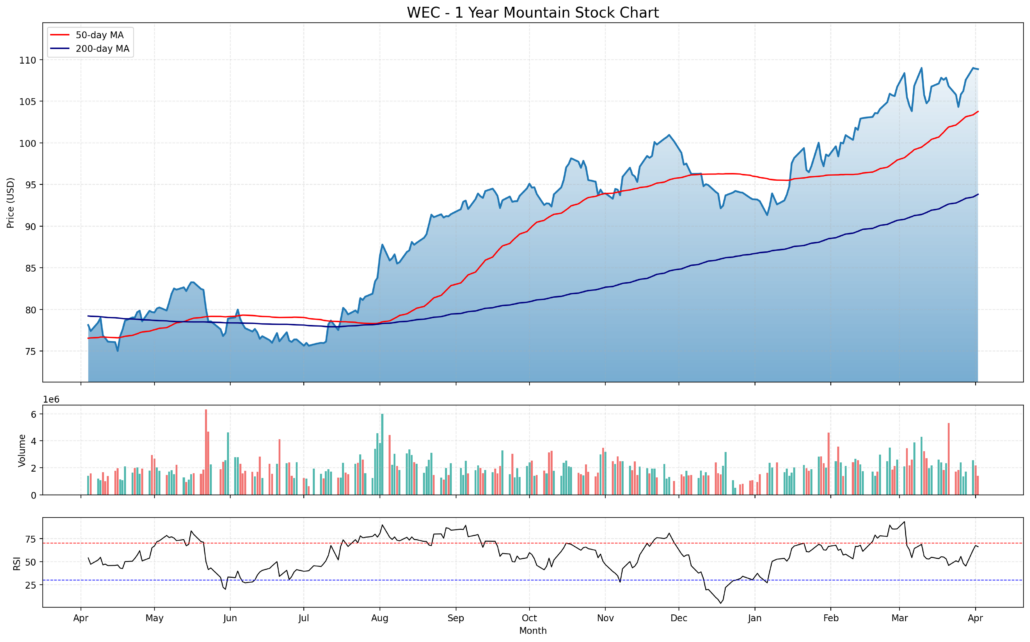

Chart Analysis

Price Trend and Moving Averages

WEC has been in a strong, sustained uptrend over the past year, climbing steadily from around $76 in early April to just shy of $110 as of the most recent data point. The 50-day moving average (in red) has been well above the 200-day moving average (in blue) for several months now, a sign of healthy momentum and a classic marker of a strong trend. The 200-day moving average is sloping upward, which reinforces the broader direction of travel. Price action has consistently respected this structure, with pullbacks finding support and eventually giving way to new highs.

In the last few months, the stock has broken through previous resistance levels with increasing conviction. It has stayed well above the longer-term moving average, which shows that this isn’t just a short-term rally—it’s been building over time.

Volume Behavior

Volume has shown a few notable spikes, particularly during periods of price acceleration in the summer and again in March. These surges were accompanied by sharp upward price moves, pointing to strong buying interest. In contrast, volume during the mild pullbacks has been subdued, suggesting that selling pressure hasn’t been significant enough to reverse the trend.

Relative Strength Index (RSI)

The RSI has mostly hovered between the 50 and 70 range, occasionally pushing above 70 but never for extended periods. That’s generally a sign of controlled strength—buyers are in charge, but the stock hasn’t entered a dangerous overbought zone for too long. In recent weeks, RSI has nudged close to overbought levels again, signaling strong underlying momentum without flashing a major red flag.

General Outlook

WEC has demonstrated a steady, upward trajectory with supportive technicals and rising volume on rallies. The stock has stayed technically sound through various market conditions over the last year, with clear institutional interest reflected in both price and volume behavior. The RSI confirms persistent strength without suggesting major overheating. This kind of pattern reflects confidence in the underlying business and signals a clear preference by market participants to stay long.

Management Team

At the helm of WEC Energy Group is Scott J. Lauber, who took over as President and Chief Executive Officer in early 2022. His long-standing history with the company spans a range of leadership roles, which gives him a deep understanding of both the operational and strategic sides of the business. Lauber has helped guide WEC through a critical phase of transformation as it invests heavily in renewable energy and infrastructure upgrades.

Supporting him is Xia Liu, the Executive Vice President and Chief Financial Officer. Liu brings years of financial leadership experience within the energy space and plays a key role in managing capital allocation, funding major initiatives, and ensuring that the company maintains financial strength even as it expands. The broader leadership team includes experienced professionals overseeing regulatory, legal, and operational functions—each playing a role in keeping the company aligned with long-term goals.

Valuation and Stock Performance

WEC Energy Group shares have shown quiet strength over the past year. As of early April 2025, the stock trades around $108.84, near the top end of its 52-week range. The share price has steadily climbed over the last twelve months, reflecting investor confidence in the company’s financial consistency and forward-looking capital plan.

With a market cap of around $34.4 billion and a price-to-earnings ratio of 22.6, the stock sits in line with other regulated utilities. It’s not a bargain-bin valuation, but that’s expected for a company with strong fundamentals and predictable cash flows. The P/E is supported by rising earnings, and the forward guidance for 2025 shows continued momentum.

The stock has stayed in a range between $77.47 and $110.19 over the past year, trending steadily upward. A beta of 0.44 suggests that WEC tends to be less volatile than the broader market, which is typically what you’d want in a utility stock focused on reliability and income. Current analyst sentiment leans neutral, with a consensus price target of $100.25. That implies a slight downside from current levels but also reflects the market’s recognition of WEC’s premium stability.

Risks and Considerations

There are always trade-offs with a company like WEC. One of the main risks is regulatory. Utilities operate under strict oversight, and any changes in rate policy, environmental rules, or energy mandates could impact profitability. The company’s ability to recover costs and earn a fair return on investment depends heavily on state and federal regulatory bodies.

The capital-intensive nature of the business is another factor to weigh. WEC is in the middle of a major infrastructure investment cycle, committing roughly $28 billion over five years. That’s a big number, and while it’s designed to modernize the grid and grow renewables, it also places pressure on the balance sheet. Debt levels are already elevated, and free cash flow is being closely monitored to ensure the dividend remains sustainable.

Environmental transitions pose both opportunity and risk. WEC is actively investing in decarbonization efforts, but any delays, cost overruns, or shifts in government policy could introduce new headwinds. At the same time, the pace of technological change in energy storage and transmission could require even more investment than currently planned.

There’s also the broader economic backdrop. While utility demand is typically stable, rising interest rates or inflationary pressures on materials and labor could squeeze margins. Market downturns may not hit WEC’s earnings directly, but they could impact investor sentiment and valuations.

Final Thoughts

WEC Energy Group continues to demonstrate why it’s considered one of the more reliable names in the utility space. The leadership team is experienced, the business model is anchored in stability, and the company is adapting to the energy transition with purpose and discipline.

The stock may not have explosive upside, but it offers the kind of dependable performance that fits well in portfolios focused on long-term results. WEC isn’t standing still—it’s reinvesting in its network, expanding its clean energy footprint, and maintaining a multi-decade track record of paying and growing dividends.

As with any investment, there are risks, particularly around regulation and capital demands. But WEC’s steady execution and focus on long-term planning suggest it’s navigating those risks with care. The combination of operational strength, a shareholder-friendly approach, and a forward-looking strategy makes it a company that continues to deliver in its lane.