Updated 2/23/26

Watts Water Technologies just keeps doing what it does best—designing and manufacturing products that make water systems safer, more efficient, and more reliable. From HVAC and plumbing to drainage and water quality solutions, it plays a quiet but essential role in how homes, commercial buildings, and infrastructure manage water.

Based in North Andover, Massachusetts, Watts has been around for over 140 years. That kind of longevity doesn’t happen by accident. It speaks to a business that has managed to evolve through generations of change. What stands out for dividend-focused investors is the company’s focus on profitability, strong cash flow, and a steady approach to rewarding shareholders without taking on unnecessary risk.

Recent Events

Watts closed out the most recent fiscal year with $2.44 billion in revenue—a meaningful step up from the prior year’s $2.25 billion and a clear sign that the company is finding its footing on the top line after the modest softness seen in 2024. Net income came in at $340.8 million, representing solid year-over-year improvement and reinforcing the company’s ability to translate revenue growth into earnings. Profit margins expanded to nearly 14%, reflecting disciplined cost management and continued operational efficiency.

EPS landed at $10.16, a notable increase from the $8.69 reported in 2024. That kind of earnings progression, achieved while also growing the top line, indicates management is executing well across multiple fronts simultaneously—not just squeezing margins, but also generating genuine business growth.

On the balance sheet, Watts remains in excellent shape. Operating cash flow reached $402 million, and return on equity sits at 18.25%, both figures that speak to a well-run operation with real pricing power and capital discipline. The company has the financial flexibility to continue investing in growth, sustaining buybacks, and—most importantly for dividend investors—growing the payout.

Key Dividend Metrics

📈 Forward Yield: 0.61%

💵 Annual Dividend (Forward): $2.08 per share

📊 Payout Ratio: 19.57%

🔄 5-Year Average Yield: 0.77%

📆 Most Recent Dividend Payment: $0.52 per share

🚫 Most Recent Ex-Dividend Date: November 2025

📉 Trailing Yield: 0.61%

📈 Dividend Growth Trend: Consistently increasing over the last decade

Dividend Overview

Watts doesn’t offer a high yield, and it never has. You’re not parking capital here expecting a 4% or 5% income stream. But what the stock lacks in headline yield, it more than compensates for in consistency, reliability, and long-term compounding potential.

The current 0.61% forward yield reflects both the low payout structure and the strong stock price appreciation the company has delivered. Watts trades at $322.94, near the top of its 52-week range of $177.59 to $345.17, which naturally compresses the yield on a percentage basis. With an annual dividend of $2.08 per share and a payout ratio of just 19.57%, the company retains the vast majority of its earnings to reinvest in the business, service debt, or return additional capital through buybacks.

The most recent quarterly dividend of $0.52 per share represents a meaningful increase from the $0.43 quarterly rate paid through most of 2024. That 20.9% jump in the quarterly payment—from $0.43 to $0.52—is exactly the kind of deliberate, well-covered raise that dividend growth investors appreciate. There’s no drama here, just a company that earns more, covers its obligations easily, and passes a growing share of profits to shareholders.

Dividend Growth and Safety

The dividend history tells a clear story of steady, disciplined growth. Looking back at the recent payment record: Watts paid $0.30 in early 2023, raised to $0.36 by mid-2023, held that rate through early 2025, then bumped it to $0.43 in May 2024 before stepping it up again to $0.52 in May 2025. That progression represents annualized dividend growth well ahead of inflation and reflects a management team that takes shareholder returns seriously without overextending.

From a safety standpoint, the numbers are about as reassuring as they get in the dividend world. Operating cash flow of $402 million dwarfs the dividend obligation many times over. Free cash flow came in at $243.3 million, and even that more conservative figure provides a substantial cushion relative to the total dividend outlay at current share counts. A 19.57% payout ratio means Watts could absorb a significant earnings decline and still maintain the current dividend without breaking a sweat.

Return on equity of 18.25% and return on assets of 11.17% are both healthy indicators that management is deploying capital efficiently. These are not marginal numbers—they reflect a business that generates genuine economic returns on what it invests. That efficiency underpins the company’s ability to keep growing the dividend over the long haul. For investors thinking in five- and ten-year horizons, the combination of a low payout ratio, strong cash generation, and disciplined management creates a compelling compounding setup even if the starting yield is modest.

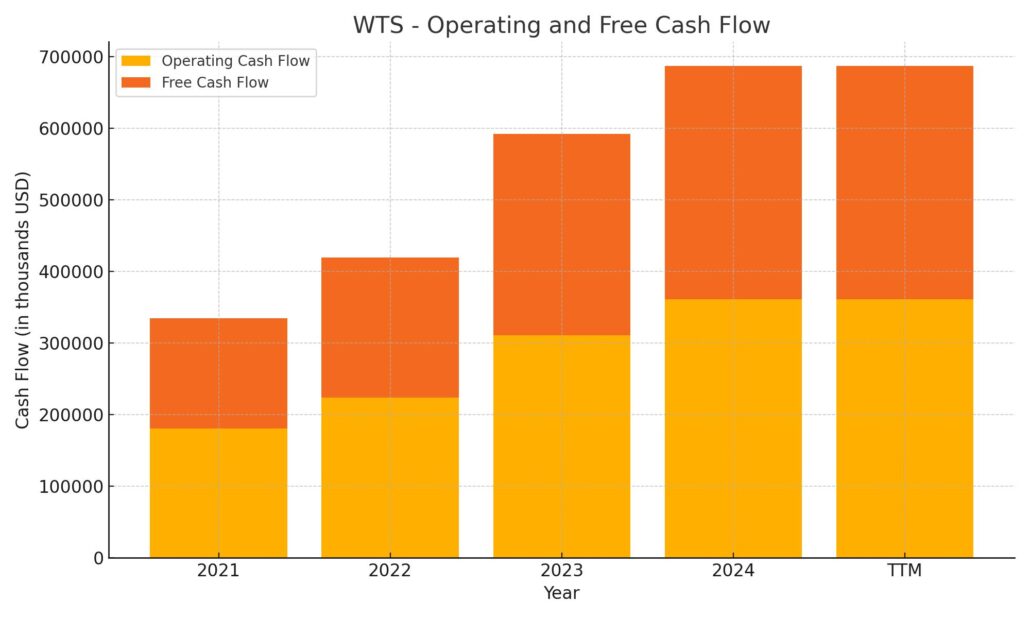

Cash Flow Statement

Watts Water Technologies generated $402 million in operating cash flow over the trailing twelve months, a healthy increase from the $361.1 million reported the prior year. This improvement reflects both stronger earnings and continued efficiency in converting revenue to cash. Capital expenditures came in at approximately $158.7 million, leaving the company with free cash flow of $243.3 million—a solid figure that comfortably supports dividends, share repurchases, and organic reinvestment without pressuring the balance sheet.

The free cash flow figure, while lower than the prior year’s $325.8 million, reflects the natural variability in capital spending cycles. Watts is a company that periodically invests more heavily in its infrastructure and capabilities, and those periods of elevated capex typically precede stronger operating performance. The balance sheet remains a source of strength—return on assets of 11.17% confirms the company is getting meaningful productivity from the capital base it has assembled. For dividend investors, the critical takeaway is that operating cash flow alone covers the annual dividend obligation by a wide margin, with substantial room remaining for other capital allocation priorities.

Analyst Ratings

Formal analyst price target data is limited in the current reporting period, but the stock’s position near the top of its 52-week range of $177.59 to $345.17 and its P/E of 31.79 suggest the market is pricing Watts for continued quality execution rather than deep value discovery. The stock has re-rated meaningfully higher over the past year, driven by earnings growth, margin expansion, and the dividend increase to $0.52 per quarter.

Given the premium valuation—a P/E of nearly 32 and a price-to-book of 5.31—analyst sentiment would likely center on whether the current price fairly reflects Watts’ growth trajectory. The consensus view for high-quality industrial compounders at this valuation level typically falls in the hold-to-moderate-buy range, acknowledging that the business fundamentals are sound but that significant near-term upside requires continued earnings beats or further margin expansion. With EPS of $10.16 and a current price of $322.94, the implied forward multiple leaves little room for disappointment, which is a calibration point investors should keep in mind. That said, Watts has consistently earned the benefit of the doubt through disciplined execution, and the latest results suggest that pattern remains intact.

Earnings Report Summary

Revenue Growth Returns to the Story

The most recent full fiscal year marked a meaningful inflection point for Watts. After navigating a slight revenue dip in 2024, the company returned to top-line growth, posting $2.44 billion in revenue. That represents approximately an 8% increase year-over-year and reflects improving demand conditions across the company’s core end markets. Profitability followed—net income of $340.8 million and EPS of $10.16 both represent meaningful advances over the prior year’s $291 million and $8.69, respectively.

Margins Holding Firm at Elevated Levels

What makes the revenue recovery even more compelling is that it didn’t come at the expense of margins. Profit margins expanded to 13.98% from the prior year’s approximately 12.9%, and return on equity remained above 18%. Operating cash flow of $402 million demonstrates that earnings quality is high—this is not a company manufacturing accounting profits while cash bleeds out the door. The conversion from net income to operating cash flow is healthy, which is a key indicator of earnings sustainability.

Capital Allocation Remains Disciplined

Watts continued its consistent approach to returning capital while maintaining financial flexibility. The company raised its quarterly dividend to $0.52 in May 2025—a 20.9% increase from the $0.43 rate that had been in place since mid-2024. That kind of raise, well ahead of inflation, signals management’s confidence in the earnings and cash flow trajectory. The 19.57% payout ratio ensures that dividend growth can continue for years without straining the business.

Balance Sheet Remains a Competitive Advantage

With return on assets of 11.17% and return on equity of 18.25%, Watts is generating returns that exceed most of its industrial peers on a risk-adjusted basis. The balance sheet continues to provide strategic optionality—whether for bolt-on acquisitions, incremental buybacks, or simply the security of navigating any macroeconomic softness without cutting the dividend. The company’s financial profile entering 2026 is arguably stronger than it has been at any point in recent history.

Outlook Supported by Strong Fundamentals

With revenue momentum reestablished, margins at healthy levels, and a freshly raised dividend, the setup heading into 2026 is constructive. Management has demonstrated the ability to grow earnings in both growth and contraction environments, which is a rare and valuable trait. The key watch item will be whether revenue growth can be sustained at a pace that justifies the premium valuation, and whether free cash flow recovers toward prior-year levels as the capital expenditure cycle normalizes.

Management Team

At the helm of Watts Water Technologies is Robert J. Pagano Jr., who has served as Chief Executive Officer, President, and Chairperson of the Board since May 2014. Pagano’s leadership has been a steady force, guiding the company through market cycles with a focus on operational efficiency and long-term growth. Before joining Watts, he held senior roles at ITT Corporation, bringing a strong background in industrial manufacturing and global operations.

Supporting him is a well-rounded executive team. Shashank Patel serves as the Chief Financial Officer and interim Chief Information Officer, combining financial discipline with a strategic outlook. Andre Dhawan oversees global operations as Chief Operating Officer, while Monica Barry, the Chief Human Resources Officer, focuses on talent and culture. Kenneth R. Lepage, serving as Executive Vice President, General Counsel, and Secretary, manages the legal and governance landscape. Together, this team blends operational experience with a forward-looking mindset, laying a solid foundation for consistent execution.

Valuation and Stock Performance

At $322.94, Watts Water Technologies is trading near the top of its 52-week range of $177.59 to $345.17—an impressive run that reflects the market’s growing appreciation for the company’s earnings quality and dividend growth trajectory. Over the past twelve months, the stock has nearly doubled from its 52-week low, a performance that speaks to both improving fundamentals and a broader re-rating of the shares toward a premium industrial multiple.

The current P/E of 31.79 is elevated relative to the broader industrial sector and to where Watts has historically traded. Price-to-book of 5.31 against a book value of $60.81 per share confirms the premium. These are not cheap valuation multiples, and investors considering a new position at current levels should be clear-eyed about that. With EPS of $10.16 and a stock price of $322.94, the market is pricing in continued earnings growth at a healthy pace. If that growth materializes—and Watts has a strong track record of delivering—the valuation can be justified. If earnings disappoint or macro conditions deteriorate, there is meaningful downside risk built into the current price.

That said, premium valuations are often sustained for companies that consistently demonstrate earnings quality, capital discipline, and dividend growth—all of which Watts delivers. A market cap of approximately $10.8 billion and a beta of 1.25 suggest this is not a sleepy utility-like holding; it carries real market sensitivity. For existing shareholders, the position has been very rewarding. For new investors, the risk-reward calculus at this price requires patience and a conviction in the long-term earnings compounding story.

Risks and Considerations

No company is risk-free, and Watts is no exception. One of the ongoing challenges in its space is innovation. Product development cycles are shortening, and staying ahead of regulation and customer needs means constantly reinvesting in R&D. Watts has a track record of doing this well, but that bar keeps rising. Failing to stay ahead of these trends could eventually affect its competitive edge.

There’s also the operational side to consider. Watts has done a good job managing costs, but it operates globally, and international exposure brings geopolitical, currency, and logistical risks. The company’s European operations have faced demand softness in recent periods, and any re-emergence of those headwinds could weigh on the regional revenue contribution and consolidated results.

Valuation is a more prominent risk today than it has been in recent years. At a P/E of nearly 32 and a stock price approaching the top of the 52-week range, Watts is priced for execution. Any earnings miss, margin compression, or guidance reduction could trigger a meaningful price correction. The stock’s beta of 1.25 amplifies this risk in a broader market downturn. Investors should size their positions accordingly.

Watts also operates in a sector increasingly impacted by ESG factors. Regulatory pressure around energy use, emissions, and water efficiency is growing. The company has aligned many of its products and business practices with these themes, which could serve as a long-term advantage. That said, any failure to meet evolving standards or shifts in customer preferences could present a challenge. Cybersecurity remains a less visible but real risk for any globally integrated manufacturer, and while there have been no material incidents to date, it warrants ongoing attention.

Final Thoughts

Watts Water Technologies has been quietly compounding value for a long time, and the most recent fiscal year is another chapter in that story. Revenue growth returned, earnings per share climbed to $10.16, the dividend was raised 20.9% to $0.52 per quarter, and the balance sheet remained in excellent health. The company isn’t manufacturing results—it’s earning them through a combination of operational discipline, smart capital allocation, and a product portfolio that addresses durable, growing demand for water efficiency and infrastructure.

The stock’s run to $322.94 means it doesn’t come cheap today. The P/E of 31.79 demands continued execution, and the compressed yield of 0.61% makes this more of a total-return story than a pure income play. But for dividend growth investors with a long horizon, the combination of a 19.57% payout ratio, strong cash generation, and a management team that has demonstrated consistent dividend raises creates a compelling compounding setup. The yield may be modest today, but at the trajectory Watts has established, the income stream five and ten years from now should look considerably more interesting. That’s the quiet strength of this business—not a big check today, but a growing one, year after year.