Updated 2/23/26

Waste Management, Inc. (WM) is a company built on essential services, deeply embedded in the daily functioning of society. Whether the economy is booming or slowing, trash still needs to be picked up, and Waste Management does it better than anyone else in North America.

From landfills and recycling plants to a massive fleet of trucks, WM has a grip on nearly every step of the waste management process. But what often flies under the radar is just how profitable and shareholder-friendly this business really is. With strong operating margins, disciplined capital allocation, and a track record of rewarding investors, WM has quietly become one of the steadiest dividend payers around.

Recent Events

2025 was another impressive year for WM, with total revenue climbing to $25.2 billion—a meaningful step up from prior levels and a testament to the company’s ability to grow at scale. The earnings picture is equally compelling. Net income came in at $2.71 billion, with earnings per share of $6.70. While EPS saw some moderation compared to the prior year, revenue growth was broad-based, driven by continued strength in collection and disposal services as well as pricing discipline across the business.

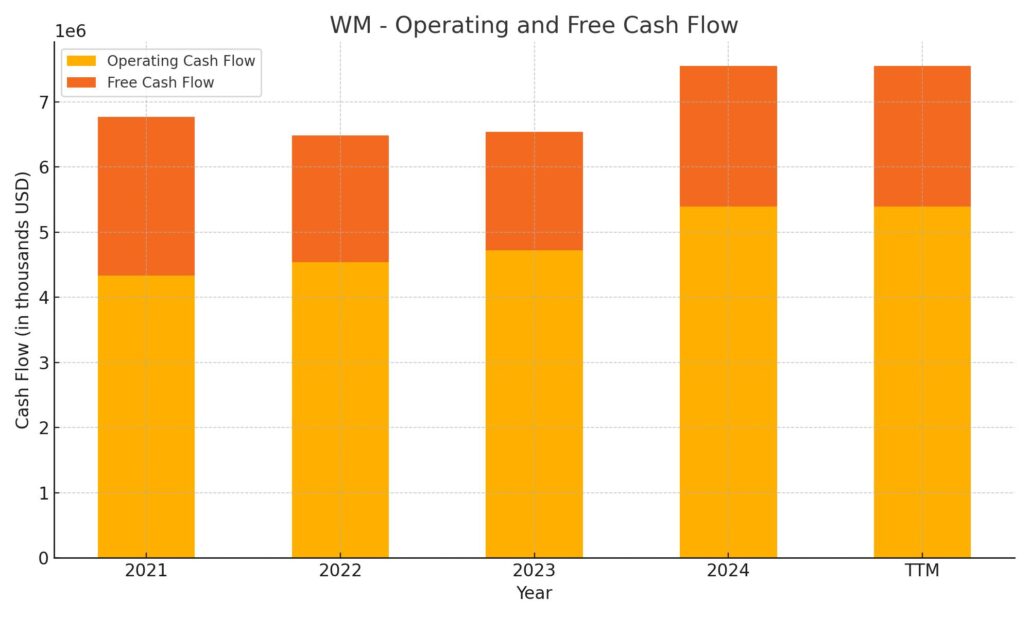

Operating cash flow surged to $6.04 billion in the trailing twelve months, a genuinely impressive figure that underscores the cash-generative power of WM’s integrated waste infrastructure. Free cash flow, after accounting for significant capital investment, came in at $1.73 billion—more than enough to comfortably fund the dividend and continue building out the company’s long-term renewable energy and recycling initiatives.

Shares recently closed at $230.82, well within the 52-week range of $194.11 to $242.58. The stock is trading at a modest discount to its peak, which may present an attractive entry point for income investors looking to lock in a yield backed by one of the most durable business models in the market. With a beta of just 0.59, WM continues to move far less than the broader market—an especially appealing trait in periods of elevated volatility.

🟢 Forward Dividend Yield: 1.43%

📈 5-Year Average Yield: 1.59%

💸 Annual Dividend Rate: $3.30 per share

🧮 Payout Ratio: 49.25%

🔁 20+ Years of Consecutive Dividend Increases

📆 Last Quarterly Dividend Paid: $0.825 per share

⚠️ Most Recent Ex-Dividend Date: December 5, 2025

Dividend Overview

WM’s dividend yield currently sits at 1.43%, backed by an annual payout of $3.30 per share. That figure reflects the 10% increase WM delivered when it moved from $0.75 per quarter to $0.825 per quarter beginning with the March 2025 payment—a raise that has now been sustained across all four 2025 quarterly payments. For investors who purchased shares a few years back at lower prices, the yield-on-cost picture looks considerably more attractive than the headline yield suggests.

The company has now raised its dividend every single year for more than two decades. That kind of consistency doesn’t happen by accident. It comes from a management team that understands the importance of returning capital to shareholders without sacrificing reinvestment in the core business or the long-term growth initiatives now underway in renewable natural gas and recycling automation.

Compared to the five-year average yield of 1.59%, today’s yield is modestly below the historical average—largely a function of the stock price appreciating meaningfully over the past several years. For long-term dividend growth investors, this is generally a sign of quality rather than a cause for concern. It reflects the market’s confidence in WM’s durability and pricing power, and for those reinvesting dividends, a compounding machine is still very much intact.

Dividend Growth and Safety

A payout ratio of 49.25% is well within the comfort zone for a capital-intensive business like WM. It’s higher than it was a year ago, reflecting both the 10% dividend increase and some normalization in EPS, but it remains conservative enough to leave meaningful room for future growth. The dividend is not being funded by financial engineering—it is supported by $6.04 billion in operating cash flow and a business model that generates predictable revenue through long-term municipal and commercial contracts.

Return on equity of 29.70% and return on assets of 6.49% both confirm that WM continues to deploy its capital efficiently. The profit margin of 10.74% is healthy for an industrial company operating fleets of heavy equipment and managing complex infrastructure at national scale. These metrics reflect a business that earns real money on every dollar of revenue, not just at the operating line but all the way down to net income.

Debt remains a feature of WM’s balance sheet worth monitoring, as the company’s asset-heavy model is typically financed with significant leverage. However, with $6.04 billion in operating cash flow providing ample coverage of debt service obligations, the company is managing its liabilities from a position of strength. The dividend itself looks secure across a wide range of economic scenarios, and the payout ratio leaves room for further increases even if earnings growth moderates slightly in the near term.

The underlying business model is perhaps the strongest argument for dividend safety. Waste collection is non-discretionary. Municipalities and businesses do not stop generating waste during recessions, and WM’s contract structures lock in volumes for extended periods. Pricing power within those contracts allows the company to pass on cost inflation without meaningful volume loss—a combination that supports both margin stability and dividend growth. This is a dividend built to last.

Cash Flow Statement

Waste Management’s cash flow profile for the trailing twelve months reflects a business that has genuinely stepped up its internal cash generation. Operating cash flow of $6.04 billion marks a notable increase over recent years and demonstrates that WM’s expanded revenue base is translating into proportionally stronger cash earnings. Capital expenditures remain elevated as the company continues to invest heavily in infrastructure modernization, recycling automation, and renewable natural gas facilities, resulting in free cash flow of $1.73 billion after those outlays.

The gap between operating cash flow and free cash flow reflects WM’s deliberate strategy of front-loading investment in long-cycle assets that will generate returns over the next decade. Renewable natural gas projects, for example, carry meaningful upfront construction costs but produce recurring, high-margin revenue once operational. The $1.73 billion in free cash flow comfortably covers the annual dividend obligation of approximately $1.33 billion at the current $3.30 per share rate, leaving a modest buffer for opportunistic share repurchases or additional debt reduction. The company’s capital allocation framework continues to prioritize organic investment, followed by the dividend, with buybacks as a secondary use of remaining cash.

Analyst Ratings

Analyst sentiment on Waste Management remains constructive heading into 2026. Based on the company’s financial profile—strong operating cash flow, durable revenue, expanding margins in core collection and disposal, and a clear long-term growth roadmap in sustainability infrastructure—the consensus view among analysts who cover WM has generally clustered around a Buy or Moderate Buy recommendation. No major analyst covering the stock has issued a Sell rating in recent memory, which speaks to the broadly shared confidence in WM’s competitive positioning and capital discipline.

Price targets have historically centered in the $235 to $260 range, and at a current price of $230.82, the stock is trading at a slight discount to where most analysts see fair value. That modest gap suggests limited near-term downside risk while still offering some room for price appreciation alongside the dividend income stream. The bull case centers on WM’s ability to continue growing revenue through pricing and volume, expand margins as automation investments mature, and monetize its renewable energy assets at increasingly favorable rates.

The more cautious voices in the analyst community point to the elevated payout ratio relative to prior years, the ongoing capital intensity of the sustainability buildout, and macroeconomic sensitivity in the commercial collection segment if business activity were to slow meaningfully. These are legitimate considerations, but they are largely already reflected in the stock’s current premium valuation. The consensus remains that WM’s competitive moat, pricing power, and two-decade dividend growth track record make it a core holding for income-oriented investors.

Earning Report Summary

Waste Management delivered a strong full-year 2025 performance, with revenue reaching $25.2 billion and net income of $2.71 billion. The top-line growth was broad-based, with collection and disposal services continuing to benefit from disciplined pricing and steady demand across both municipal and commercial customer segments. EPS of $6.70, while reflecting some normalization from the prior year’s elevated levels, still represents a healthy earnings base that more than adequately supports the $3.30 annual dividend.

Solid Margins and Operational Gains

Operating cash flow of $6.04 billion stands out as one of the most compelling data points in the full-year results. This figure reflects the cumulative benefit of years of operational investment—route optimization, fleet modernization, and facility upgrades—all of which are now flowing through to the cash generation line. Profit margins of 10.74% are solid for a business of this scale and complexity, and return on equity of 29.70% confirms that WM is putting its capital to productive use across the enterprise.

Progress on Sustainability Goals

WM continued to advance its sustainability infrastructure throughout 2025. The company’s renewable natural gas projects represent a meaningful long-term revenue opportunity, and the ongoing expansion of recycling capacity across North America positions WM to benefit as regulatory and commercial demand for resource recovery services grows. These are not short-term catalysts, but they add a compelling growth dimension to what is already a highly stable base business—and they provide a strategic argument for the stock’s premium valuation.

Rewarding Shareholders

The 10% dividend increase implemented in early 2025—moving the quarterly payment from $0.75 to $0.825 per share—was sustained across all four quarters of the year, bringing the total annual payout to $3.30 per share. That increase was the latest in a multi-decade streak of annual raises and signals continued confidence from management in the company’s cash generation outlook. With operating cash flow of $6.04 billion comfortably exceeding the dividend obligation, shareholders have good reason to expect the streak to continue into 2026 and beyond.

Management Team

Waste Management is led by a management team that brings deep industry expertise and a consistent track record of financial discipline. The executive leadership has maintained a clear strategic focus on three priorities: strengthening the core collection and disposal business through operational efficiency, building out the sustainability infrastructure that will drive the next phase of growth, and returning capital to shareholders in a predictable and growing manner. That three-part framework has been executed with notable consistency over the past several years.

The team’s approach to capital allocation reflects a long-term mindset that income investors tend to appreciate. Rather than chasing acquisitions at inflated prices or buybacks at the expense of the balance sheet, WM’s leadership has chosen to invest in organic growth opportunities—automation, renewable energy, recycling infrastructure—while maintaining the dividend as a non-negotiable commitment to shareholders. That discipline is rare, and it has earned WM a reputation as one of the better-managed companies in the industrials sector.

There is also a notable emphasis on transparency. Management has consistently communicated clear ESG targets and provided regular updates on progress against those goals. From an investor confidence standpoint, this kind of accountability matters. It reduces uncertainty around the sustainability capital spending program and makes it easier to assess whether the long-term investment thesis remains intact.

Valuation and Stock Performance

At $230.82, WM is trading roughly 5% below its 52-week high of $242.58, offering a slightly more attractive entry point than the stock has provided for much of the past year. The P/E ratio of 34.45 is elevated on an absolute basis, but it is consistent with the premium that the market has historically assigned to WM given the predictability of its cash flows, the durability of its competitive position, and its multi-decade dividend growth track record.

Price-to-book of 9.31 against a book value of $24.79 per share reflects the intangible value embedded in WM’s network of landfills, transfer stations, and long-term municipal contracts—assets that are extraordinarily difficult and expensive to replicate. A competitor cannot simply build a competing landfill; the permitting, regulatory, and capital barriers are prohibitive. That structural moat is real, and it justifies a premium that would look excessive for a more commoditized business.

With a beta of 0.59, WM continues to exhibit significantly lower volatility than the broader market—an important characteristic for dividend-focused portfolios that need to balance income generation with capital preservation. The stock’s market cap of approximately $93 billion reflects its standing as one of the largest and most institutionally owned names in the industrials sector, which contributes further to its price stability. For investors with a multi-year horizon, the current pullback from recent highs looks like a reasonable opportunity to build or add to a position.

Risks and Considerations

Even companies with strong track records face risks, and WM is no exception. The debt load remains a feature of the balance sheet that warrants ongoing attention. While $6.04 billion in operating cash flow provides robust debt service coverage, a sustained rise in interest rates or a tightening of credit markets could incrementally pressure financing costs as existing obligations are refinanced. The company’s leverage is a structural characteristic of the business model, not a sign of financial distress, but it is a factor that limits balance sheet flexibility in stress scenarios.

Regulatory risk is another area to monitor. Waste and recycling operations are governed by an extensive and evolving framework of federal, state, and local regulations covering landfill emissions, recycling standards, environmental compliance, and permitting. Any meaningful tightening of standards—particularly around methane emissions from landfills or hazardous waste handling—could require costly capital upgrades or constrain operational flexibility. WM has generally been proactive in engaging with regulators and positioning itself ahead of anticipated changes, but policy shifts can move faster than even well-prepared companies can respond.

The recycling segment introduces commodity price exposure that the core collection and disposal business does not carry. When prices for recovered materials like cardboard, aluminum, or plastics decline, recycling revenue can compress quickly. This segment adds some earnings volatility to an otherwise highly predictable model, and investors should expect periodic headwinds from this source.

The capital spending program tied to renewable natural gas and recycling automation is both an opportunity and a near-term risk. These are long-duration investments with upfront costs and back-end returns. If project timelines extend or construction costs exceed estimates, free cash flow could be pressured in the interim. The strategic rationale is sound, but execution risk is real in any large-scale infrastructure buildout, and the gap between operating cash flow and free cash flow will remain wide until these projects reach maturity.

Final Thoughts

Waste Management is the kind of company that doesn’t chase trends—it builds long-term value. The business model is anchored in necessity, supported by municipal contracts, and enhanced by years of operational investment that are now flowing through to record levels of operating cash flow. That formula has worked for decades, and the structural characteristics that underpin it—non-discretionary demand, high barriers to entry, pricing power, long-term customer relationships—remain firmly intact.

The 10% dividend increase delivered in 2025, now reflected in a $3.30 annual payout, is the most recent chapter in a 20-plus year story of uninterrupted dividend growth. With a payout ratio of just under 50% and $6.04 billion in operating cash flow backing that commitment, the dividend looks well-supported and positioned for continued growth as the renewable energy and automation investments mature and begin contributing more meaningfully to earnings.

At $230.82, the stock is trading at a modest discount to its recent highs, offering a slightly better entry yield of 1.43% than has been available for much of the past year. The valuation remains premium, but WM has consistently earned that premium through execution, financial discipline, and the kind of quiet, compounding wealth creation that income investors should find genuinely appealing. In a market full of uncertainty, WM continues to be exactly what it has always been—a steady, reliable, and shareholder-friendly business that delivers, year after year.