Updated April 2025

W. R. Berkley has been quietly building value for decades in the specialty insurance world. The company, founded back in 1967 and based out of Greenwich, Connecticut, focuses on property and casualty insurance—specifically, the kind of niche markets where pricing power and underwriting expertise really shine.

What sets WRB apart is how it runs its operations. Instead of the typical top-down model, it lets each of its more than 50 insurance businesses operate independently. That gives it flexibility and focus, which shows in its underwriting discipline and profitability. WRB doesn’t chase growth for the sake of headlines—it plays a long game, sticking to what it knows best and compounding value year after year.

And for income-focused investors, there’s something deeply appealing about that kind of stability. Even though the yield might look modest at first glance, the reliability and financial strength behind it make a strong case for a second look.

📅 Recent Events

A few key things have unfolded over the past year that really matter for dividend-minded investors. First, the stock has seen a strong run—up over 20% in the past 12 months. That’s not a fluke. The performance has been backed by solid earnings growth and consistent fundamentals.

In the most recent quarter, earnings jumped 45% year-over-year, with net income hitting $1.76 billion. Revenue also climbed by nearly 14%, reaching $13.64 billion. That kind of growth isn’t coming from aggressive expansion—it’s the result of consistent execution in underwriting and investment income.

The company also completed a 3-for-2 stock split in July 2024, which is worth noting. Stock splits don’t change the fundamentals, but they do reflect management’s confidence in the future and make the shares more accessible to retail investors.

From a financial standpoint, WRB is sitting on $3.1 billion in cash and carrying a manageable debt load, with a debt-to-equity ratio of just over 36%. Free cash flow for the trailing twelve months came in at a strong $3.33 billion, which gives the company all the firepower it needs to support its dividend and keep growing it over time.

💰 Key Dividend Metrics

📈 Forward Yield: 0.46%

💸 Payout Ratio: 7.19%

⏳ 5-Year Average Yield: 0.61%

🔁 Dividend Growth (Trailing Annual): 3.2%

📆 Most Recent Dividend Date: March 12, 2025

🔔 Ex-Dividend Date: March 3, 2025

📊 Dividend Stability: Near 50 years of uninterrupted payments

🧾 Dividend Overview

Looking at WRB purely through the lens of yield might leave income investors underwhelmed. At just under half a percent, it’s not exactly throwing off tons of income today. But here’s the thing—this is a company that doesn’t overextend itself. The dividend is more of a reflection of discipline than a way to attract attention.

With a payout ratio just above 7%, WRB is keeping most of its profits in-house to reinvest in the business. And for a company that consistently earns a return on equity north of 20%, that’s not a bad trade-off. This is a management team that doesn’t throw money around lightly. They’ve built a reputation for growing book value per share steadily, which tends to benefit long-term holders far more than a flashy dividend ever could.

WRB has also been known to issue special dividends on occasion, though not recently. Still, with their cash position and operating cash flow as strong as they are, the option is definitely on the table when excess capital builds up.

📈 Dividend Growth and Safety

Where WRB really stands out is in the safety and consistency of its dividend. This isn’t the kind of stock you buy for the headline number. It’s the kind you tuck into the portfolio and forget about—until you check back in five or ten years and realize it’s been quietly doing its job all along.

That low payout ratio, backed by nearly $3.7 billion in operating cash flow, gives the dividend a wide margin of safety. And it’s not just the coverage that’s impressive—it’s the company’s ability to grow that dividend, even if in small, regular steps. Over time, those 3-5% hikes compound in a meaningful way.

There’s also the nature of WRB’s business to consider. Specialty insurance isn’t just another corner of the market—it’s a place where underwriting skill really matters. WRB consistently posts combined ratios below 95%, which means it’s profitable on its insurance underwriting even before investment income kicks in.

Add to that a low beta of 0.41, and you’re looking at a stock that behaves more like a bond with growth potential. It doesn’t swing wildly with the market, and that’s exactly what many dividend investors want. Something steady. Something predictable.

WRB might not top any “high-yield” lists, but it delivers where it counts. Strong financials, disciplined growth, a cautious but reliable dividend policy, and the kind of consistency that’s harder and harder to find in today’s market.

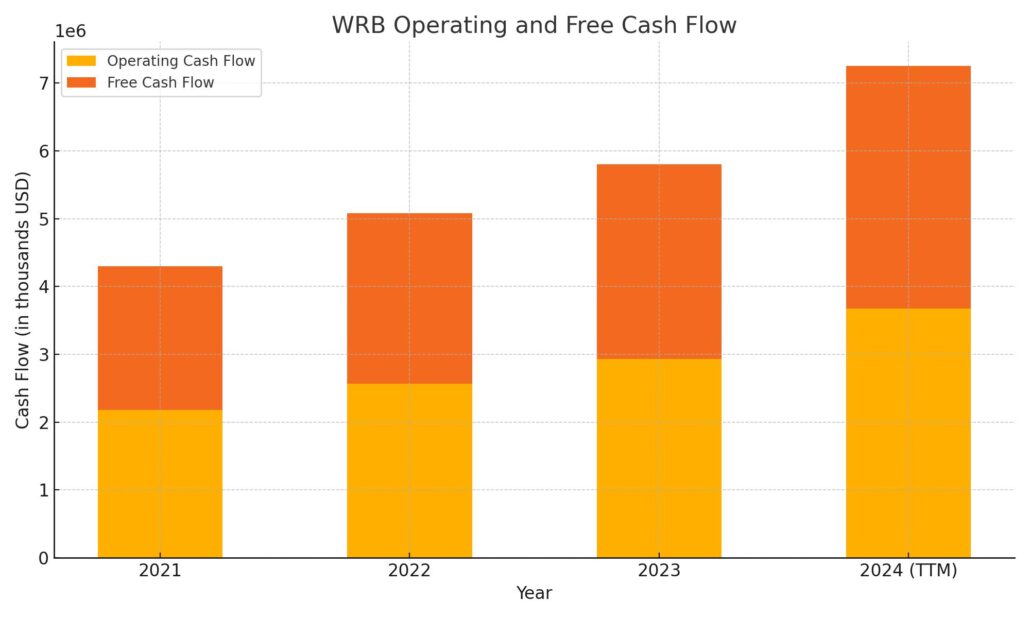

Cash Flow Statement

W. R. Berkley’s cash flow profile over the trailing twelve months reflects a well-balanced and conservatively managed financial engine. Operating cash flow came in at $3.68 billion, showing continued year-over-year growth from $2.93 billion in 2023. That’s a healthy climb, driven by strong underwriting performance and investment income. Capital expenditures remained modest at around $106 million, allowing the company to convert nearly all of its operating inflows into free cash flow—$3.57 billion to be exact. This reinforces how efficiently the company manages its core business while still reinvesting selectively for growth.

On the investing side, WRB used $2.18 billion, in line with prior years, as it continues to put capital to work through securities purchases and business development. Financing cash flow was negative $852 million, largely due to share repurchases of $304 million and dividend payments. The end cash position rose to nearly $2 billion, a clear signal of financial strength. The company issued a small amount of new debt but remained disciplined, avoiding over-leverage. Overall, WRB’s cash flow statement points to a business that generates consistent cash, spends prudently, and returns capital to shareholders with confidence.

Analyst Ratings

📉 In recent developments, W.R. Berkley Corporation has seen a shift in sentiment from some analysts. One notable move came when an analyst at a major investment bank downgraded the stock from a buy to a neutral rating. Interestingly, this wasn’t due to concerns about business fundamentals—in fact, quite the opposite. The analyst actually raised the price target slightly from $73 to $74, but felt the stock had simply run its course in the short term, citing valuation concerns.

📊 The average 12-month price target among analysts now sits around $64.93. Within that, estimates range from a conservative $52 on the low end to a bullish $74 at the high. That spread shows there’s still a good deal of debate over where WRB should be trading, especially as it flirts with historic valuation highs. For long-term holders, this just means the market may be cooling a bit after a strong run-up.

🔍 The reason behind the downgrade centers largely around valuation. The stock is nearing its historical price-to-book ceiling, which naturally dampens near-term upside expectations. However, analysts still point to the company’s strong return on equity and lower exposure to casualty volatility as positives—it’s just that much of that optimism may already be baked into the current share price.

Earning Report Summary

W.R. Berkley closed out the fourth quarter of 2024 on a strong note, putting up numbers that speak to both operational strength and smart execution. The company reported net income of $576 million, a solid jump of 45% compared to the same period last year. That kind of bottom-line growth isn’t something you see every day in the insurance space, especially not paired with the kind of underwriting discipline WRB is known for.

Underwriting Still a Core Strength

One of the highlights was the combined ratio, which came in at 90.2%. That’s well below the break-even mark of 100%, and it shows that WRB continues to write profitable business. Gross premiums written climbed 8.2% to $3.5 billion, and net premiums rose about 8% as well. The company also achieved an average rate increase of 7.7%, not counting workers’ comp. That’s no small feat in a competitive market and speaks to the pricing power they’ve earned in specialty lines.

Investments Lend a Boost

On the investment side, WRB saw another lift. Investment income played a key role in the quarter’s strong performance, thanks in part to higher interest rates working in their favor. With their conservative portfolio and strong balance sheet, even modest gains here move the needle.

A Focused, Nimble Model

The decentralized model W.R. Berkley operates with continues to pay off. Each business unit is given the autonomy to react quickly to market shifts, and it shows in the consistency of their results. Return on equity came in at an impressive 30.9%, which really reflects how efficiently they’re deploying capital.

All in all, this was a confident quarter from a company that knows its strengths and sticks to them. Between strong underwriting, smart rate increases, and steady investment income, WRB heads into the new year with solid momentum.

Chart Analysis

The stock chart for WRB over the past year shows a steady and impressive climb, especially in the second half of the timeframe. After spending the early months stuck in a narrow range around the low $50s, the price found its footing mid-year and began trending upward in a much more consistent way.

Moving Averages and Trend Strength

The 50-day moving average (red line) crossed above the 200-day moving average (blue line) around July, a technical signal often read as a bullish indicator. Since then, both moving averages have continued rising, with the 50-day remaining comfortably above the 200-day throughout the rest of the year. That separation shows a healthy and sustained uptrend, not just a short-term spike.

Volume Patterns

Volume was relatively stable for most of the year, though some notable spikes appear, particularly in late March. These volume bursts tend to align with strong upward price movements, suggesting accumulation and institutional interest rather than retail-driven volatility. There were no drastic sell-offs or volume blowouts on down days, which points to confidence behind the price action.

Momentum and RSI

The relative strength index (RSI) started the year in the lower range but steadily climbed alongside price gains. By the final week of the chart, RSI had broken above the 70 mark, which puts it in overbought territory. While that might suggest short-term caution, overbought conditions during strong trends can persist longer than expected, especially when supported by positive earnings and sentiment.

Overall Technical Picture

The price recently surged to its highest level on the chart, briefly peaking above 72 before pulling back slightly. That parabolic move coincided with high volume and an RSI that’s now stretched, so some short-term cooling wouldn’t be surprising. Still, the longer-term setup remains constructive. The trend is upward, the volume supports the move, and momentum has built gradually—not suddenly—throughout the year.

WRB’s price action tells the story of a stock that’s been steadily gaining strength. It’s the kind of pattern that reflects a well-managed company consistently executing on its strategy, with technicals that mirror strong fundamentals rather than speculative hype.

Management Team

W.R. Berkley Corporation is guided by a leadership team that’s deeply connected to the company’s roots. Executive Chairman William R. Berkley, who founded the company in 1967, remains an influential figure, bringing decades of industry knowledge and a long-term view that has helped shape the company’s identity. Alongside him, his son W. Robert Berkley Jr. serves as President and Chief Executive Officer. This continuity in leadership has created a strong cultural foundation with clear direction and stability.

The team is further supported by experienced executives like Richard M. Baio, the Chief Financial Officer, who oversees capital management with a disciplined hand. Lucille T. Sgaglione, another long-standing EVP, plays a major role in the company’s operations and strategic planning. What’s unique about W.R. Berkley is its decentralized structure—each business unit operates with autonomy, encouraging innovation and responsiveness across the board. This setup has been key in allowing WRB to adapt quickly to shifts in market conditions while maintaining risk control and underwriting quality.

Valuation and Stock Performance

Over the past year, WRB’s stock has delivered strong returns, climbing roughly 23% and comfortably outpacing the broader market. That performance isn’t a one-time spike—it’s part of a longer trend. Over the last five years, total returns have surpassed 240%, a reflection of the company’s consistent earnings growth, careful underwriting, and disciplined capital allocation.

The stock recently traded around $69.75, which sits just under some analysts’ fair value estimates in the low $70s. That slight discount could reflect the market’s cautious stance on valuation after a solid run-up, but the fundamentals haven’t changed. WRB is still posting impressive earnings, and its return on equity remains near the top of the industry. Its forward price-to-earnings ratio is in the mid-teens—reasonable for a business with this kind of reliability and growth history.

One development that recently caught investor attention is Mitsui Sumitomo Insurance’s plan to acquire a 15% stake in W.R. Berkley. While not yet complete, this partnership could be a meaningful boost for the company’s international reach and distribution capabilities. The market reacted positively to the news, seeing it as validation of WRB’s quality and strategic value.

Risks and Considerations

Like any insurer, WRB faces headwinds—some structural, some cyclical. One area worth watching is exposure to climate-related financial risks. The company has some holdings in sectors that are vulnerable to both physical climate events and regulatory transitions, such as energy and pipelines. As the landscape continues to shift, these investments could come under pressure, particularly if public or investor scrutiny intensifies.

Beyond environmental risks, the insurance business itself is inherently cyclical. Underwriting margins can compress in soft markets, and investment income—though strong lately—can swing with interest rates and market volatility. There’s also always a risk of large catastrophic losses in the P&C world, which, even with reinsurance, can impact earnings sharply in a bad quarter. The decentralized model offers flexibility, but it also requires consistently strong leadership across each operating unit to keep everything moving in the same direction.

Final Thoughts

W.R. Berkley continues to deliver on the traits that long-term investors value: steady growth, thoughtful capital allocation, and a disciplined underwriting culture. The leadership’s long tenure and hands-on approach give the company a sense of continuity that’s increasingly rare. With performance tracking well above market averages and fundamentals holding strong, WRB is positioned for continued relevance in a competitive space.

That said, it’s not immune to macro pressures or sector-specific risks. Changes in regulation, interest rate dynamics, or broader economic conditions could all test the company’s flexibility. But its conservative balance sheet, strong cash generation, and consistent execution provide a good deal of insulation. It’s a name that has built trust over time by doing what it says and staying true to its core strengths.