Updated 2/23/26

Vulcan Materials is firmly rooted in something more fundamental—supplying the materials that build the very roads we drive on and the cities we live in. Headquartered in Birmingham, Alabama, Vulcan is the nation’s largest producer of construction aggregates like crushed stone, sand, and gravel.

While it may not have the buzz of a tech startup, Vulcan’s relevance is anything but temporary. As long as the country continues investing in infrastructure, this company will remain essential. For dividend investors, that steady demand for its products has translated into a long-term commitment to returning capital to shareholders. The dividend isn’t just an afterthought here—it’s part of the company’s rhythm.

Recent Events

Vulcan Materials has traded in a wide band over the past twelve months, ranging from a low of $215.08 to a high of $331.09. Shares currently sit at $304.36, representing a meaningful recovery from the lower end of that range and putting the stock within striking distance of its 52-week peak. The rebound reflects renewed investor confidence in the infrastructure spending backdrop and Vulcan’s continued ability to grow earnings per share.

Revenue for the trailing twelve months reached $7.94 billion, a solid top-line showing for a business whose pricing discipline has been one of its defining characteristics in recent years. Net income climbed to $1.08 billion, with EPS coming in at $8.46—a notable step up from the $7.53 adjusted figure reported for full-year 2024, underscoring consistent bottom-line momentum. Profit margins expanded to 13.56%, and the company generated $1.81 billion in operating cash flow, demonstrating that Vulcan’s earnings are being converted to cash at a healthy rate.

Capital expenditures remain elevated as management continues investing in long-term capacity, with free cash flow settling at $409 million after those outlays. That figure is tighter than prior periods but reflects deliberate reinvestment rather than any deterioration in business quality. Return on equity stands at 12.97% and return on assets at 5.78%, both consistent with a capital-intensive aggregates business operating at a high level.

Key Dividend Metrics

📅 Dividend Date: November 10, 2025 (most recent payment)

💵 Forward Annual Dividend Rate: $2.08

📈 Dividend Yield: 0.64% (Forward)

📊 Payout Ratio: 22.79%

🔁 5-Year Average Yield: 0.84%

💰 Last Dividend Payment: $0.49 per share

📅 Last Split: 3-for-1, March 11, 1999

Dividend Overview

Vulcan Materials is not a stock you buy for yield. At 0.64%, the forward dividend sits below the company’s own five-year average yield of 0.84%, which itself was never a number that drew income-focused investors in from the sidelines. What you’re buying here is reliability paired with consistent growth, wrapped in one of the most defensible business models in the materials sector.

The payout ratio of 22.79% is extraordinarily conservative for a company generating over $8 per share in earnings. Vulcan is retaining the vast majority of its profits to fund capital expenditure, service debt, and pursue opportunistic acquisitions—all of which serve the long-term health of the business and, by extension, future dividend capacity. There’s nothing precarious about a $2.08 annual dividend sitting on top of $8.46 in EPS.

For dividend investors who prioritize safety and durability over headline yield, Vulcan’s approach should be reassuring. The company has no need to stretch its payout to attract shareholders, and that conservatism is precisely what makes the dividend dependable across economic cycles.

Dividend Growth and Safety

The dividend growth story at Vulcan is one of steady, deliberate progress. Looking back through the recent dividend history, the quarterly payment moved from $0.43 per share through 2023, stepped up to $0.46 in 2024, and then climbed again to $0.49 in 2025—bringing the annualized rate to $2.08. That represents a roughly 14% increase in the per-share quarterly payment over just two years, and a broader multi-year trajectory that has seen the annual dividend rise significantly from the $1.16 level of five years ago.

On the safety front, the numbers speak clearly. Operating cash flow of $1.81 billion dwarfs the roughly $274 million required to fund the annual dividend at current share counts. Even after capital expenditures, the company retains meaningful flexibility. The payout ratio of under 23% means Vulcan could face a significant earnings shock and still cover its dividend without breaking a sweat.

Structurally, Vulcan’s business model provides a natural hedge against demand volatility. Infrastructure projects—highways, bridges, water systems—operate on multi-year planning and funding cycles, which means Vulcan’s order visibility extends well beyond a single quarter. Public spending through legislation like the Infrastructure Investment and Jobs Act continues to support aggregates demand at the federal and state level, providing a durable tailwind that benefits Vulcan more directly than almost any other public company.

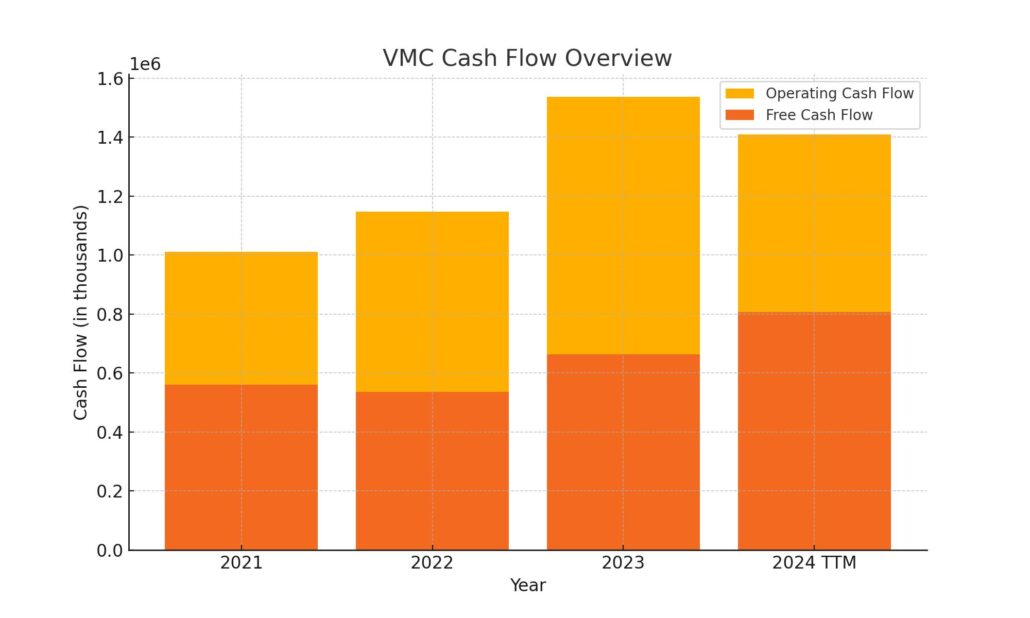

Cash Flow Statement

Over the trailing twelve months, Vulcan Materials generated $1.81 billion in operating cash flow, a strong result that reflects the company’s pricing power and the persistent demand for construction aggregates across both public infrastructure and private construction markets. This figure represents a meaningful increase from prior periods and confirms that Vulcan’s earnings quality remains high—cash is tracking income closely. Capital expenditures came in at approximately $1.40 billion, reflecting the company’s continued commitment to maintaining and expanding its quarry network and production capacity.

After those capital outlays, free cash flow came in at $409 million—tighter than in some prior years but a direct consequence of elevated reinvestment. That reinvestment is not a sign of financial stress; it’s a reflection of management’s confidence in the long-term demand picture. The dividend remains extraordinarily well covered at the free cash flow level, and the company’s $1.08 billion in net income provides further assurance that capital allocation decisions are being made from a position of strength, not necessity. Book value per share stands at $65.28, with a price-to-book ratio of 4.66x, consistent with the premium the market assigns to Vulcan’s irreplaceable asset base.

Analyst Ratings

With VMC trading at $304.36 and carrying a P/E ratio of nearly 36x, analyst sentiment has generally remained constructive, reflecting confidence in Vulcan’s pricing power and its exposure to federally funded infrastructure spending. The stock’s recovery from the low $200s to current levels suggests the market has absorbed prior concerns about weather-related volume headwinds and is increasingly focused on the earnings growth trajectory.

Based on the company’s financial profile—$8.46 in EPS, expanding margins, and $1.81 billion in operating cash flow—analysts covering the aggregates space have historically rewarded Vulcan with above-market multiples, citing the scarcity value of its quarry network and the long-tailed nature of infrastructure demand. The current P/E of 35.98x is elevated relative to the broader materials sector, which typically trades closer to 15–20x earnings, but Vulcan has consistently commanded that premium due to its market-leading position and consistent execution.

The consensus view heading into 2026 appears to be that Vulcan remains a high-quality compounder worth owning at current prices for long-term investors, while acknowledging that near-term upside may be more limited given how far the stock has already recovered from its 2025 lows. Price targets from prior coverage cycles clustered in the $285–$325 range, and with VMC now at $304, the stock sits roughly in the middle of that band.

Earnings Report Summary

Vulcan Materials closed out fiscal 2025 with results that reinforced its reputation as one of the most consistently profitable businesses in the materials sector. Full-year revenue reached $7.94 billion, and net income of $1.08 billion translated to EPS of $8.46—up from the $7.53 adjusted figure in 2024, a year-over-year improvement of roughly 12%. Profit margins expanded to 13.56%, and operating cash flow of $1.81 billion confirmed that the earnings growth is real and cash-backed.

Aggregates Continue to Drive the Story

The aggregates segment remained the primary earnings engine, as it has been for years. Pricing discipline continued to be the central narrative, with management successfully pushing through per-ton price increases that more than offset any softness in shipment volumes. The ability to grow revenue and earnings in an environment where volume may not always cooperate is the defining characteristic of Vulcan’s competitive moat—its quarries are often the only viable local source of construction aggregates, giving it genuine pricing authority.

Margins Expand as Cost Controls Hold

One of the cleaner stories in the most recent results was margin expansion. With a profit margin of 13.56% and return on equity of 12.97%, the company demonstrated that it can grow earnings without sacrificing financial discipline. Selling, general, and administrative expenses have remained well-managed as a percentage of revenue, and the incremental margins on pricing gains continue to flow through to the bottom line at an attractive rate.

Capital Deployment and Balance Sheet

Capital expenditures remained elevated, consistent with management’s multi-year investment cycle in quarry development and operational infrastructure. Free cash flow of $409 million, while lower than in some prior years, reflects that investment rather than any deterioration in business fundamentals. The company’s book value per share of $65.28 and a return on assets of 5.78% are characteristic of a capital-intensive business generating solid returns on a large and growing asset base.

Outlook for 2026

Management enters 2026 with a constructive demand backdrop. Federal infrastructure funding continues to work its way through state-level project pipelines, and residential and commercial construction activity, while mixed regionally, supports aggregates demand across Vulcan’s geographic footprint. Pricing is expected to remain a tailwind, and the company’s cost structure appears well-positioned to support continued margin improvement. Capital expenditure guidance will be a key variable to watch, as it will determine how much of the operating cash flow converts to free cash available for dividends and shareholder returns.

Management Team

At the helm of Vulcan Materials Company is a leadership team with deep industry experience and a clear vision for the company’s future. Chairman and Chief Executive Officer J. Thomas Hill has been steering the company since 2014, bringing over two decades of experience within Vulcan to the role. His tenure has been marked by strategic growth initiatives, a focus on operational excellence, and a consistent track record of delivering shareholder value through disciplined capital allocation.

Supporting him is Mary Andrews Carlisle, who serves as Senior Vice President and Chief Financial Officer. Since joining Vulcan in 2006, Carlisle has held various leadership positions within the finance department, demonstrating deep expertise in financial planning, capital markets, and long-term balance sheet management.

Thompson S. (Tom) Baker II serves as President, having previously held the role of Chief Operating Officer. Baker’s extensive experience across multiple divisions gives him a comprehensive understanding of the company’s day-to-day operations and long-term strategic priorities.

The broader executive team includes Chief Strategy Officer Stanley G. Bass and Chief Operating Officer Ronnie Pruitt, each contributing meaningful experience in operations and strategic planning. This collective depth of leadership positions Vulcan Materials to continue navigating the demands of the construction materials industry with consistency and discipline.

Valuation and Stock Performance

Vulcan Materials shares are trading at $304.36 as of February 23, 2026, sitting comfortably above the midpoint of the 52-week range of $215.08 to $331.09. The stock has recovered substantially from its lows, and investors who added during the weakness in the $215–$240 range have been well rewarded. At current prices, VMC carries a market capitalization of approximately $40.2 billion, reflecting its status as the dominant player in U.S. construction aggregates.

The P/E ratio of 35.98x is the central valuation debate for anyone considering a position today. At nearly 36 times trailing earnings, Vulcan is priced for continued execution and ongoing margin expansion—there’s no meaningful margin of safety baked into that multiple. The price-to-book ratio of 4.66x, against book value of $65.28 per share, similarly reflects a premium to intrinsic asset value that requires the business to keep compounding at a healthy rate to justify. Beta of 1.05 suggests the stock moves roughly in line with the broader market, which is a reasonable profile for a business this tied to economic activity.

The elevated multiple is not entirely without justification. Vulcan’s quarry network is a genuinely irreplaceable asset—permitting new quarries is extraordinarily difficult, which means existing operations carry a structural competitive advantage that doesn’t depreciate in the traditional sense. The infrastructure spending tailwind from multi-year federal legislation is real and ongoing. And management has demonstrated consistent pricing discipline that translates volume into earnings more efficiently than most cyclical peers. Even so, at 36x earnings, the stock demands flawless execution.

Risks and Considerations

Investing in Vulcan Materials carries risks that are both industry-specific and financial in nature. The company’s quarrying operations involve inherent physical risks including pit wall failures, flooding, and equipment damage, any of which can disrupt production, increase costs, or delay project timelines. These are ongoing operational realities in the aggregates business that management works to mitigate but cannot fully eliminate.

Regulatory risk is a persistent consideration. Environmental compliance requirements for mining operations are stringent and subject to change. Vulcan has faced compliance issues in the past, and any escalation in environmental enforcement or permitting restrictions could affect operational flexibility and add to costs.

On the financial side, capital expenditures are running high, which is compressing free cash flow even as operating cash flow remains strong. If the infrastructure spending environment softens or project delays push out demand, Vulcan could find itself with elevated capex commitments against a weaker revenue backdrop. Short interest of approximately 4.7 million shares is modest relative to the float, but any negative earnings surprise could amplify downside given how much optimism is embedded in the current valuation.

Finally, the valuation itself is a risk. At 35.98x earnings, VMC is priced well above both historical norms and sector peers. If revenue growth decelerates, margins plateau, or interest rates remain elevated—increasing competition for capital from fixed income alternatives—the multiple compression alone could produce meaningful downside even if the underlying business continues to perform reasonably well.

Final Thoughts

Vulcan Materials remains one of the highest-quality businesses in the materials sector, and the financial results through early 2026 do nothing to challenge that characterization. Revenue approaching $8 billion, net income above $1 billion, EPS of $8.46, and operating cash flow of $1.81 billion collectively paint the picture of a company executing at a high level. The dividend, now at $2.08 annually after consecutive annual increases, is covered many times over and backed by a business model with genuine structural durability.

The honest question for dividend growth investors today is whether $304 per share is the right entry point. The yield of 0.64% is below the company’s own historical average, and the P/E of nearly 36x leaves limited room for error. For investors already holding VMC at lower cost bases, the case for continuing to hold is straightforward—the dividend is safe, growing, and supported by a business with a long runway. For new positions, patience for a better entry price could be rewarded if market volatility creates an opportunity to buy this high-quality compounder at a more attractive valuation. Vulcan’s long-term prospects remain intact; the question is simply one of price.