Updated April 2025

Visa doesn’t scream “dividend stock” the way some others do, but that’s never been the point. It’s a different kind of income play—quietly powerful, incredibly consistent, and built for the long haul. This is a company that knows how to grow, return capital, and stay out of trouble, which is exactly what long-term investors should want in a dividend name.

While the yield is modest, the bigger picture here is one of steady compounding. Visa isn’t a lender. It doesn’t take on credit risk. It simply facilitates payments—earning a cut every time money moves. And in a world leaning harder into digital transactions, Visa sits comfortably in the center of that trend.

Recent Events

Visa’s most recent quarterly results didn’t make huge headlines, but the fundamentals remain rock solid. Revenue rose over 10% year over year, hitting nearly $36.8 billion on a trailing basis. Net income came in at $19.7 billion, and earnings per share for the trailing twelve months reached $9.91.

What’s more telling is how profitable this company continues to be. Operating margins are nearly 69%, which is rare air. That level of efficiency gives Visa massive flexibility—whether it’s increasing dividends, buying back stock, or investing in new tech to stay ahead of the curve.

The stock itself has done well lately. Over the past year, it’s gained more than 26%, outpacing the broader S&P 500. Even with some pre-market volatility, Visa continues to draw long-term money, and there’s good reason for that.

Key Dividend Metrics

💰 Forward Annual Dividend Yield: 0.68%

📈 5-Year Average Yield: 0.67%

🧾 Forward Annual Dividend Rate: $2.36 per share

🔄 Payout Ratio: 21.67%

📆 Dividend Growth Streak: 15+ years

🚀 5-Year Dividend CAGR: Over 17%

🧮 Free Cash Flow Payout: comfortably under 40%

🔍 Last Ex-Dividend Date: February 11, 2025

📅 Most Recent Dividend: March 3, 2025

Dividend Overview

Visa isn’t offering a big yield right now. At just under 0.7%, it won’t turn heads among investors who focus strictly on income. But for those looking at the full picture—quality, consistency, and growth—it’s a very different story.

This company has raised its dividend every year since going public. That kind of consistency is rare, and it shows a clear commitment to returning value to shareholders in a responsible way. More importantly, Visa doesn’t have to stretch to do it. The payout ratio is below 22%, giving it a massive cushion to continue raising that dividend even if earnings growth slows.

The dividend is backed by real financial strength, not just good intentions. Visa’s business throws off enormous free cash flow and has no need to borrow heavily to sustain payments. This isn’t a stretch yield—it’s a measured, well-supported return.

Dividend Growth and Safety

This is where Visa really shines. Over the past five years, the company has more than doubled its dividend payout. That works out to a compound annual growth rate of over 17%, which is impressive by any standard, especially for a mega-cap company.

The real beauty here is how little stress that growth puts on the company’s financials. With over $21 billion in operating cash flow last year and less than $14 billion in capital outlays, Visa has plenty of dry powder left even after dividends and share repurchases.

Debt isn’t an issue, either. Total debt is just over $20 billion, but there’s $14 billion in cash on the books, and the debt-to-equity ratio remains comfortably under control. The current ratio is just over 1.1, showing a healthy balance sheet with enough liquidity for any short-term needs.

Put simply, Visa is in a sweet spot for dividend investors. It’s not a high-yield stock today, but it offers something arguably more valuable: high-quality, low-risk dividend growth that compounds over time. This is the kind of name you quietly accumulate and let do its thing. Over a 5-10 year horizon, the results speak for themselves.

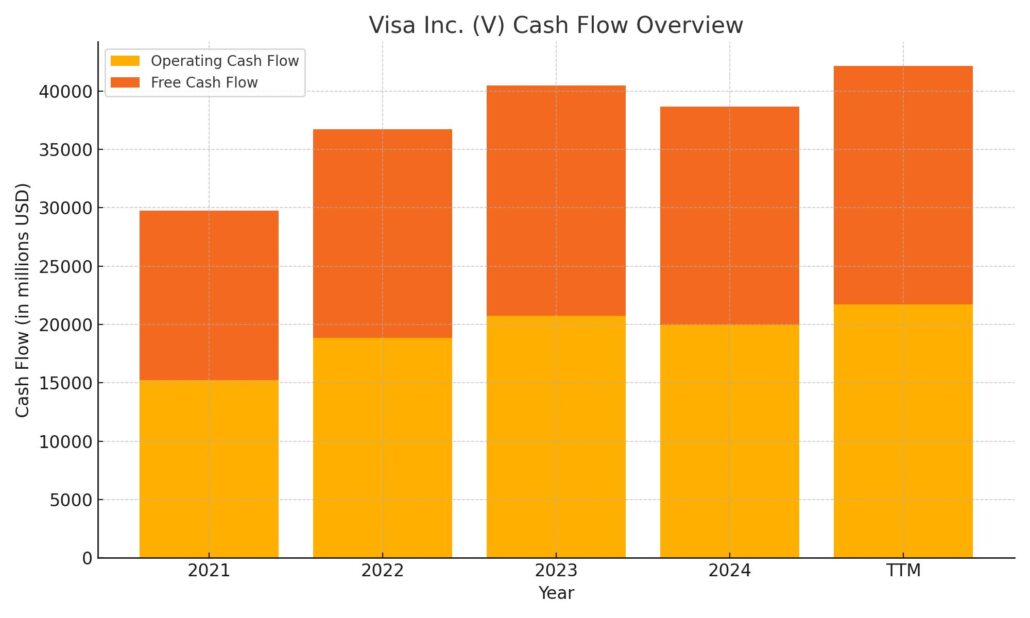

Cash Flow Statement

Visa’s cash flow remains a standout feature of its financial profile, reflecting both operational efficiency and consistent shareholder returns. Over the trailing twelve months, the company produced $21.7 billion in operating cash flow, an increase from the prior year and a sign of healthy transaction volumes and disciplined cost controls. Even after capital expenditures of $1.34 billion, Visa still generated $20.4 billion in free cash flow—a figure that reinforces just how strong and self-sustaining its business model is.

On the financing side, Visa returned a significant amount of capital to shareholders, with $17.1 billion spent on share repurchases and a total financing outflow of nearly $21.7 billion. Despite this, its cash position remains solid, ending the period with over $20.3 billion on hand. That stability, paired with modest investing activity and low interest costs, keeps Visa well-positioned to support ongoing dividend growth, share buybacks, and long-term strategic investments without straining its balance sheet.

Analyst Ratings

📈 Visa Inc. has recently attracted upbeat sentiment from analysts, with several firms signaling confidence in its outlook. 🟢 Seaport Research Partners upgraded the stock to a buy rating, pointing to Visa’s strong footprint in the U.S. payments landscape and its relatively attractive valuation when stacked against industry peers. The upgrade also came with anticipation around Visa’s upcoming investor day, which is expected to provide clarity on future strategy and possibly serve as a catalyst for the stock.

🌟 Morgan Stanley added further momentum by naming Visa its top pick for 2025. Analysts there highlighted a few key drivers behind the bullish stance. First, investor interest in the payments space is gaining traction again. Second, despite economic concerns, consumer behavior has remained solid and continues to lean on credit card usage—Visa’s bread and butter. Third, fintechs are evolving toward more focused and profitable models, which plays to Visa’s strengths as a platform provider. On top of that, expectations for increased M&A activity and a friendlier regulatory backdrop have also helped drive their positive view. Morgan Stanley bumped Visa’s price target up to $371 while maintaining an overweight rating.

🎯 Across the board, the consensus analyst price target for Visa now sits around $355.84. That implies some upside from where the stock is currently trading, and the sentiment largely reflects Visa’s consistently strong financials and its resilience in a shifting economic landscape.

Earning Report Summary

Visa’s most recent earnings report came in strong, giving investors more reasons to feel confident about where the company is headed. It wasn’t just a beat on the top and bottom lines—it was the kind of quarter that reinforces how steady Visa’s business really is, even with all the noise out there in the economy.

Revenue and Profit Show Solid Growth

Revenue for the quarter hit $9.6 billion, up 12% from the same time last year. That kind of growth isn’t easy to come by for a company of Visa’s size, but it shows how consistent spending trends and cross-border transactions are helping fuel results. Net income landed at $5.3 billion, with earnings per share coming in at $2.65—a healthy 17% increase. That kind of profitability reflects a well-oiled business model and tight control over expenses.

Transaction Volume Keeps Climbing

Visa processed over 61 billion transactions during the quarter. That’s 10% more than the same period a year ago. Payments volume grew 7%, and cross-border volume—which is especially important for Visa’s international growth—was up 13%, excluding intra-Europe activity. People are still swiping, tapping, and clicking at a healthy pace.

Revenue Streams Stay Balanced

Service revenue climbed to $4.2 billion, while data processing brought in $4.6 billion, both up about 8%. International transaction revenue followed suit with a 9% gain, landing at $3.5 billion. These three streams continue to move together and reinforce how diversified Visa’s revenue engine really is.

Expenses Rise, But It’s Controlled

Operating expenses did edge up, coming in at $3.3 billion for the quarter, a 7% increase. Most of that came from marketing and people costs—areas where Visa is clearly still investing for the long term. Even so, the company managed to hold onto a strong operating margin, which speaks to how well it’s managing the overall cost structure.

Strong Financial Position

Visa wrapped the quarter with over $17 billion in cash and investments. That’s a solid war chest that gives the company plenty of options—whether it’s buying back shares, paying dividends, or investing in future growth. The company’s effective tax rate came in at 16.5%, a slight tailwind that helped boost net income even more.

All in all, this was another quarter that shows Visa’s steady hand in a shifting payments landscape. Business is growing, costs are in check, and the long-term fundamentals remain firmly intact.

Chart Analysis

Visa (V) has shown a strong recovery and steady uptrend over the past year, and the current technical picture supports that narrative. What stands out most is the shift in momentum that began around October, where the price pushed decisively above the 200-day moving average and hasn’t looked back since.

Moving Averages and Price Momentum

For much of the early part of the chart, the price was trading below the 50-day moving average and struggling to gain traction. That changed in the fall. The 50-day MA (red line) began to curl upward and crossed above the 200-day MA (blue line) in what’s commonly referred to as a golden cross. Since then, price has stayed comfortably above both, which typically reflects a strong bullish structure.

While the stock experienced a sharp pullback in March, it held above the 200-day moving average and bounced back quickly—suggesting support remains firm around that zone. The 50-day continues to act as dynamic support, keeping the trend healthy.

Volume and Participation

Volume has remained steady, with a few noticeable spikes during upswings, especially in the October to February run-up. That kind of volume action during rallies signals strong participation and conviction from buyers. There hasn’t been a significant surge in selling volume, which also helps keep the bias tilted upward.

RSI and Momentum Shifts

The Relative Strength Index (RSI) has done a good job of tracking the ebbs and flows of momentum throughout the year. There were periods of overbought readings in November and late January, followed by cooling-off phases that kept the uptrend from overheating. The RSI recently rebounded from near the 30 level and is now climbing again, which could be an early sign of renewed strength.

Overall, the chart reflects a healthy, trend-following name that has gone through normal consolidations and come out stronger. As long as the price continues to hold above the longer-term averages and buyers step in on pullbacks, the technical foundation remains supportive of further strength ahead.

Management Team

Visa’s leadership is built around a group of highly experienced professionals who bring a mix of payments expertise, technology know-how, and global perspective. Leading the charge is CEO Ryan McInerney, who took on the role in 2023 after serving a decade as Visa’s President. His background in consumer banking and technology has made him a steady hand as Visa navigates a fast-changing industry.

Backing him is CFO Chris Suh, who joined from Electronic Arts. His financial discipline and operational insight from a tech-heavy environment add a useful layer to Visa’s executive bench. Other key figures include Charlotte Hogg, who oversees the company’s European operations, and Rajat Taneja, Visa’s President of Technology, who plays a pivotal role in shaping the company’s infrastructure and innovation. This team collectively brings deep industry understanding and a forward-looking mindset, which continues to keep Visa aligned with its long-term goals.

Valuation and Stock Performance

Visa shares have climbed steadily over the past year, currently trading around $346.33. The stock has been in a solid uptrend since last fall and has benefited from strong earnings, steady macro trends in digital payments, and renewed investor appetite for dependable growth names. Over the last 52 weeks, shares have traded between $252.70 and $366.54, showing a wide but upward-moving range.

The trailing price-to-earnings ratio stands at 34.91, with a forward P/E of 30.67. That suggests investors are still willing to pay a premium for consistent earnings and free cash flow growth. The PEG ratio of 2.28 indicates that while it’s not cheap on a growth-adjusted basis, it’s far from frothy when weighed against the company’s high margins and stability. The stock’s beta of 0.94 means it tends to be a bit less volatile than the market, another plus for steady hands.

The consensus analyst price target sits around $355.84, pointing to a bit of room for upside. Analyst sentiment is largely constructive, with most maintaining buy or overweight ratings. With strong fundamentals and a defensible market position, the stock continues to be viewed as a core holding in many institutional portfolios.

Risks and Considerations

Despite the strong setup, Visa isn’t without potential headwinds. Regulatory pressure is one to keep an eye on, especially in Europe and the UK, where investigations into payment fees and anti-competitive practices are ongoing. The outcomes of these could impact how much Visa can charge merchants in certain markets, potentially trimming margins down the road.

There’s also growing noise around the European Central Bank’s concern about the region’s dependence on U.S.-based payment networks. This could prompt governments and local institutions to push for regional alternatives, which might limit Visa’s long-term growth in those areas.

Then there’s competition. Fintechs continue to chip away at traditional payment channels, and while Visa has done a good job partnering with many of them, the pace of change in the payments ecosystem remains a moving target. Staying ahead means continued investment in AI, security, and digital infrastructure—none of which come cheap.

Final Thoughts

Visa remains a company that consistently delivers. The leadership team is stable and experienced, the financials are clean, and the long-term story hasn’t changed. It’s a business that benefits from scale, trust, and massive network effects, and those factors don’t erode overnight. While regulatory and competitive risks exist, Visa has the cash flow, people, and infrastructure to adapt as needed.

Its valuation reflects the quality of the business, and that’s not likely to change any time soon. Whether it’s leveraging AI to improve fraud detection, expanding in emerging markets, or adapting to evolving payment preferences, Visa continues to move with intent. The focus stays on execution, and so far, it’s showing up where it matters most—on the bottom line.