Updated 2/23/26

Virtus Investment Partners is a well-structured asset manager with a disciplined approach to capital returns and a shareholder-friendly dividend policy. The company runs a multi-boutique model—think of it as a network of specialized investment teams under one roof. Each group brings its own style, strategy, and edge. The goal? Diversify not just across asset classes, but across minds and methodologies. While the stock price has taken a significant hit—falling nearly 36% from its 52-week high of $215.06 down to the current $137.01—long-term income investors may find something genuinely compelling here. The payout has actually grown, and the balance sheet behind it remains intact.

🧮 Key Dividend Metrics

💰 Forward Yield: 6.33%

📈 5-Year Average Yield: 2.66%

📆 Last Dividend Payment: January 30, 2026

🔻 Payout Ratio: 45.82%

💵 Annual Dividend: $9.60

🧾 Last Quarterly Dividend: $2.40

📊 Beta: 1.44

Recent Events

The past year has been a difficult one for VRTS shareholders. Shares have slid from a 52-week peak of $215.06 all the way down to $137.01, representing a decline of more than 36% from the high. The stock is now trading near the very bottom of its 52-week range of $134.81 to $215.06, a range that underscores just how sharply sentiment has shifted against the asset management space.

Despite the price weakness, the underlying business has continued to generate meaningful earnings. EPS sits at $19.97 on a trailing basis, and return on equity is 13.39%. Net income came in at approximately $138.4 million on revenue of $852.9 million, producing a profit margin of 16.23%. These are not the numbers of a company in operational distress—they are the numbers of a company whose stock has been punished beyond what the fundamentals seem to justify.

Market cap has compressed to roughly $925 million, a level that places VRTS firmly in small-cap territory despite earnings power that would suggest a meaningfully higher valuation. For income-focused investors, that compression has one notable side effect: it has pushed the dividend yield to 6.33%, the most attractive entry point the stock has offered in years.

Dividend Overview

The dividend story at VRTS has only gotten better, even as the stock has declined. The company now pays a $2.40 quarterly dividend, adding up to $9.60 annually, and at the current price of $137.01 that translates to a forward yield of 6.33%. To put that in context against the stock’s five-year average yield of 2.66%, investors buying today are locking in more than double the historical norm—not because the company stretched its payout recklessly, but because the price has fallen while dividends continued to grow.

The payout ratio sits at a conservative 45.82% against trailing EPS of $19.97. That means the company is retaining more than half of its earnings even after funding a dividend that most income investors would consider generous. There is no sign of financial strain behind the payout—it is well-supported by real earnings power.

The dividend increase that took effect with the October 2025 payment—moving from $2.25 to $2.40 per quarter—represents a 6.7% raise, and marks the continuation of a pattern where Virtus has steadily stepped up its quarterly payout over time. Institutional ownership remains high, which reflects continued confidence from large, sophisticated investors in the company’s long-term capital return discipline.

Dividend Growth and Safety

Virtus has demonstrated a clear and consistent pattern of dividend increases over the past several years. Starting from $1.65 per quarter in early 2023, the company moved to $1.90 later that year, then to $2.25 in late 2024, and most recently raised the quarterly rate to $2.40 in October 2025. That progression represents cumulative quarterly dividend growth of roughly 45% in less than three years—a track record that stands out even among companies marketed specifically as dividend growers.

The safety profile behind these payments is solid. With EPS of $19.97 and a quarterly dividend of $2.40, coverage is more than comfortable. The payout ratio of 45.82% leaves ample room to maintain or grow the dividend even if earnings face near-term pressure. Return on equity of 13.39% and a profit margin above 16% suggest the business continues to generate meaningful profits from its asset management operations.

The balance sheet provides additional support. While specific operating and free cash flow figures are not available for the current period, the company’s earnings-based dividend coverage ratio is strong, and with a book value per share of $136.03 nearly matching the current stock price of $137.01, investors are essentially buying the company at close to tangible asset value while collecting a 6.33% yield. The stock’s beta of 1.44 does mean price swings will be more pronounced than the market average, but that volatility has created an income opportunity rather than a fundamental risk to the dividend.

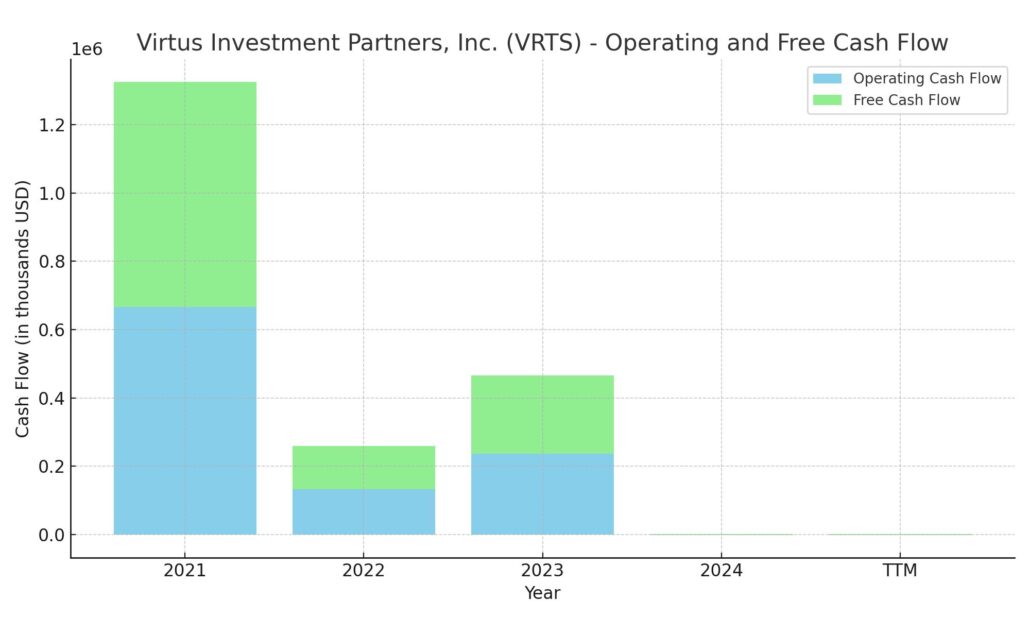

Cash Flow Statement

Virtus Investment Partners’ cash flow statement tells a story of a company in transition. Over the trailing twelve months (TTM), operating cash flow has collapsed to just $1.76 million, a sharp drop from $237 million in 2023 and over $665 million in 2021. That’s a significant decline and reflects a shift in the firm’s internal capital dynamics, possibly tied to lower performance fees or changes in working capital. At the same time, free cash flow turned slightly negative at -$3.8 million, compared to a robust $228 million just a year ago.

Despite this drop in core cash generation, the financing side shows a notable influx of capital. The company issued over $1 billion in debt and repaid about $806 million, signaling some refinancing or restructuring activity. There was also nearly $45 million spent on share repurchases, maintaining a steady capital return policy even amid tighter cash flows. While investing outflows of roughly $17 million stayed modest, the combination of cash inflow from financing and a leaner operating year left Virtus with meaningful liquidity on the balance sheet. The continued weakness in operating cash flow is something dividend investors should watch carefully as the company moves through 2026, even as earnings-based dividend coverage remains comfortable.

Analyst Ratings

Formal analyst coverage of VRTS has been limited in early 2026, and no current consensus price targets are available as of the February 23 update date. That relative silence from the Street is not unusual for a smaller-cap asset manager trading near multi-year lows—coverage tends to thin out precisely when price action is most discouraging.

Looking back at the most recent analyst activity, the directional lean from major firms has been cautious. Morgan Stanley’s Michael Cyprys had maintained a Sell rating into early 2025, and Barclays’ Benjamin Budish held a similarly cautious posture, both citing margin pressure and earnings trajectory concerns within the asset management space. At the same time, Piper Sandler’s Crispin Love held a Buy rating with a target well above current levels, reflecting confidence in Virtus’ long-term capital discipline and multi-boutique positioning.

With the stock now trading around $137—significantly below even the more conservative price targets that were in circulation a year ago—the valuation case has only grown more interesting from an income investor’s perspective. Whether the broader analyst community re-engages with fresh price target updates will be worth monitoring, particularly if quarterly earnings results show any stabilization in AUM trends or a rebound in operating cash flow generation.

Earning Report Summary

Virtus Investment Partners’ most recent reported results showed a business that continues to generate solid profitability even as the stock price has disconnected sharply from earnings power. Full-year revenue came in at approximately $852.9 million, with net income of $138.4 million and trailing EPS of $19.97. A profit margin of 16.23% and return on equity of 13.39% are respectable figures for an asset manager operating in a challenging environment for active strategies.

AUM and Flows

Asset flows remain one of the most closely watched metrics for any asset manager, and Virtus is no exception. The company has navigated a period of industry-wide pressure on active management, with some institutional redemptions weighing on total AUM in recent quarters. While detailed quarter-by-quarter AUM disclosures are pending with the next earnings release, the revenue base of $852.9 million reflects the scale of the fee-generating platform that remains in place underneath the stock’s recent price weakness.

Expense Trends and Margin Strength

Profitability metrics have held up reasonably well despite the pressures on the top line. A 16.23% profit margin reflects the company’s ability to manage its cost structure even as performance-based compensation fluctuates with market conditions. Return on equity of 13.39% is meaningful given that the stock now trades at just 1.01 times book value—suggesting that investors are acquiring that return stream at essentially no premium to net assets. Operating leverage within the multi-boutique model continues to support margins when revenue conditions are stable.

Channel Highlights

Virtus continues to operate across institutional, retail separate account, and open-end fund distribution channels. The institutional channel has historically been a source of both large inflows and, periodically, large redemptions when single clients rebalance. Retail and intermediary channels provide a more diversified and sticky revenue base. The company’s strategy of housing multiple investment boutiques under one umbrella gives it exposure to a wide range of asset classes and investor mandates, which supports revenue diversification even when specific strategies face headwinds. The next quarterly earnings release will provide updated AUM and flow data that income investors should review closely.

Management Team

At the helm of Virtus Investment Partners is George R. Aylward, who has led the company as President and Chief Executive Officer since its spin-off in 2008. With over two decades of experience in the asset management space, Aylward has played a key role in shaping Virtus’ strategy and guiding its evolution as an independent player in the investment world.

Supporting him is Michael A. Angerthal, Executive Vice President and Chief Financial Officer. He has been with Virtus since the beginning of its standalone journey and oversees the company’s financial direction, including risk oversight, budgeting, and shareholder communications. His background includes time at GE and Coopers & Lybrand, which adds breadth to the company’s financial stewardship.

Barry M. Mandinach leads the sales and marketing efforts as Executive Vice President and Head of Distribution. With decades of experience in asset management distribution, he has built out the firm’s reach across institutional and retail clients. Richard W. Smirl, Chief Operating Officer, handles the nuts and bolts of operations, including technology and product support. His past work at Russell Investments helps drive the operational side of the business.

Collectively, this leadership group brings stability, continuity, and depth. Their combined tenure and experience serve as a steadying force for the firm’s long-term vision, and the continued pattern of dividend increases under their stewardship reflects a management team that takes its commitment to shareholder returns seriously.

Valuation and Stock Performance

Virtus Investment Partners’ stock is now trading at one of its most compressed valuations in recent memory. At $137.01, the shares carry a P/E ratio of just 6.86—a level that would appear deeply discounted under most conventional valuation frameworks for a profitable financial services company. The price-to-book ratio of 1.01 means the stock is trading at almost precisely its book value of $136.03 per share, giving investors very little downside from an asset coverage standpoint even in a stress scenario.

Market cap has compressed to approximately $925 million despite the company generating $138.4 million in net income over the trailing twelve months. That implies a price-to-earnings multiple that many value-oriented investors would find striking—particularly when paired with a 6.33% dividend yield and a sub-50% payout ratio. The enterprise value picture adds additional texture given the company’s debt and cash position, but the equity valuation alone presents a case that is difficult to dismiss on a fundamentals basis.

The stock has underperformed the broader market significantly over the past twelve months, tracking from the high end of its $134.81–$215.06 range down to the low end. Beta of 1.44 means that in a market recovery, VRTS could snap back with above-average velocity—though that same beta works against it during risk-off episodes. For investors focused on income rather than price appreciation, the current entry point offers a 6.33% yield from a business whose EPS of $19.97 covers that dividend nearly twice over.

Risks and Considerations

Virtus doesn’t operate in a vacuum. Market conditions weigh heavily on its performance, and the asset management space is often at the mercy of macroeconomic trends. During periods of market drawdowns or low investor confidence, assets under management can shrink, impacting fee-based revenue. The recent compression in AUM has already shown how quickly that dynamic can affect the top line.

There’s also exposure to more concentrated strategies. Some portfolios are built around particular sectors or global regions, which makes them more vulnerable to economic or political shifts. If sentiment turns against those segments, it can accelerate outflows. The single institutional redemption that weighed on AUM in recent quarters is a reminder that large client concentrations carry their own specific risks.

The company also invests in high-yield, lower-rated securities in some strategies. These instruments offer attractive returns, but they come with increased default risk and more pronounced volatility. When liquidity dries up or credit spreads widen, these segments can take a meaningful hit. Derivative usage in some portfolios adds another layer of complexity—when used responsibly they can hedge risk, but in fast-moving markets they can amplify losses.

The weakness in operating cash flow that has persisted into recent periods deserves ongoing attention from dividend investors. While earnings-based dividend coverage remains comfortable at a 45.82% payout ratio, sustained divergence between net income and cash generation would eventually need to reconcile. Management’s ability to normalize operating cash flow is a key variable to watch in 2026.

Competitive pressure is constant. Larger players with more scale and distribution capabilities continue vying for market share, and the secular shift toward passive strategies creates a persistent headwind for active managers like Virtus. The regulatory backdrop remains a wild card as well—any meaningful changes in fee disclosure requirements, fiduciary standards, or product regulations could alter the operating environment. Virtus must continuously justify its strategies and performance to advisors and clients, and it does not have the brand scale of the largest firms in the space.

Final Thoughts

Virtus Investment Partners presents a genuinely interesting income opportunity as of February 2026. The combination of a 6.33% dividend yield, a payout ratio below 46%, and EPS of $19.97 that covers the $9.60 annual dividend nearly twice over is not a profile that appears often in the asset management space. The most recent dividend increase—from $2.25 to $2.40 per quarter in October 2025—shows a management team that continues to step up shareholder returns even as the stock price has moved sharply against them.

The valuation is the other side of the coin that income investors should not overlook. At 6.86 times earnings and 1.01 times book value, VRTS is priced at levels that imply very little confidence in the business’s earnings persistence. That skepticism may be warranted if AUM flows deteriorate further or if operating cash flow does not normalize. But for investors who believe the earnings base is sustainable, the margin of safety here is considerable.

Risks around market sensitivity, flow volatility, and operational cash flow trends are real and should be monitored carefully. The stock’s beta of 1.44 guarantees the ride will not be smooth. But for investors with a long time horizon and a preference for current income, Virtus offers a compelling yield from a fundamentally solvent business trading near its book value. That combination does not guarantee price appreciation in the short term, but it does provide meaningful income while waiting for sentiment to catch up with fundamentals.