Updated 2/23/26

VICI Properties isn’t your typical real estate investment trust. It has a unique story—spun off from Caesars Entertainment back in 2017, this REIT owns and operates some of the most iconic entertainment and gaming destinations in the country. We’re talking about well-known properties like Caesars Palace, the MGM Grand, and the Venetian in Las Vegas. But beyond the glitz, VICI’s real strength lies in the consistency of its income and its commitment to rewarding shareholders.

The bulk of VICI’s real estate is tied up in long-term triple-net leases. That structure means tenants are responsible for almost all property expenses, and VICI just collects rent—a setup that results in highly stable and predictable income. Add in the fact that many leases come with built-in annual rent increases, and you’ve got a reliable income engine that continues to grow.

Let’s dive into what’s been happening recently and how VICI stacks up from a dividend investor’s point of view.

Recent Events

VICI closed out its most recently reported fiscal year with continued top-line momentum. Revenues reached $3.97 billion, and the company posted $2.79 billion in net income—a meaningful improvement over prior periods that underscores the durability of VICI’s triple-net lease model. The profit margin of 70.18% is exceptional by almost any measure and reflects just how lean the operating structure remains when tenants shoulder property-level costs.

On the dividend front, VICI raised its quarterly payout from $0.433 to $0.45 per share beginning with the September 2025 payment—a roughly 3.9% increase that marks yet another consecutive annual raise since the company’s IPO. That brings the annualized dividend to $1.77 per share, and the yield at the current price of $30.11 sits at a compelling 5.81%. For income investors, a sub-$31 entry point with a yield near 6% on a business generating $2.46 billion in operating cash flow is a meaningful setup.

Institutional ownership remains extremely high, reflecting continued confidence in VICI’s business model among the largest pools of professional capital. The company’s low beta of 0.70 reinforces its reputation as a stable, income-oriented holding in diversified portfolios.

Key Dividend Metrics

📈 Forward Yield: 5.81%

💵 Annual Dividend (Forward): $1.77

🔁 5-Year Average Yield: 5.00%

🧮 Payout Ratio: 66.44%

📆 Dividend Growth (Last Hike): +3.9% (Q3 2025)

💰 Last Quarterly Payment: $0.45

📊 EPS: $2.63

Dividend Overview

With a current yield of 5.81%, VICI delivers exactly what income investors are looking for—a meaningful payout backed by one of the most dependable cash flow streams in the REIT universe. That yield sits comfortably above the company’s five-year average of roughly 5.00%, which at the current price of $30.11 suggests investors are getting above-average income for a business that hasn’t fundamentally deteriorated—quite the opposite, in fact.

The payout ratio of 66.44% is another green flag. It confirms VICI isn’t stretching itself to fund distributions, leaving meaningful room for reinvestment and future raises while still prioritizing shareholder returns. The triple-net lease structure keeps VICI’s own operating costs extremely low, which is why a 70% profit margin is sustainable rather than anomalous. Tenants handle taxes, insurance, and maintenance—VICI collects rent and manages its balance sheet.

Operating cash flow of $2.46 billion provides substantial coverage for the dividend at current payout levels, and the company’s low beta of 0.70 means the income stream is delivered with considerably less share price volatility than the broader equity market—a combination that income-focused investors should find attractive.

Dividend Growth and Safety

VICI’s dividend track record has been impressive since it went public, and that streak remains intact. The most recent raise, from $0.433 to $0.45 per quarter, represented a 3.9% increase and took effect with the September 2025 payment. While the pace of growth has moderated somewhat compared to the 6%-plus hikes seen in earlier years, the consistency of annual raises is what matters most for long-term income compounders. VICI has now raised its dividend every year since its IPO—something not every REIT can claim.

Looking at the recent dividend history, the pattern is clear and deliberate: $0.39 per quarter through mid-2023, stepping up to $0.415 in the back half of 2023 and holding through mid-2024, then moving to $0.433 for four quarters before the latest step to $0.45. This staircase pattern of steady, predictable increases is precisely the behavior dividend growth investors want to see.

Future growth prospects remain solid. Operating cash flow of $2.46 billion and free cash flow of $1.28 billion provide strong coverage for the current annualized dividend of $1.77 per share. The gap between free cash flow and dividend obligations leaves VICI with financial flexibility to pursue additional acquisitions, manage its debt load, and continue raising the payout. Return on equity of 10.36% and return on assets of 5.01% are respectable metrics for a capital-intensive REIT operating in a higher-rate environment.

VICI’s beta of 0.70 reinforces the low-volatility character of this income holding. The properties themselves—casinos, resorts, and entertainment destinations—tend to generate consistent foot traffic even during softer economic periods, and because the major gaming operators holding VICI’s leases have substantial financial resources, rent collections have remained reliable across varying macro backdrops. For investors evaluating dividend growth and safety together, VICI continues to check the right boxes.

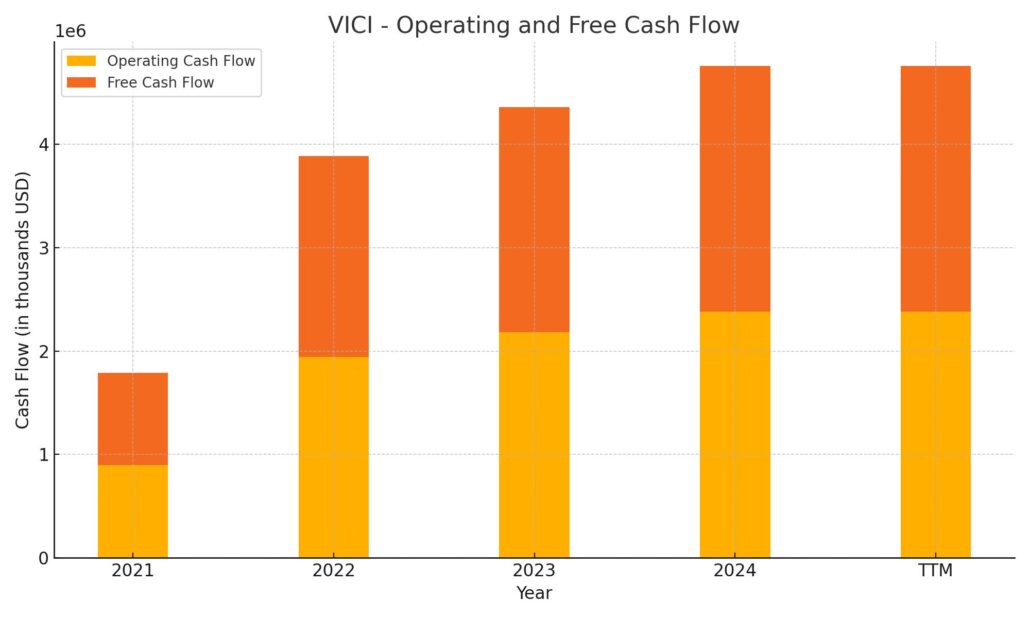

Cash Flow Statement

VICI’s cash flow statement reflects a company with one of the most capital-efficient business models in the REIT sector. Operating cash flow for the trailing period came in at $2.46 billion, a figure that confirms the strength and predictability of the underlying lease income. Free cash flow of $1.28 billion, while lower than the operating figure, reflects some investing activity and remains more than sufficient to fund dividends at current levels with room to spare. The divergence between operating and free cash flow is worth monitoring but is not alarming given the nature of VICI’s investment activity.

The triple-net lease model remains the engine behind VICI’s cash flow quality. Because tenants absorb virtually all property-level expenses, capital expenditure requirements on VICI’s side are minimal, which is why such a high proportion of revenue—70.18%—flows through to net income. Net income of $2.79 billion on revenue of $3.97 billion is an exceptional conversion rate that most REITs simply cannot replicate. With a profit margin at that level and operating cash flow comfortably above $2 billion, VICI’s dividend coverage remains among the most secure in the diversified REIT category. The balance sheet and cash generation together paint a picture of a business that is built to sustain and grow its payout through varying market conditions.

Analyst Ratings

Formal analyst consensus data is not available in the current data set, but VICI’s financial profile makes it straightforward to assess where the investment community is likely positioned. A stock trading at $30.11 with a P/E of 11.45, a 5.81% dividend yield above its five-year average, a 70% profit margin, and $2.46 billion in operating cash flow presents a profile that income-oriented analysts have historically viewed favorably. The current price sits in the lower half of the 52-week range of $27.48 to $34.03, suggesting the market has pulled back from more optimistic valuations seen earlier in the year.

VICI’s credit profile has improved meaningfully since its early years as a public company. The Moody’s upgrade to investment-grade status was a landmark event, and the company’s consistent rent collections, conservative balance sheet management, and disciplined acquisition strategy have maintained that standing. Analysts covering the gaming REIT space have generally maintained constructive views on VICI given these qualities, even as the broader REIT sector faces ongoing pressure from elevated interest rates.

The primary debate among analysts centers on the interest rate environment and its effect on REIT valuations generally, rather than on any company-specific deterioration. With VICI’s yield now at 5.81% and its fundamentals intact, any sustained movement toward lower rates would likely serve as a meaningful catalyst for price appreciation. Until that shift materializes, the income thesis stands on its own merits for investors willing to hold through the rate uncertainty.

Earnings Report Summary

Revenue Still Climbing

VICI’s most recently reported financials show continued top-line growth, with revenue reaching $3.97 billion. That represents meaningful progress from the $3.85 billion reported in 2023, and the trajectory reflects both the embedded rent escalators in VICI’s existing leases and the contribution of investments made in prior periods. The consistency of lease-based revenue is a defining feature of this business—there are no seasonality swings or volume-dependent fluctuations to navigate. Rent comes in, quarter after quarter, from some of the most recognized gaming and entertainment operators in the world.

Net Income and Margins Impress

Net income of $2.79 billion represents a strong result and translates to EPS of $2.63. The profit margin of 70.18% is a standout figure that reflects the structural advantages of triple-net leasing—when tenants cover property-level costs, a vastly higher share of revenue falls to the bottom line compared to traditional property ownership models. Return on equity of 10.36% and return on assets of 5.01% are solid figures for a capital-intensive REIT navigating a higher-rate environment, and they confirm that VICI is generating real returns on the asset base it has assembled through years of strategic acquisitions.

Cash Flow Supports the Dividend Narrative

For dividend investors, operating cash flow of $2.46 billion is the number that matters most, and it provides robust coverage for VICI’s annualized dividend obligation. Free cash flow of $1.28 billion, after accounting for investing activity, still leaves a comfortable buffer above the dividend. This level of cash generation supports not only the current $1.77 annualized payout but also the continued pattern of annual increases that VICI has maintained since going public. The alignment between cash flow growth and dividend growth is exactly what long-term income investors want to see sustained.

Balance Sheet and Capital Discipline

VICI’s book value per share of $25.89 and price-to-book ratio of 1.16 suggest the market is applying only a modest premium to the underlying asset value—a reasonable reflection of the current rate environment’s pressure on REIT valuations. The company’s low beta of 0.70 means shareholders have experienced considerably less volatility than the broad market, which is a meaningful quality-of-life factor for income investors who prioritize consistency. With the dividend recently raised to $0.45 per quarter and cash flow metrics remaining strong, the foundation heading into 2026 looks solid.

Management Team

At the helm of VICI Properties is a leadership team with deep roots in real estate and gaming. Edward Pitoniak serves as the Chief Executive Officer, bringing extensive experience from the hospitality and entertainment sectors. Prior to leading VICI, Pitoniak held significant roles in various real estate ventures, providing him with a solid foundation to guide the company through both growth phases and periods of macro uncertainty.

John Payne, the President and Chief Operating Officer, has over two decades of experience in the gaming and hospitality industry. His background includes leadership positions at major gaming corporations, where he was instrumental in operations and development. Payne’s expertise is pivotal in managing VICI’s extensive portfolio of gaming properties and maintaining the relationships with blue-chip tenants that underpin the company’s income reliability.

Overseeing the financial health of the company is Chief Financial Officer David Kieske. With more than 20 years in real estate finance, Kieske’s previous tenure at Wells Fargo Securities involved providing capital solutions to real estate entities. His financial acumen ensures VICI’s fiscal strategies support its growth objectives while maintaining the balance sheet discipline that earned the company its investment-grade credit rating.

The broader executive team comprises professionals with diverse backgrounds in law, finance, and operations, collectively steering VICI Properties toward its long-term strategic goals with a consistent emphasis on shareholder returns.

Valuation and Stock Performance

VICI is currently trading at $30.11, sitting in the lower portion of its 52-week range of $27.48 to $34.03. The pullback from the year’s high of $34.03 has pushed the yield above 5.8% and compressed the P/E ratio to 11.45—a level that looks undemanding for a business generating $2.79 billion in net income with a 70% profit margin and a track record of annual dividend increases.

The price-to-book ratio of 1.16, against a book value per share of $25.89, indicates the market is applying only a modest premium to VICI’s asset base. In prior rate environments, high-quality REITs with VICI’s tenant roster and income consistency commanded much higher multiples. The compression in valuation is largely a sector-wide phenomenon tied to interest rate sensitivity rather than company-specific deterioration, which means investors entering at current levels are getting a better price on the same underlying business.

With a market cap of approximately $32.2 billion and a beta of 0.70, VICI remains one of the larger and more stable REITs available to income investors. The combination of a sub-12x P/E, a yield meaningfully above the five-year average, and strong cash flow coverage of the dividend makes the current valuation look attractive for investors with a multi-year income horizon. A reversion toward the midpoint of the 52-week range alone would represent a roughly 5% price gain on top of the 5.81% yield—a reasonable total return scenario without requiring any heroic assumptions.

Risks and Considerations

While VICI Properties has a solid foundation, several risks deserve consideration. Tenant concentration remains the most prominent. A significant portion of VICI’s revenue flows from a limited number of gaming operators, meaning any financial instability among those tenants could directly affect rental income. The major operators have proven resilient, but the concentration risk is structural and doesn’t disappear with favorable conditions.

Interest rate sensitivity continues to weigh on the entire REIT sector, and VICI is not immune. Higher rates increase borrowing costs on any new debt issuance and apply pressure to valuation multiples as income investors compare REIT yields against risk-free alternatives. The current price of $30.11, down from the 52-week high of $34.03, reflects some of that ongoing pressure. Any sustained move higher in long-term rates could create additional headwinds for the share price even if the underlying business performs well.

Economic downturns introduce another layer of risk. VICI’s properties serve consumer discretionary spending, and while gaming destinations have historically shown resilience, a severe recession could pressure tenant profitability and, in an extreme scenario, lease terms. The triple-net structure provides VICI with significant contractual protection, but it is not a guarantee against tenant stress over long time horizons.

VICI’s expansion into non-gaming experiential properties introduces both diversification benefits and exposure to new market dynamics and regulatory environments. While the diversification is strategically sensible, execution in unfamiliar segments carries its own risks. Finally, the company’s short track record as a public entity—less than a decade—means its dividend growth history, while encouraging, has not been tested through a full economic cycle. Investors should weigh that context when evaluating the long-term sustainability of future payout increases.

Final Thoughts

VICI Properties continues to stand out in the REIT landscape through its combination of iconic assets, triple-net lease discipline, and a dividend growth record that has remained unbroken since its IPO. The most recent raise to $0.45 per quarter extends that streak and brings the annualized payout to $1.77—a figure now yielding 5.81% at the current price of $30.11, above the company’s five-year average yield and backed by $2.46 billion in operating cash flow.

The valuation setup at current levels is more compelling than it has been in some time. A P/E of 11.45, a price-to-book of 1.16, and a yield approaching 6% on a business with a 70% profit margin and low beta don’t often arrive together. The primary overhang—interest rate pressure on REIT multiples broadly—is real, but it is a sector-level dynamic rather than a VICI-specific problem. The underlying business continues to perform.

For income investors seeking a durable, growing dividend from a business with hard assets, blue-chip tenants, and a management team that has demonstrated consistent capital discipline, VICI at current levels presents a strong case. As always, aligning any investment with individual financial goals and risk tolerance is essential, but the income thesis here remains among the more compelling in the REIT universe.