Updated April 2025

Rooted in the backbone of U.S. telecom, Verizon’s strength comes from its scale, its network, and its ability to keep cash coming in year after year. This isn’t a company chasing trends. It focuses on consistency. That stability has allowed Verizon to be a reliable dividend payer for decades, even through market downturns and rising interest rates. For those building income-focused portfolios, it deserves a serious look.

📌 Key Dividend Metrics

📅 Next Dividend Date: Ex-dividend on April 10, 2025

💵 Forward Annual Dividend: $2.71 per share

📈 Forward Yield: 6.06%

📊 5-Year Average Yield: 5.70%

🔁 Payout Ratio: 64.86%

📆 Next Payment: May 1, 2025

📉 Trailing Annual Yield: 5.92%

Recent Events

Verizon’s stock has been quietly gaining back ground over the past year. It hit a low near $37 and has since bounced back to the mid-$40 range, closing at $44.74 most recently. While the broader market has had its ups and downs, Verizon’s recovery has been slow, steady, and driven by fundamentals—not hype.

Most notable lately is the improvement in free cash flow. Over the past 12 months, Verizon brought in nearly $37 billion in operating cash flow and had over $16 billion left in free cash flow after capital expenditures. That kind of financial breathing room is exactly what you want to see if you’re counting on a dividend to stick around.

Revenue hasn’t been flashy—up just 1.6% year over year—but that’s not unusual for a company of Verizon’s size. More importantly, profit margins are holding strong. The latest figures show a profit margin just shy of 13% and an operating margin north of 21%, which in a capital-heavy industry like telecom, is a real sign of strength.

The company still carries a big debt load, over $170 billion, but the market doesn’t seem too worried. The valuation is still reasonable, and with a beta of 0.40, Verizon isn’t bouncing around with every market tremor. It’s steady. And that’s just the kind of temperament income investors often prefer.

Dividend Overview

Verizon’s 6.06% forward dividend yield sets it apart in today’s market. In a world where many companies struggle to even maintain a payout, Verizon’s ability to offer such a high yield without extreme risk makes it a standout.

It’s not just the size of the dividend that’s appealing—it’s the track record behind it. The payout ratio of about 65% tells you that the dividend is being paid from a strong base. There’s still flexibility left for investment, debt reduction, or even modest increases over time.

Speaking of increases, Verizon has raised its dividend annually for 17 straight years. The bumps have been modest, typically around 2% to 3%, but the key here is consistency. No skipped years, no freezes. Just a quiet, steady upward march. And that kind of reliability, especially when yields are this high, adds real value for long-term income investors.

Dividend Growth and Safety

When evaluating the safety of Verizon’s dividend, three factors rise to the top: strong cash flow, a manageable payout ratio, and the reliability of its core business.

The cash flow picture is solid. Nearly $37 billion in operating cash flow provides a thick cushion. After paying for capital investments, there’s still enough free cash flow to cover the dividend more than once over. That’s the kind of buffer that helps a dividend survive economic bumps in the road.

The payout ratio near 65% strikes a good balance. It rewards shareholders without putting pressure on the balance sheet. It also gives Verizon some flexibility. If costs rise or revenues dip, the company isn’t painted into a corner.

Yes, Verizon has a large amount of debt, but that’s expected in telecom. This industry is built around heavy infrastructure, which demands capital. But it also delivers recurring revenue—monthly bills from millions of customers that keep rolling in, month after month. That predictability helps the company manage its debt without compromising shareholder returns.

Verizon’s low beta also speaks volumes about its nature as a dividend stock. A beta of 0.40 means it’s less volatile than the overall market. So, while the yield is high, you’re not signing up for a rollercoaster ride.

In the end, Verizon doesn’t need to dazzle. It just needs to deliver. And for dividend investors, that’s exactly what it’s been doing—quietly, consistently, and with a check in the mailbox every quarter.

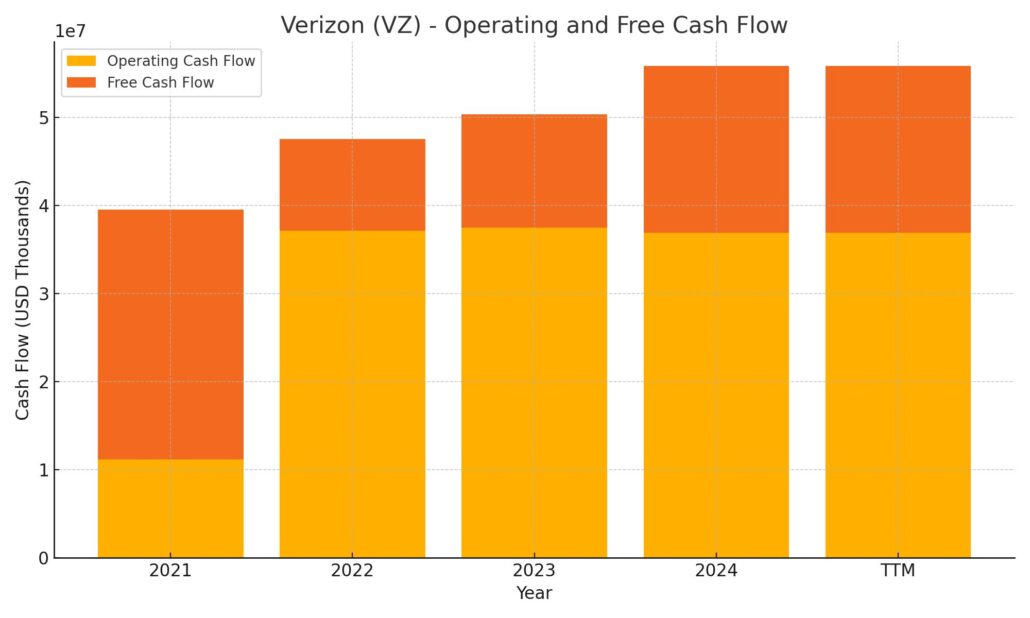

Cash Flow Statement

Verizon’s cash flow performance over the trailing twelve months highlights a business built around dependable, recurring income. The company brought in $36.9 billion in operating cash flow, matching its output from the prior year and showcasing remarkable consistency. Despite slightly lower revenues, Verizon maintained solid operational efficiency, which kept its cash generation strong. This level of cash flow is more than sufficient to fund its dividend obligations, which currently run just under $11.4 billion annually.

Capital expenditures for the TTM came in at just under $18 billion, showing a disciplined pullback from previous years where spending reached well over $24 billion. As a result, free cash flow rose sharply to $18.9 billion, a notable increase from $12.9 billion in the previous year and nearly double the amount from two years ago. Financing activities, including net debt repayments, led to a cash outflow of $17.1 billion. Still, the company ended the period with $4.6 billion in cash—an increase from last year’s $3.5 billion. The improving free cash flow trend and restrained capital spending both underscore Verizon’s financial maturity and its ability to comfortably support shareholder returns without compromising its liquidity.

Analyst Ratings

📈 In recent weeks, Verizon Communications (VZ) has seen a mix of analyst actions reflecting varying perspectives on the company’s outlook. On April 1, one firm raised its price target from $48 to $50, maintaining an outperform rating. This move shows confidence in Verizon’s ability to sustain profitability and execute well in a competitive environment. On the flip side, earlier in March, another analyst firm took a more cautious approach and downgraded the stock from outperform to peer perform, signaling a neutral stance on near-term potential.

💬 The average price target from analysts currently sits around $46.69, with projections spanning from a low of $40 to a high of $55. This consensus implies a modest upside from the latest trading levels near $44.74, suggesting a fair valuation range in the eyes of the market.

📉 The recent downgrade came amid concerns about intensifying competition in the wireless space, which could pressure subscriber growth and margins. That said, the upgrade and raised target reflect growing optimism in Verizon’s cost control measures and its ability to generate strong cash flow. The contrast in views illustrates how some analysts are zeroing in on short-term challenges, while others are leaning into the company’s longer-term stability and dividend strength.

Earning Report Summary

Verizon wrapped up its fourth quarter with a performance that felt steady and focused, signaling that the telecom giant is leaning into its core strengths while navigating a highly competitive landscape. The numbers weren’t jaw-dropping, but they told a story of stability and solid execution.

Solid Earnings Rebound

Earnings per share came in at $1.18, which marks a nice rebound from the loss the company posted during the same period a year ago. If you strip out the one-time items and look at the adjusted EPS, it was $1.10—just a touch higher than last year’s $1.08. It’s not a dramatic leap, but it’s progress, and in this kind of business, slow and steady often wins. Revenue hit $35.7 billion for the quarter, up just over 1.5% from the year before. Again, nothing flashy, but it’s a move in the right direction.

Wireless Growth Driving Momentum

Wireless continues to be the engine that powers Verizon. The company added 568,000 postpaid phone subscribers—its best quarterly performance in five years. That’s a big deal in a market where grabbing new customers isn’t easy. Wireless service revenue climbed 3.1% year-over-year, landing at $20 billion. Pricing changes, upsells on additional services, and growth in fixed wireless access helped move that number higher. Broadband also had a good showing, with 408,000 new additions, most of which came from fixed wireless. That piece of the business now serves nearly 4.6 million customers.

Better Bottom Line and Healthy Cash Flow

The bottom line looked a lot healthier this time around. Verizon posted $5.1 billion in net income for the quarter, a sharp turnaround from the $2.6 billion loss a year ago. Free cash flow for the full year came in at $19.8 billion—an improvement over last year’s $18.7 billion. They kept capital spending in check too, investing about $17.1 billion into the network and tech upgrades.

Looking Ahead

Verizon’s forecast for 2025 suggests more of this measured growth. They’re calling for wireless service revenue to rise somewhere between 2% and 2.8%, and adjusted EPS is expected to grow up to 3%. Capital expenditures are projected to be in the $17.5 to $18.5 billion range, which shows the company is still investing, but not overextending. It’s a cautious but confident outlook—and for a company that thrives on consistency, that’s exactly what shareholders likely want to see.

Chart Analysis

Trend and Moving Averages

The chart shows a clear upward shift in price behavior over the last several months. After dipping toward the $36–$37 range in early summer, the stock began a steady climb, moving past both the 50-day and 200-day moving averages. For a good part of the fall and early winter, the price hovered above the 50-day average, suggesting a healthy bounce from the earlier lows.

Around the start of the year, there was a brief dip that tested the 200-day moving average, which held up well as support. Since then, the stock has climbed again, and the 50-day average has recently crossed above the 200-day—a bullish signal known as a golden cross. This crossover tends to mark a shift in momentum and suggests the recent trend may have legs.

Volume Behavior

Trading volume has been relatively stable, with a few spikes during key price movements. Notably, volume picked up during the early January rally and again in March, showing increased participation during upward moves. There hasn’t been much volume during sell-offs, which implies that any downward pressure has been relatively soft and lacking conviction.

RSI Momentum

The RSI has mostly floated in neutral-to-bullish territory. It occasionally pushed above 70, suggesting short-term overbought conditions, but didn’t linger there too long. Lately, the RSI dipped and rebounded again, showing that the recent consolidation may be setting up for another leg higher. The index hasn’t dipped much below 30 during this period, indicating persistent demand and the absence of panic selling.

Overall Price Structure

The overall structure of the chart points to a slow and steady recovery. While there have been periods of consolidation and short-term pullbacks, the price action consistently finds support at higher levels, forming a classic uptrend. The recent price bounce off the 200-day moving average, along with the rising slope of the moving averages, further reinforces the idea that the longer-term trend is improving.

The past year on this chart tells a story of gradual rebuilding in confidence and steady momentum, with fewer signs of volatility as time has passed. It reflects a market that’s warming up to the stock again—quietly, but firmly.

Management Team

Verizon’s leadership is shaped by a team of experienced executives guiding the company through a fast-changing communications environment. Hans Vestberg leads the group as Chairman and Chief Executive Officer. Before joining Verizon, he served as CEO of Ericsson, and his background in global network strategy has helped push Verizon’s 5G expansion forward. Since stepping into the CEO role in 2018 and Chairman in 2019, he’s kept the company focused on connectivity innovation and operational discipline.

Supporting him is Sowmyanarayan Sampath, Executive Vice President and CEO of the Consumer Group. He’s responsible for delivering wireless and broadband services to millions of retail customers across the U.S. His role centers on subscriber growth, pricing strategies, and improving customer experiences.

Kyle Malady serves as Executive Vice President and CEO of the Business Group, overseeing services for commercial, enterprise, and government clients. With deep roots in technical operations, Malady brings a performance-driven approach to building and maintaining reliable, large-scale infrastructure for business-critical services.

Other key leaders include Shankar Arumugavelu, who oversees global operations, and Leslie Berland, who heads up marketing. Together, this executive group spans network operations, customer experience, marketing, strategy, and finance. The organizational structure splits operations into two customer-centric divisions—consumer and business—supported by centralized teams handling legal, HR, technology, and finance. This format allows Verizon to remain agile, efficient, and focused on core strengths across both customer and commercial segments.

Valuation and Stock Performance

As of early April 2025, Verizon’s stock was trading at $44.74. That’s a modest dip on the day but part of a stronger upward trend since the start of the year. Year-to-date, the stock has gained around 12%, quietly outperforming expectations and showing strength in a market that’s been anything but predictable.

From a valuation standpoint, Verizon’s stock still appears attractively priced. Forward earnings multiples remain below sector averages, suggesting that the market hasn’t fully priced in the company’s earnings stability or its consistent free cash flow. Earnings are expected to grow modestly over the next few years, which may not attract momentum traders but is perfectly suitable for investors who value predictable returns.

The company’s dividend yield continues to stand out, hovering above 6%. That payout is backed by strong operating cash flow and a conservative payout ratio, reinforcing confidence that the dividend is not only secure but has room to grow incrementally. While the overall valuation may not scream bargain, the combination of yield, cash flow, and low volatility makes the current price level look more than reasonable.

Risks and Considerations

Even with its many strengths, Verizon carries a few risks that are worth considering. One of the most persistent concerns is the company’s debt. With a capital-intensive business model, Verizon has taken on substantial long-term debt over the years to invest in its network infrastructure. While that’s par for the course in telecom, it does mean the company must remain diligent about refinancing, managing interest costs, and balancing capital allocation.

Competitive pressure is another challenge. The wireless market is cutthroat, with rivals aggressively targeting market share through pricing and promotional tactics. Verizon’s leadership in premium service and network quality gives it a solid foundation, but the company must continue innovating to hold its ground.

Technology is evolving rapidly. Consumer expectations shift quickly, and new platforms and tools are changing how people connect. Verizon needs to stay nimble, investing in emerging tech while ensuring that its current offerings stay ahead of customer needs.

Regulatory risks also loom large. The telecommunications sector is heavily regulated, and changes in government policy or enforcement can have a material impact on pricing, privacy, and infrastructure investment. Verizon has a good track record navigating this terrain, but it’s a risk that never fully disappears.

Despite these headwinds, Verizon’s overall risk profile is relatively low. The consistency in its operations, the strength of its balance sheet, and its focus on cost control all contribute to a stable financial outlook.

Final Thoughts

Verizon is the kind of company that delivers on what it promises. It doesn’t chase trends or make headlines with dramatic moves, but it does the fundamentals well—generating strong cash flow, keeping margins steady, and returning capital to shareholders through dividends. The leadership team is experienced and forward-thinking, with a clear structure in place to guide both consumer and business segments through ongoing market changes.

Valuation-wise, the stock looks fairly priced given the strength of its balance sheet and the predictability of its cash flow. While it may not offer explosive growth, it brings a level of stability that’s become increasingly valuable in a volatile market.

The risks—debt, competition, technology shifts, and regulation—are all manageable with the right strategic focus. Verizon has shown time and again that it can navigate these challenges and still deliver consistent returns.

For those seeking reliable income and a business that performs steadily through cycles, Verizon continues to offer a solid foundation. Its performance in 2025 so far shows a company that’s not just holding steady but gradually building momentum in the right direction.