Updated April 2025

Verisk Analytics has built itself into a quiet but commanding force in the analytics space. What started as a data provider for the insurance industry has evolved into a high-margin, analytics-driven enterprise that plays a critical role in the global insurance ecosystem. It’s not typically the first name that pops into the heads of dividend investors, but that might be exactly why it’s worth a closer look. With a combination of steady performance, reliable cash flow, and an increasingly shareholder-friendly approach, Verisk offers a lot more than meets the eye.

Recent Events

Over the past year, Verisk has been on a solid run. The stock is up over 32% in the last 12 months, outpacing many large-cap peers and well ahead of the broader market. That kind of growth doesn’t usually come from companies considered “dividend stocks,” but Verisk has always played by a different set of rules.

In the latest quarter, earnings climbed nearly 21% year over year, while revenue rose by a healthy 8.6%. Those are strong numbers for a firm of this size, and they come from a company that’s been steadily refining its focus. After divesting several non-core segments, Verisk is now streamlined, focused almost entirely on its core insurance analytics business—and the numbers show it’s working.

With a net profit margin over 33% and return on equity north of 400%, Verisk isn’t just doing well; it’s executing at a high level. It’s also generating consistent free cash flow, bringing in over $700 million in levered free cash over the past twelve months. That’s key for dividend-focused investors. It means the company not only earns good money but keeps plenty of it to return to shareholders.

That discipline is paying off. Verisk bumped up its dividend once again this year, underscoring management’s confidence in the business and its long-term cash flow profile.

Key Dividend Metrics 📊

💰 Forward Annual Dividend Rate: $1.80

📈 Forward Dividend Yield: 0.60%

🔁 5-Year Average Dividend Yield: 0.59%

📅 Dividend Growth Streak: Over 10 years

📤 Payout Ratio: 23.42%

🔒 Dividend Safety: Strong

🚨 Most Recent Dividend Date: March 31, 2025

⚠️ Ex-Dividend Date: March 14, 2025

Dividend Overview

Verisk isn’t a high-yield name. At just 0.60%, the current dividend yield won’t grab headlines—but the strength of the payout is in its foundation. For starters, the company’s payout ratio is comfortably low at just over 23%. That’s a lot of room for growth, even if earnings were to take a short-term dip.

The more you dig into Verisk’s financial model, the more sense it makes for long-term dividend investors. The company’s operating structure is asset-light and cash-generative. That means less need for large capital investments, more steady cash flow, and more flexibility to return capital to shareholders when it makes sense.

Even with a modest yield, the reliability of Verisk’s dividend adds value. The consistency of the payout, combined with regular increases, creates a solid backbone for income-focused investors who don’t mind a little patience. It’s also worth noting that the company continues to buy back shares—another way management is returning value.

Dividend Growth and Safety

Dividend safety is often overlooked in favor of yield, but in Verisk’s case, it’s the standout feature. With $1.14 billion in operating cash flow and over $700 million in free cash flow last year, the company’s dividend payments are backed by a strong and stable foundation. Based on the $1.80 annual dividend and roughly 140 million shares outstanding, the total dividend payout lands around $252 million—a fraction of total free cash flow.

That kind of margin gives Verisk plenty of room to keep raising its dividend without putting stress on the balance sheet. And that’s exactly what the company has been doing. Over the past five years, the dividend has grown at a double-digit pace. No fireworks, just steady, dependable increases that keep stacking up year after year.

The debt picture might raise eyebrows—total debt stands at $3.25 billion, and the debt-to-equity ratio is eye-popping due to the company’s low equity base. But context matters. Verisk doesn’t operate like a traditional industrial or manufacturing company. It runs lean and earns consistently, with minimal need for heavy reinvestment. With an EBITDA north of $1.3 billion, it covers its obligations comfortably.

Another point that works in Verisk’s favor: its low beta. At 0.88, the stock is less volatile than the overall market. That makes it an appealing anchor for a portfolio seeking both income and stability. Institutional investors seem to agree—over 96% of the float is held by institutions, and that usually signals long-term trust in management and the financial strategy.

Verisk might not be the most obvious pick for a dividend-focused portfolio, but it’s quietly become one of the most consistent. It doesn’t make noise with a big yield, but its payouts are backed by strong fundamentals, clean financials, and management that knows how to execute. If you’re looking for steady, low-drama dividend growth, Verisk makes a solid case.

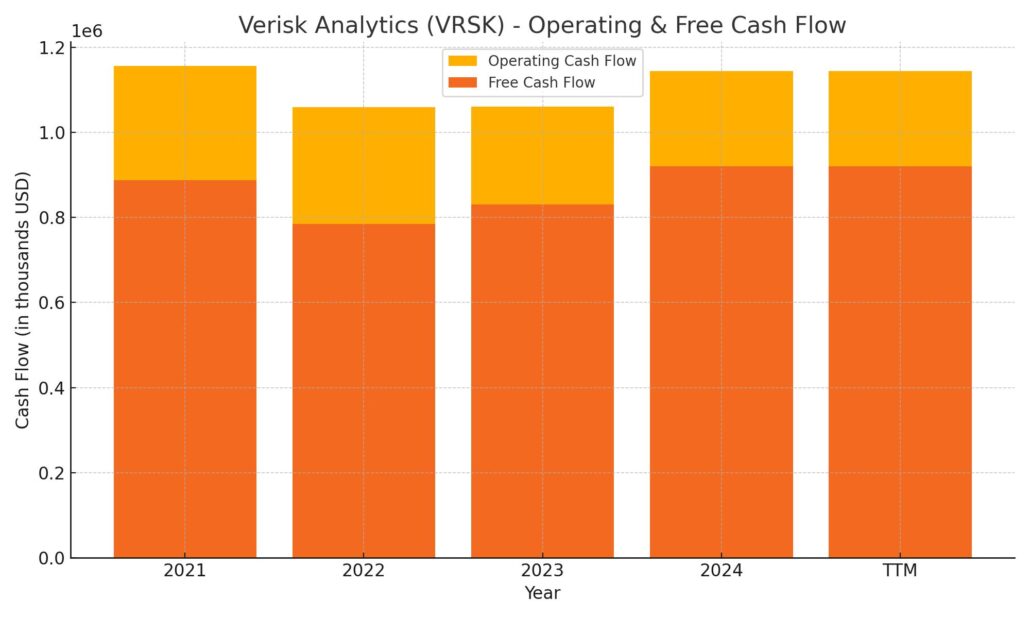

Cash Flow Statement

Verisk’s trailing 12-month cash flow profile reflects consistent operational strength. Operating cash flow came in at $1.14 billion, a slight uptick from the previous year and in line with its historical trend. Free cash flow stood at $920 million, showing solid efficiency despite elevated capital expenditures near $224 million. These figures confirm the company’s ability to generate reliable cash from core operations, which supports both dividends and share repurchases without financial strain.

On the financing side, Verisk returned over $1 billion to shareholders through stock buybacks while managing a balanced debt strategy—issuing $590 million in new debt and repaying $396 million. Investing cash flow was modestly negative at $125 million, with no major acquisitions impacting the period, a sharp contrast to the large inflow seen in 2023 from asset sales. Despite sizable shareholder returns and steady reinvestment, Verisk maintained a stable cash position around $291 million, consistent with prior years.

Analyst Ratings

🔄 In January 2025, Barclays shifted its outlook on Verisk Analytics, moving the stock from an “Overweight” to an “Equal Weight” rating with a revised price target of $310. 📉 This adjustment came after a strong run-up in the stock’s price, which pushed it closer to what the firm sees as its fair value. In short, the upgrade cycle has cooled as the valuation began to reflect much of the near-term upside.

🎯 As of early April 2025, the average analyst price target for Verisk sits at $305.47. Targets range from a more cautious $280 to a bullish $332, with 21 analysts weighing in. The consensus suggests a generally optimistic stance, though the recent rally has tempered expectations for significant near-term gains.

📊 Many analysts continue to point out Verisk’s strength in subscription-based revenue, which has grown steadily thanks to solid product adoption and smart bundling strategies. The company’s move toward value-based pricing is also seen as a plus, improving its ability to command stronger margins while making revenues more predictable. Still, after such a strong run, valuation is starting to become a headwind for further upgrades.

Earning Report Summary

Solid Revenue Momentum

Verisk wrapped up the fourth quarter of 2024 with solid numbers that showed steady demand and strong execution. Revenue came in at $736 million for the quarter, up 8.6% from the same time last year. A big part of that growth came from their subscription services, which climbed 11% year-over-year. It’s clear their strategy of leaning into recurring revenue is working. More clients are locking into long-term services instead of just one-off transactions, which brings a lot more stability to the business.

What’s also encouraging is that this growth wasn’t dependent on flashy deals or short-term boosts. It was broad-based, with both underwriting and claims solutions performing well. That speaks to the strength of their core business and the value clients are seeing in their data and analytics offerings.

Margins and Profitability

On the profit side, Verisk delivered $398 million in adjusted EBITDA, up nearly 10% from the previous year. Margins improved too, ticking up to 54.1%. That kind of expansion doesn’t happen by accident—it reflects good discipline on expenses and an ongoing shift toward more profitable offerings.

The company has clearly been focused on keeping operations lean while still investing in growth areas. That balance is showing up in their bottom line, and it’s something investors like to see.

Verisk isn’t just growing its business—it’s also making sure shareholders benefit directly. During the quarter, they returned $55 million through dividends. On top of that, they completed a $300 million accelerated share repurchase program in January. That’s a sizable move and a strong signal that management sees value in the stock and is serious about rewarding investors.

Looking Ahead

Management laid out guidance for 2025, and it’s optimistic. They’re projecting revenue between $3.03 billion and $3.08 billion, with adjusted EBITDA in the $1.67 to $1.72 billion range. Expected earnings per share are forecasted to land somewhere between $6.80 and $7.10.

That outlook suggests confidence in where the business is headed. With solid momentum, growing margins, and a clear commitment to shareholder returns, Verisk is heading into the new year with a strong foundation and steady footing.

Chart Analysis

Price Trend and Moving Averages

Over the past year, the price action has shown a steady upward trajectory. After a brief dip early in the chart, the stock found its footing around May and began a strong rally that continued through the summer. The 50-day moving average (red line) crossed above the 200-day moving average (blue line) around mid-year—a classic bullish signal—and has remained above it since. This kind of setup suggests the longer-term trend is firmly intact, with buyers consistently stepping in on pullbacks.

What’s also worth noting is how the stock has respected both moving averages throughout the chart. During the few periods where price dipped close to the 50-day line, it quickly rebounded, signaling strong underlying support. The 200-day moving average continues to rise steadily, adding confidence to the idea that this isn’t a short-term blip but part of a more durable trend.

Volume Behavior

Volume has stayed relatively balanced, with occasional spikes during stronger moves, especially during rallies. These higher-volume days on upward price movements are encouraging, as they show participation from larger players rather than just low-volume drift. There hasn’t been a major increase in selling volume, even during pullbacks, which helps paint a picture of calm accumulation rather than distribution.

RSI and Momentum

The RSI (Relative Strength Index) has generally stayed within a healthy range. There were a few moments of overbought conditions, particularly during the late fall and again recently, but it hasn’t stayed extended for long. Each time the RSI cooled off, the price held up fairly well, which suggests the pullbacks were more about digestion than weakness.

Currently, the RSI is approaching overbought territory again. While that might mean the stock is due for a pause, the broader trend and price structure remain supportive. The RSI also spent a significant amount of time this year above the midpoint of 50, which typically favors the continuation of upward momentum.

Overall Structure

The chart shows a clear pattern of higher highs and higher lows, supported by strong technical trends and steady volume. Momentum remains on the side of buyers, and the long-term structure looks intact. If the trend continues, the recent breakout above resistance levels could evolve into a new leg higher, especially if volume stays constructive and price action remains orderly.

Management Team

Leadership Overview

At the helm of Verisk Analytics is Lee M. Shavel, who has served as Chief Executive Officer, President, and Director since 2023. Before stepping into the CEO role, Shavel was the company’s Chief Financial Officer and President, and prior to joining Verisk, held senior leadership positions at Nasdaq and Merrill Lynch. His background in both finance and strategy has shaped his approach to leading Verisk through its transformation into a more focused, high-margin data analytics company.

Supporting Shavel is a seasoned executive team that includes Elizabeth D. Mann as Chief Financial Officer and Executive Vice President, and Nicholas Daffan as Chief Information Officer and Executive Vice President. Together, this leadership group is tasked with pushing the company forward in a highly competitive landscape, while maintaining operational discipline and a commitment to consistent shareholder returns.

Valuation and Stock Performance

Current Market Position

As of late March 2025, Verisk’s stock was trading just below $295, giving the company a market cap of around $41 billion. The stock has performed well over the past year, easily outpacing broader indexes and sector averages. This momentum reflects both operational consistency and investor confidence in the company’s streamlined business model following its exit from non-core operations.

Analyst Perspectives

Across the analyst community, sentiment remains positive but slightly cautious. The average 12-month price target sits around $299, with estimates ranging from $279 on the low end to $321 on the high end. That tight range suggests most analysts see the stock as fairly valued at current levels, at least in the near term. After a strong run, the risk-reward profile appears balanced, and further upside will likely depend on continued earnings outperformance or new growth catalysts.

Financial Outlook

Looking to the year ahead, Verisk has guided for revenues between $3.03 billion and $3.08 billion, targeting 6% to 8% organic constant currency growth. While growth remains healthy, the company is also preparing for higher interest expenses in 2025, with projections ranging from $145 million to $165 million. This is a step up from just over $124 million in 2024 and could weigh on net income if not offset by operating gains. The guidance reflects confidence in the company’s core operations, even as it navigates a slightly more expensive financial environment.

Risks and Considerations

Market and Competitive Risks

Verisk operates in a competitive and fast-evolving industry. Data and analytics firms are popping up rapidly, while larger players continue to expand their capabilities. Maintaining a competitive edge requires constant innovation and reinvestment. If Verisk slows its product development or underestimates shifts in client demand, there’s a real risk of losing market share.

Regulatory and Legal Risks

Data privacy regulations are also becoming more complex across global markets. Since Verisk handles sensitive insurance-related data, staying compliant isn’t optional—it’s mission-critical. Regulatory changes or missteps could lead to fines, restrictions, or reputational damage. Ongoing legal proceedings, while not unusual for a firm of its size, add another layer of potential financial exposure.

Financial Risks

With rising interest rates, Verisk is entering a period where its cost of debt will take a larger bite out of earnings. The company has done well managing leverage, but increased financing costs could eventually impact its ability to aggressively repurchase shares or raise dividends at the same pace. Investors will want to watch how management balances debt servicing with capital return strategies.

Emerging Technological Risks

Verisk is also pushing further into AI-powered tools, which brings both opportunity and complexity. While AI can increase efficiency and open up new markets, it also creates exposure to flawed data models, biases, and security vulnerabilities. Trust and reliability are central to Verisk’s brand, so how the company handles AI risk management will matter a lot in the long run.

Final Thoughts

Verisk is a company with a clear direction, strong leadership, and a track record of delivering results. After sharpening its focus on insurance analytics, it has become more efficient, more predictable, and more disciplined. The recent price performance reflects that transformation, though it also raises the bar for what’s next.

With manageable risks and a solid foundation, Verisk seems well-positioned to keep delivering on its long-term vision. Continued execution, especially in maintaining strong free cash flow and expanding margins, will likely be the key to keeping investors on board through whatever challenges lie ahead.