Updated April 2025

Headquartered in Chattanooga, Tennessee, Unum has carved out its space in the insurance world by focusing on workplace benefits—think disability, life, and supplemental health coverage. It’s not flashy, but it’s a backbone service for employers and employees alike.

The company traces its roots back to the 1800s and has long since settled into a rhythm of reliability. In a market that often favors hype over substance, Unum delivers something refreshingly steady: disciplined underwriting, solid returns, and dependable dividends. And that combination is hard to ignore when you’re investing for income and long-term peace of mind.

Recent Events

It’s been a strong run for Unum. The stock recently closed at $82.91, a notable climb from its 52-week low of $48.38. That’s a surge of more than 55% over the past year—well ahead of the broader market. This isn’t the result of some wild swing or speculative frenzy, either. It’s built on earnings strength and growing investor confidence.

In its most recent quarter, Unum posted a 5.5% year-over-year increase in earnings and a 2.9% rise in revenue. That added up to $1.78 billion in net income over the last 12 months, or $9.46 in earnings per share. And with a forward P/E ratio still under 10, the stock looks reasonably valued, especially for a company showing this kind of bottom-line growth.

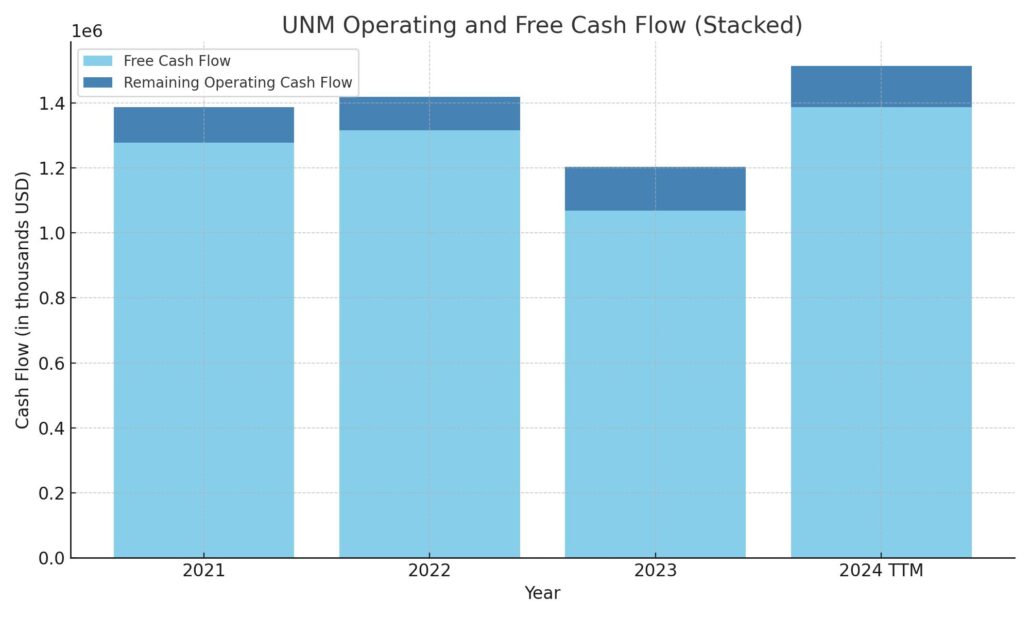

Cash flow is another piece of the story. Unum pulled in $1.51 billion in operating cash flow and $1.44 billion in free cash flow. That’s a solid financial cushion, especially considering its debt sits at just over $4 billion. It’s got $2.7 billion in cash, which helps keep the balance sheet healthy and flexible.

Key Dividend Metrics

📅 Dividend Yield (Forward): 2.03%

💰 Annual Dividend Rate: $1.68

🧮 Payout Ratio: 16.6%

📈 5-Year Average Yield: 3.76%

🚀 1-Year Dividend Growth: 3.70%

🛡️ Dividend Safety: Well-supported by free cash flow

📊 Ex-Dividend Date: January 24, 2025

💵 Last Dividend Paid: February 14, 2025

Dividend Overview

Unum’s dividend isn’t going to top any yield charts, but that’s not the point. What matters here is reliability and long-term sustainability—and on that front, it delivers. The forward yield of 2.03% may seem modest at first glance, especially when compared to its five-year average of 3.76%, but the context matters: the stock price has appreciated quickly, pulling the yield down even as the company keeps raising the payout.

What stands out is the low payout ratio. At just 16.6% of earnings, Unum is keeping plenty of profit in reserve. That means more flexibility to reinvest in the business, buy back shares, or keep increasing dividends—without putting financial pressure on the company.

Unum’s dividend record is also worth noting. It’s been paying uninterrupted dividends for decades, and in a world where dividend cuts aren’t uncommon, that kind of consistency is a rare find. It’s not a dividend aristocrat, but it has the kind of quiet track record that income investors love.

Dividend Growth and Safety

When you look at dividend growth, Unum doesn’t jump out with big, flashy increases. Instead, it’s taken a steady, measured approach—raising the dividend at a compound annual rate of about 5% over the past five years. The most recent bump was around 3.7%, and with so much room left in the payout ratio, there’s clearly space to continue that trend.

The real story is safety. The company’s free cash flow of $1.44 billion easily covers the roughly $296 million it spends annually on dividends. That leaves a big margin of safety, especially during economic slowdowns or if unexpected costs crop up. This isn’t a dividend being funded by debt or aggressive financial engineering—it’s backed by earnings and cash.

The debt situation is also well under control. With a debt-to-equity ratio of just 37%, and $2.7 billion in cash on hand, Unum isn’t anywhere close to stretched. That financial stability adds another layer of comfort for long-term investors who are counting on their dividends showing up every quarter.

Institutional investors clearly see the appeal, with over 90% of the float held by large firms. Short interest is low too, sitting at just over 2% of float. These kinds of stats don’t drive headlines, but they do point to a market that sees this stock as stable and dependable.

Unum isn’t aiming to be the most exciting name in your portfolio. What it offers is a steady hand, a dependable income stream, and a track record that’s hard to argue with. For dividend-focused investors, those are the kinds of qualities that build long-term wealth.

Cash Flow Statement

Unum Group generated $1.51 billion in operating cash flow over the trailing twelve months, a healthy increase from the prior year’s $1.2 billion. Free cash flow came in at $1.39 billion, reflecting solid efficiency even after accounting for capital expenditures of $125.7 million. These figures suggest strong operational footing, with consistent cash inflow from core business activities.

On the investing side, outflows totaled $344.4 million, which is significantly lower than prior years, indicating reduced capital commitments or divestitures. Financing activities, however, showed a substantial cash outflow of $1.15 billion, primarily due to aggressive share repurchases nearing $1 billion and modest debt repayment. Despite these outflows, Unum still managed to grow its cash position to $162.8 million, up from $146 million a year ago—a sign of careful capital allocation and solid liquidity management.

Analyst Ratings

📈 Unum Group (UNM) has recently seen a mix of analyst actions reflecting varied perspectives on its performance and outlook. As of now, the stock has a consensus rating of “Moderate Buy” from 14 analysts, comprising 10 “Buy” ratings and 4 “Hold” ratings. The average price target stands at $87.86, suggesting a potential upside from the current trading price.

🔻 In early January, JPMorgan adjusted its stance on Unum Group, downgrading the stock from “Overweight” to “Neutral.” Despite the downgrade, they raised the price target from $74 to $79, indicating expectations of modest appreciation. This change was attributed to a reassessment of the company’s valuation following a period of strong performance.

🔼 On the more bullish side, Raymond James upgraded Unum Group in early March from “Market Perform” to “Strong Buy,” setting a price target of $108. The shift was driven by growing confidence in Unum’s efforts to de-risk its long-term care insurance segment, a move analysts believe could boost profitability and financial resilience going forward.

📊 Piper Sandler also weighed in positively, maintaining an “Overweight” rating while bumping the price target to $92. Their view centered around Unum’s strong fundamentals and the potential for steady growth within its core business lines.

These varying analyst takes reflect the broader view that while Unum may not be a high-flying growth stock, it continues to offer steady performance and upside potential, especially for investors focused on stability and income.

Earnings Report Summary

Unum Group wrapped up the fourth quarter of 2024 with a solid performance that reflects a business steadily firing on multiple cylinders. The numbers weren’t off-the-charts, but they point to a company that knows how to manage its business, keep the financials strong, and deliver value consistently.

Earnings and Revenue

Net income came in at $348.7 million for the quarter, or $1.92 per diluted share, up from $330.6 million, or $1.69 per share, during the same period last year. Adjusted operating income also moved higher, reaching $368.9 million, or $2.03 per share, which is a 13% jump year over year. Total operating revenue climbed 2.5% to hit $3.2 billion, helped along by a boost in both premium income and investment returns.

While earnings growth was clear, the result still landed a bit below what some analysts were expecting. But for long-term investors, especially those focused on dividend strength and financial health, the bigger picture remains encouraging.

Segment Performance

In the Unum U.S. segment, premium income grew 3% to reach $1.7 billion. However, operating income slipped slightly by 2.6%, coming in at $333.2 million. That dip was largely due to lower contributions from all three business lines under this umbrella, a minor setback in an otherwise stable segment.

On the flip side, Unum International posted some stronger results. Premium income jumped 17% to $246.6 million, with operating income growing 4.6% to $37.6 million. The U.K. side of the business pulled much of that weight, with notable increases in both revenue and profitability. It’s a good sign that the company is seeing strong contributions from its global operations.

The Closed Block segment—those legacy insurance policies that Unum continues to manage—also had a bright spot this quarter. Operating income there rose 30% to $27.7 million. On the corporate side, though, the story wasn’t as positive. Operating losses widened to $50.4 million, mainly due to shifting investment income into other lines of the business.

Capital and Outlook

Unum continues to keep its financial house in order. It ended the year with $2 billion in holding company liquidity and a strong risk-based capital ratio around 430%. Book value per share rose sharply to $61.38, up 23% from the year before. The company also returned capital to shareholders through a sizable share repurchase agreement worth $471 million.

Looking to 2025, management expects operating income per share to grow between 8% and 12%, with premium growth in the 4% to 7% range. It’s not flashy guidance, but it shows a company comfortable in its lane—and steadily moving forward.

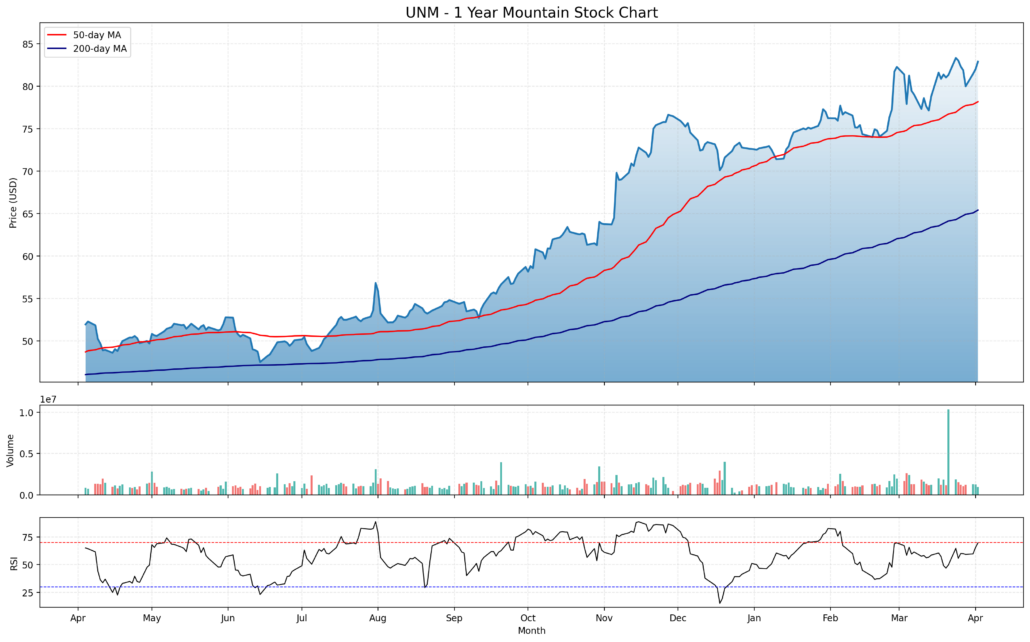

Chart Analysis

Price Trend and Moving Averages

This one-year chart of UNM shows a clear and consistent uptrend, with the stock steadily climbing from the low $50s into the mid-$80s range. What stands out is how smoothly the price has tracked above both the 50-day and 200-day moving averages for the better part of the year. The red 50-day line stayed comfortably above the blue 200-day line throughout, which is a classic sign of strength and momentum. There were no major breakdowns or reversals along the way—just a steady grind higher with occasional pauses.

The most notable acceleration happened between late October and mid-November, where the stock saw a strong breakout and never really gave up its gains. That kind of action usually points to a shift in sentiment or improving fundamentals that caught investor attention.

Volume and Market Activity

Volume remained fairly stable most of the year, with a few noticeable spikes. The largest came near the end of March, potentially reflecting institutional interest or reaction to a news event. Outside of that, trading volume hasn’t shown signs of panic or heavy sell pressure—another signal of underlying confidence.

Even during mild pullbacks, there wasn’t much evidence of volume spikes, which suggests dips were met with calm buying rather than fear-based selling.

Relative Strength Index (RSI)

Looking at the RSI at the bottom of the chart, it spent a good amount of time sitting above 70—the threshold often considered overbought. But rather than sharp corrections following those peaks, the stock mostly consolidated sideways or gently pulled back, indicating strong hands holding the stock.

More recently, the RSI is again hovering around the overbought line, which might imply that the stock is stretched in the short term. However, with no signs of divergence or breakdown, it’s more likely just a reflection of continued strength and consistent buying interest.

Overall Movement and Technical Tone

This is the kind of chart that reflects long-term confidence. It’s not about sudden spikes or speculative bursts—just steady, upward movement supported by positive trends in volume and price structure. Every time the stock paused or dipped, it regained footing quickly and moved higher, creating a staircase pattern that technical traders tend to respect.

It paints a picture of a stock with reliable momentum, a strong technical foundation, and participation from steady hands. That kind of setup tends to support continued strength if broader market conditions remain favorable.

Management Team

At the helm of Unum Group is President and Chief Executive Officer Richard P. McKenney, who has been leading the company since April 2015. With over eight years in this role, McKenney brings a wealth of experience and a steady hand to the organization. Supporting him is Steven A. Zabel, the Executive Vice President and Chief Financial Officer, who plays a crucial role in steering Unum’s financial strategy. The leadership team is further strengthened by Michael Q. Simonds, serving as Executive Vice President and Chief Operating Officer, and Liz Ahmed, the Executive Vice President of People and Communications. Together, this team combines deep industry knowledge with a commitment to fostering a positive corporate culture.

The board of directors is chaired by Kevin T. Kabat, who brings extensive experience from his tenure as CEO of Fifth Third Bancorp. The board comprises individuals from diverse backgrounds, including Susan L. Cross, former Executive Vice President and Global Chief Actuary at XL Group Ltd., and Joseph J. Echevarria, retired CEO of Deloitte LLP. This diversity in leadership ensures a broad range of perspectives, contributing to well-rounded governance and strategic oversight.

Valuation and Stock Performance

Unum Group’s stock has demonstrated a commendable trajectory, reflecting the company’s solid financial health and market confidence. As of April 2, 2025, the stock closed at $82.91, with a market capitalization of approximately $14.66 billion. The price-to-earnings (P/E) ratio stands at 8.76, which is notably lower than the industry average, suggesting that the stock may be undervalued relative to its peers.

In terms of historical performance, Unum’s stock has experienced a steady climb from the low $50s to the mid-$80s over the past year. This upward trend is indicative of strong investor confidence and the company’s consistent ability to meet or exceed market expectations. The 52-week range of $48.38 to $84.48 underscores this growth, highlighting the stock’s resilience and appeal to investors seeking stability and potential appreciation.

Risks and Considerations

While Unum Group presents a compelling investment profile, it is essential to consider the inherent risks associated with the insurance industry. The company has identified a broad range of risk factors in its recent disclosures, with a significant portion categorized under finance and corporate matters. These include financial and accounting risks, as well as challenges related to executing corporate strategy.

Additionally, a meaningful share of the identified risks pertain to production, encompassing aspects such as product development and service delivery. Legal and regulatory risks reflect the complex compliance landscape in which Unum operates. Macro and political factors also present uncertainties, signaling potential exposure to broader economic and geopolitical fluctuations.

Investors should also be mindful of the company’s exposure to long-term care insurance liabilities. In a strategic move to mitigate this risk, Unum entered into a $3.4 billion reinsurance transaction with Fortitude Re in early 2025. This deal is designed to reduce Unum’s exposure to legacy long-term care policies, thereby strengthening its balance sheet and enhancing financial stability.

Final Thoughts

Unum Group stands out as a robust player in the insurance sector, backed by a seasoned management team and a diverse, experienced board of directors. The company’s stock performance and valuation metrics suggest it is well-positioned for continued growth, offering potential value to investors. However, it is important to weigh the associated risks, particularly those inherent to the insurance industry and the company’s specific business lines.

Strategic decisions, such as the recent reinsurance agreement, show that management is proactive in addressing long-term challenges while maintaining a focus on financial strength. Unum’s commitment to steady leadership, disciplined growth, and shareholder value positions it as a company with a long-term view and a track record of navigating the business cycle with care.