Updated April 2025

UnitedHealth Group (UNH) doesn’t always command attention the way tech giants or trendy IPOs do. But for dividend investors with a long view and a taste for reliability, it’s worth a closer look. With nearly half a trillion in market cap and operations spanning insurance, pharmacy services, and data-driven health care, UNH has become a cornerstone in the American healthcare system.

This is a company that’s built for resilience. Through its two main segments—UnitedHealthcare and Optum—it combines the predictability of insurance with the growth potential of healthcare services and tech. That balance gives it a unique position: cash-generative, stable, and still expanding. For those looking to collect dividends without worrying about the next market headline, UnitedHealth might just check all the right boxes.

Recent Events

Lately, the stock has taken a bit of a breather. After peaking above $630, shares have drifted lower and are currently hovering around $523. It’s a decent pullback, driven more by broader market dynamics than anything specific to the company. Defensive sectors like healthcare have seen some rotation out as investors chase more cyclical plays. That’s opened the door for dividend seekers to take another look, especially with the yield inching up.

Behind the scenes, UNH continues to execute. Optum—its high-margin, tech-powered health services business—keeps expanding. It’s not always the flashiest part of the company, but it’s arguably the engine that will power much of UNH’s future. Meanwhile, the core insurance segment remains a rock, driving steady premium income and maintaining tight control on costs.

Management hasn’t skipped a beat on shareholder returns, either. The company paid its latest quarterly dividend in March, extending a long record of uninterrupted payouts.

Key Dividend Metrics

🟢 Forward Dividend Yield: 1.61%

🟡 Trailing 12-Month Yield: 1.56%

🟢 5-Year Average Yield: 1.35%

🟢 Forward Annual Dividend Rate: $8.40 per share

🟡 Payout Ratio: 52.74%

🟢 5-Year Dividend Growth Rate: High single digits

🟢 Dividend History: Steady growth since the 1990s

🟡 Next Ex-Dividend Date: March 10, 2025

🟢 Last Dividend Paid: March 18, 2025

Dividend Overview

The yield might not jump off the page at first glance. A little over 1.6% won’t light up screens for high-yield chasers, but that’s not the point with UnitedHealth. This is a long-term story built around consistency and compounding.

At a payout ratio of just over 52%, the dividend is well-covered by earnings. That kind of discipline allows the company to reinvest in growth, manage debt, and still return meaningful cash to shareholders. And with a forward price-to-earnings multiple around 17.5, the stock isn’t screamingly expensive either—especially when you factor in its steady performance and defensive qualities.

UnitedHealth’s approach to dividends is measured but generous. It’s not a company that throws cash around, but rather one that treats shareholders like long-term partners. The dividend comes like clockwork, and the growth has been strong enough to outpace inflation in recent years.

Dividend Growth and Safety

This is where UNH stands out. While it’s not the highest yielder out there, the pace of growth over the last five years has been impressive. The company has consistently boosted its dividend at a high single-digit to low double-digit clip, year after year. That kind of reliability is what long-term investors dream of—slow and steady gains that snowball over time.

The company’s fundamentals back it up. Free cash flow is strong. Over the last twelve months, UNH has generated more than $24 billion in operating cash flow. Even after reinvesting and handling debt, there’s more than enough left to comfortably support its dividend, which only costs a fraction of that.

Yes, the debt load is sizable—around $82 billion—but it’s balanced by almost $30 billion in cash and a highly predictable revenue stream. The current ratio is below 1.0, which might raise eyebrows elsewhere, but in UnitedHealth’s case, it’s not unusual. The business operates with precision, and its cash conversion is highly efficient. This isn’t a company scrambling for liquidity.

Another quiet signal of strength? Over 90% of its shares are held by institutions. That kind of support speaks volumes. Big money doesn’t stick around unless it believes in the long game—and that includes dividend dependability.

Looking ahead, investors can expect the usual quarterly cadence. Historically, UNH has announced dividend increases in the second quarter, which could mean a raise is on deck. Given the company’s consistent financials and modest payout ratio, there’s plenty of room for another bump without stretching the balance sheet.

For income investors who care about durability, consistency, and quiet strength, UnitedHealth keeps doing what it’s always done: delivering.

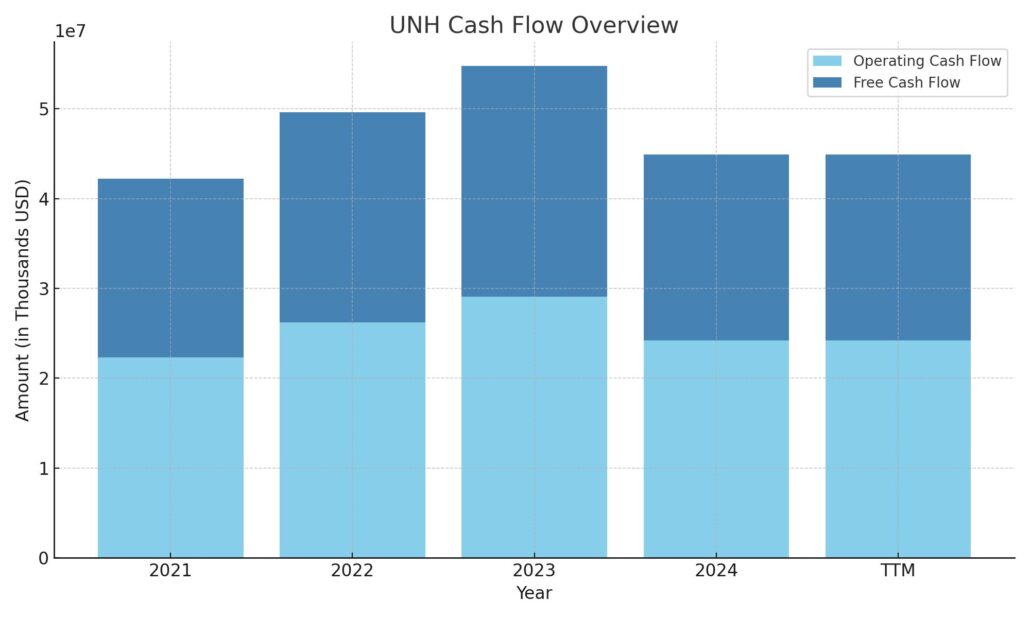

Cash Flow Statement

UnitedHealth Group’s trailing twelve-month (TTM) cash flow performance highlights its strength in generating consistent operating income. The company pulled in $24.2 billion in operating cash flow, which, while lower than last year’s $29.1 billion, still reflects solid earnings quality and strong cash conversion from its core healthcare operations. After accounting for capital expenditures of $3.5 billion, free cash flow landed at $20.7 billion—a healthy figure that easily covers dividend obligations and leaves room for reinvestment or strategic initiatives.

On the investing side, UNH reported an outflow of $20.5 billion, much of which is tied to acquisitions and expansion in its healthcare services segment. Financing cash flow came in at negative $3.5 billion, shaped by a mix of debt issuance and equity buybacks. While the company raised $17.8 billion in new debt, it also repurchased $9 billion in stock and paid down $3 billion in debt, reflecting a balanced capital strategy. The end cash position sits at $25.3 billion, providing a sizable liquidity cushion. Despite the dip in total operating cash from the prior year, the cash flow profile remains fundamentally strong and well-aligned with the company’s steady, disciplined approach to shareholder returns.

Analyst Ratings

🟢 UnitedHealth Group (UNH) has seen varied analyst activity recently, reflecting a mix of perspectives on its valuation and future performance. As of April 2, 2025, the stock is trading at $523.20.

🔻 In January 2025, one major firm adjusted its outlook on UNH, lowering the target price from $694 to $660 while still keeping an “overweight” rating. The downgrade in target was tied to concerns around regulatory developments and their potential drag on earnings, especially in light of increased scrutiny on healthcare reimbursement models and pharmacy benefit managers.

🟢 On the other hand, another well-followed research house reiterated its “overweight” stance with a target price of $700 around the same time. Their analysts highlighted confidence in UnitedHealth’s integrated healthcare platform, which combines insurance and services through its Optum arm, noting that it provides a durable competitive edge in both revenue growth and cost management.

📈 The current consensus price target across 21 analysts sits at $629.32, pointing to a projected upside of about 20% from where shares are trading now. While some near-term caution exists, particularly around political and policy risks, sentiment remains broadly positive on the long-term fundamentals.

Earning Report Summary

Revenue Growth, But Not Without Hiccups

UnitedHealth Group closed out the fourth quarter of 2024 with $100.8 billion in revenue, which is a solid 7% jump from the same time last year. That’s a healthy climb, and most of the momentum came from its Optum business, which continues to be the company’s growth engine. Optum’s revenue grew nearly 10%, thanks to expansion in care delivery and ongoing investments in healthcare services.

Still, the numbers didn’t fully meet Wall Street’s expectations, which had revenue pegged a bit higher. While the miss wasn’t massive, it does show that even a company as consistent as UNH isn’t immune to external pressures.

EPS Surprise and Medical Costs in Focus

On the earnings side, the company delivered $6.81 per share, coming in slightly ahead of estimates. That’s the good news. But on the cost side, there was a bit more to digest. The medical care ratio ticked up to 87.6%, meaning UNH spent more on patient care than expected. That increase raised a few eyebrows and suggests rising costs from higher-than-anticipated healthcare utilization and specialty meds.

Shifts in Enrollment and Guidance for 2025

Another note from the quarter was a dip in Medicaid membership—about 400,000 people. That drop came as pandemic-era enrollment protections ended, and states resumed eligibility checks, trimming the rolls. Even with that, the company stood firm on its guidance for 2025, sticking with a revenue target of $450 to $455 billion and projected earnings between $29.50 and $30.00 per share.

Cash Flow Remains a Strong Point

One of the clear highlights was cash flow. UnitedHealth pulled in $24.2 billion in operating cash for the year, a level that was well above net income. That gives the company room to continue reinvesting, managing debt, and keeping shareholders happy with ongoing dividends.

Market Reaction and Uncertainty Ahead

Despite the decent top and bottom-line performance, the stock took a hit, falling about 5% after the report. The reaction mostly centered around the elevated medical costs and some uncertainty following the recent passing of UnitedHealthcare’s CEO, Brian Thompson. Leadership transitions can make investors a bit uneasy, even when the underlying business remains strong.

In short, UNH continues to deliver, but like most major players in healthcare, it’s facing a few more headwinds than usual.

Chart Analysis

Price Action and Moving Averages

Over the past year, the price action has told an interesting story. After climbing steadily through the summer, the stock peaked in the fall and then ran into some turbulence. That sharp drop in December stands out, likely triggered by either an earnings reaction or broader market volatility. Since then, the price has tried to find its footing, with a modest recovery playing out through March and into April.

The 50-day moving average (red line) rolled over late last year and dipped below the 200-day moving average (blue line) earlier this year. That’s traditionally a bearish signal, often referred to as a “death cross,” but the recent uptrend has brought the price back into that moving average zone. Now, the stock is hovering just below both the 50- and 200-day lines, suggesting a test is underway. A decisive move above those could add some momentum to the recent recovery.

Volume Patterns

Volume hasn’t shown any major spikes recently, though there were a few bursts around earnings and selloffs. For the most part, it’s been steady and not showing any signs of panic or euphoria. That kind of volume behavior supports the idea of the stock trying to base after its pullback, rather than breaking down further.

RSI and Momentum

Looking at the Relative Strength Index (RSI), there was a clear dip into oversold territory earlier this year, followed by a strong bounce. Now, the RSI is approaching the upper end of the range, just below the typical overbought threshold of 70. This suggests the recent upward move might be getting stretched in the short term, but not yet at a point where it’s screaming for a reversal. The momentum is there, but it wouldn’t be surprising to see a bit of consolidation before the next leg higher—if one is coming.

Overall, this chart reflects a stock that went through a significant correction but has been showing signs of stabilization. It’s trading near key technical levels with improving momentum, though some resistance lies directly overhead. Patience here might be rewarded if the recent strength continues and clears those averages with follow-through.

Management Team

UnitedHealth Group has long been recognized for strong, steady leadership guiding it through a complex healthcare landscape. At the top is Andrew Witty, who brings experience from his former role as CEO of GlaxoSmithKline. His background in global healthcare and focus on long-term innovation have played a key role in the company’s strategic direction and operational discipline.

The sudden passing of Brian Thompson, who led the UnitedHealthcare division, was a significant moment for the company. He had been a well-respected leader, and his loss was felt throughout the organization. In response, the company moved swiftly and decisively by promoting Tim Noel, formerly head of the Medicare and Retirement segment. Noel is no stranger to the culture and priorities of the organization, which gives some comfort that the transition will be smooth.

Also central to the leadership team is John Rex, who serves as both President and CFO. Rex has a firm grip on the company’s financial strategy and capital allocation decisions. Together, this leadership group brings a mix of strategic vision and execution strength that continues to serve the business well in a fast-changing healthcare environment.

Valuation and Stock Performance

As of early April 2025, shares of UnitedHealth Group are trading just above $523. Over the past twelve months, the stock has covered some ground, with a high of $630 and a low near $436. That kind of range is typical in today’s market environment, especially for companies navigating the regulatory noise in healthcare.

The company’s trailing P/E sits above 33, but what stands out more is the forward P/E at just under 18. That signals the market expects earnings growth to normalize and improve, which softens the appearance of an otherwise high valuation. It’s also supported by the PEG ratio under 1.0, pointing to growth that’s coming at a reasonable price.

Looking at analyst sentiment, the average price target sits near $629. That implies roughly 20% upside from current levels, which reflects underlying confidence in the business despite recent market volatility. Much of that confidence rests on UnitedHealth’s ability to balance both parts of its business—the traditional insurance side and the rapidly growing services side through Optum. That diversification has historically cushioned the stock during rough patches and supported steady performance over time.

Risks and Considerations

No matter how stable a company appears, risks are part of the equation—and for UnitedHealth, there are several worth watching. One of the biggest is regulatory uncertainty. Whether it’s adjustments to Medicare reimbursements or broader shifts in healthcare law, the business model is tightly linked to how policy plays out in Washington. A major change in regulation could impact revenue streams or operating margins in ways that are hard to predict.

Then there’s the competitive landscape. UnitedHealth operates in a crowded space, where new entrants and established players are always looking to chip away at market share. Staying ahead means continuing to invest in technology, services, and customer engagement. That requires capital, discipline, and sharp execution.

Cybersecurity is another layer of risk. As the company leans further into digital platforms and data-driven care, the stakes get higher. Patient data is sensitive, and a breach could cause reputational harm and result in regulatory action. The company has strong infrastructure in place, but it’s an area where no one can afford to get complacent.

There’s also the matter of overall cost pressure in healthcare. From rising drug prices to increased service utilization, expenses can climb in ways that put strain on margins. When combined with broader economic forces like inflation and interest rates, it becomes clear that even well-run companies like UnitedHealth must remain nimble.

Final Thoughts

UnitedHealth continues to stand out as a force in the healthcare industry. It’s not flashy, but that’s part of its strength—it knows what it does well and focuses on doing it better. The leadership team is experienced and stable, the business is diversified, and the financial profile remains strong.

Recent market action shows some volatility, but not in a way that undercuts the long-term story. This is still a company with meaningful scale, a defensible business model, and a track record of execution. While there are always risks in any healthcare name, UnitedHealth seems well-positioned to manage them while continuing to deliver value to its shareholders.