Updated April 2025

UPS, the global shipping giant we all recognize, is more than just brown trucks and cardboard boxes. It’s a logistics powerhouse with roots that stretch deep into American commerce. Whether it’s e-commerce deliveries to your doorstep or supply chain services for multinational corporations, UPS has built a business model that’s hard to replace.

But the story today isn’t about growth or innovation. It’s about a company that’s evolving into a pure dividend play—one that continues to generate massive cash flow but is also grappling with a very different kind of market pressure.

Recent Events

The past year hasn’t been kind to UPS. Its share price has taken a tumble, down over 28% from its 52-week high. That’s not surprising when you consider what’s been going on under the hood. The e-commerce boom has cooled, freight volumes are softer, and labor costs spiked after the company inked a major contract with the Teamsters union.

Still, UPS posted modest top-line growth in its latest quarter. Revenue ticked up 1.5% year-over-year, and EPS came in at $6.75, a 7.2% increase. Not bad, considering the backdrop. But the broader concern has been profitability. Operating margins are thinner, and investors are starting to ask tougher questions about whether the business can maintain its cash-generating mojo.

One area where pressure is building: the balance sheet. Total debt has climbed to $25.65 billion, far outweighing the company’s $6.32 billion cash balance. The debt-to-equity ratio now sits above 153%, and while not catastrophic, it certainly adds to the complexity when you’re also paying out nearly every dime of earnings in dividends.

Despite those challenges, UPS remains a reliable cash flow generator. Over the past twelve months, it pumped out more than $10 billion in operating cash flow and just under $4.8 billion in levered free cash flow. So while the outlook may be murky, the check to shareholders hasn’t bounced—and doesn’t seem poised to anytime soon.

Key Dividend Metrics

📈 Forward Dividend Yield: 6.00%

💵 Forward Annual Dividend: $6.56 per share

📊 Payout Ratio: 96.6%

📆 Last Dividend Paid: March 6, 2025

🔁 5-Year Average Yield: 3.40%

📉 Share Price Decline (1Y): -28%

💼 Cash Flow Coverage (FCF/Dividend): Barely adequate but still holding

Dividend Overview

At this point, UPS isn’t just paying a dividend—it’s leaning into it. The forward yield has swelled to 6%, a level that towers over its historical average. That’s not just a result of a higher payout; it’s also because the stock has slipped so far. For dividend-focused investors, this makes UPS a compelling yield anchor.

Currently, the company is shelling out $6.56 per share annually. And it hasn’t backed off that commitment, even as margins are squeezed and the economic backdrop remains uncertain. Management seems locked in on keeping shareholders whole.

That said, the payout ratio tells a more nuanced story. At nearly 97%, UPS is using almost all its earnings to fund the dividend. That’s fine for now—but it leaves little room for hiccups. Especially for a capital-heavy business like this, with trucks to replace, systems to upgrade, and a global network to maintain.

Still, there’s comfort in the consistency. UPS has long been shareholder-friendly, and that hasn’t changed. Institutional ownership remains high—over 70% of shares are in big investors’ hands—which tends to keep management disciplined about preserving the dividend, even when times get tough.

Dividend Growth and Safety

UPS has been a dependable dividend grower for years. While it’s no longer increasing the payout in dramatic fashion, the checks have continued to grow steadily. But given today’s financial setup, growth could take a breather. The last bump in the dividend was modest, and with so much of its earnings tied up in distributions, there’s not a lot of headroom left.

Digging into the free cash flow numbers adds more color. Over the last year, UPS generated about $4.79 billion in levered free cash flow—right around what it paid out in dividends. That margin is thin. Not dangerous, but not especially comforting either. Any drop in cash flow or unexpected expense could tip the balance.

What UPS does have going for it is scale. It’s been through downturns, recessions, and disruptions before. This isn’t a new playbook—it’s a well-tested one. The company knows how to hunker down when necessary. For now, the dividend looks like it’s staying put.

At a forward P/E of under 14, the stock isn’t being priced like a growth machine. It’s being treated like a high-yield bond proxy. And in many ways, that’s what it has become—a low-volatility name with a big yield that’s more about income than capital appreciation.

The catch? The business model has to keep delivering just enough to support that yield. No frills, no drama—just consistent performance. If UPS can do that, even flat growth may be enough to satisfy its base of dividend investors.

UPS may no longer be riding a wave of e-commerce tailwinds or international expansion stories. But for investors focused on income, the story has become simpler—and sometimes, simpler is better.

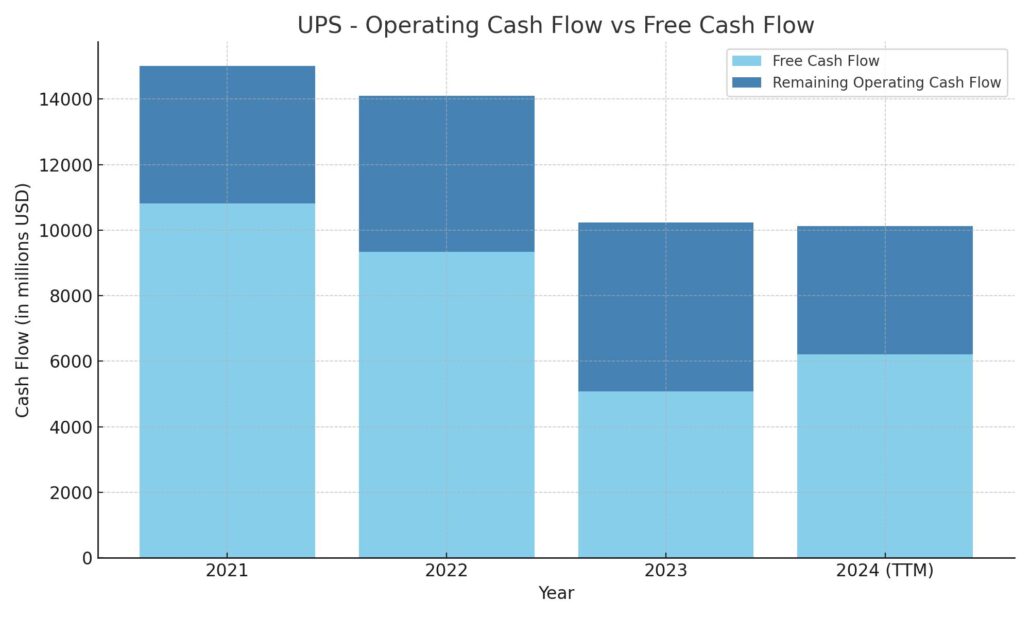

Cash Flow Statement

UPS generated $10.1 billion in operating cash flow over the trailing twelve months, maintaining a solid level of internal cash generation, though this marks a continued decline from its 2021 peak of $15 billion. Despite softer top-line growth and margin pressure, the business continues to produce enough operating income to support its capital allocation priorities, which include dividend payments and modest share repurchases. Free cash flow stood at $6.2 billion for the same period, showing that even with reduced profitability, UPS retains meaningful flexibility with its cash.

On the investment side, capital expenditures totaled nearly $3.9 billion, a reduction from prior years, pointing to more selective or possibly delayed infrastructure spending. Financing activities saw a net outflow of $6.85 billion, largely due to debt repayments and continued capital returns to shareholders. UPS ended the period with a cash balance of just over $6.1 billion—almost double where it was at the close of 2023. While overall cash flow strength is no longer at pandemic-era highs, the company is managing its capital carefully, ensuring it remains able to support a generous dividend while navigating a more complex operating landscape.

Analyst Ratings

📉 United Parcel Service (UPS) has recently experienced a mix of analyst activity, highlighting differing views on where the stock is headed. Currently, the consensus among 25 analysts leans toward a “Moderate Buy,” with 14 buy ratings, 9 holds, and 2 sells. The average price target is $135.83, pointing to a potential upside of around 23% from its current share price of about $110.

🚩 In late March, one of the more cautious calls came from Barclays, which maintained its “underweight” rating and trimmed its price target from $100 to $90. The downgrade was primarily driven by mounting concerns around softening package volumes and intensifying competition in the logistics space, both of which could weigh on near-term profitability.

🚀 On the other side of the fence, BMO Capital recently reaffirmed its bullish stance. While the firm did nudge its price target lower from $140 to $130, it stuck with its “outperform” rating. The update acknowledges current operational challenges but remains confident in UPS’s longer-term strategy, particularly its focus on driving efficiency and strengthening its network across high-margin areas.

🎯 The range in analyst sentiment reflects the balancing act UPS is navigating—short-term headwinds versus longer-term execution and cash flow consistency.

Earnings Report Summary

UPS recently reported its earnings for the fourth quarter of 2024, and while the numbers weren’t earth-shattering, they did show some resilience in a tougher environment. Revenue came in at $25.3 billion, up 1.5% from the same quarter last year. That slight gain was mostly thanks to a stronger showing in the U.S. Domestic Package segment and some surprising strength overseas. Domestic saw a small lift from better revenue per package, while international deliveries actually picked up in volume.

Profit Performance

Operating profit hit $2.9 billion for the quarter, which is a decent step up from last year. If you strip out a few one-time items, that number climbs to $3.1 billion. Margins also held up well—an 11.6% operating margin, or 12.3% on an adjusted basis. On the earnings front, UPS posted $2.01 per share, but that number rises to $2.75 when adjusted, which is about an 11% improvement from the year before. It’s a sign that despite cost pressures, UPS is still managing to squeeze out solid profitability.

Segment Breakdown

One part of the business that took a hit was Supply Chain Solutions. Revenue there dropped over 9%, mostly because the company offloaded Coyote Logistics. That sale pulled numbers down a bit, although growth in freight forwarding helped soften the blow. Margins in this segment were slimmer, but still in positive territory.

Full-Year View and Strategy Updates

Looking at the year as a whole, UPS pulled in $91.1 billion in revenue. Full-year operating profit was $8.5 billion—or $8.9 billion when adjusted—putting the operating margin just under 10%. Full-year earnings per share came in at $6.75, or $7.72 on an adjusted basis. The company also generated $10.1 billion in operating cash flow, which helped fund $5.9 billion in returns to shareholders through dividends and buybacks.

UPS also shared a few strategic updates. One major move was cutting back volume from its largest customer by more than half by late 2026. That’s a bold decision, but it reflects a push to improve margins and shift toward more profitable business. Plus, as of January 2025, UPS brought all SurePost volume back in-house. These steps are part of a broader effort to streamline operations and focus on efficiency.

Chart Analysis

Price Action and Moving Averages

Over the past year, the stock has shown a clear downtrend. Price has steadily declined from the $140–$150 range down to just above $110, with several lower highs along the way. What stands out is the position of the 50-day moving average (red line) consistently trailing below the 200-day moving average (blue line), confirming the persistent bearish pressure. Even the brief rallies through summer and into the fall didn’t push the price above those key trend indicators in a sustained way.

More recently, the stock attempted to climb back in February and March, but that rally was quickly sold into. Price has now broken below the February low, putting in a fresh low for the year. This type of breakdown doesn’t suggest any immediate reversal is underway.

Volume Behavior

Volume remained relatively stable for most of the year, but there were notable spikes in late January and mid-March. These bursts of activity typically coincide with earnings events or major news. Interestingly, those spikes were followed by sharp price drops, suggesting selling volume overwhelmed any short-lived optimism. Recent volume trends look more cautious, which may indicate market participants are waiting for a clearer signal.

Relative Strength Index (RSI)

The RSI has been hovering mostly in the neutral to oversold range. It approached overbought levels a couple of times in February and early March during short-lived rallies but quickly dropped back below 50. More recently, RSI has stayed closer to the 30 level, signaling weak momentum. It hasn’t crossed into extreme oversold territory consistently, but it also hasn’t shown any strong push back toward 60 or above, which would indicate recovery strength.

Final Takeaway

This chart reflects a stock under continued selling pressure. While there are occasional rallies, they’ve failed to change the overall trend. Price remains below both major moving averages, volume hasn’t confirmed any reversal, and RSI momentum is weak. For now, the technical picture leans more toward caution, with no clear signal of a sustained turnaround in place.

Management Team

At the head of United Parcel Service is CEO Carol B. Tomé, who stepped into the role in mid-2020. She came with a strong background in finance, having served as CFO at The Home Depot. Her approach at UPS has been focused and deliberate—centered on streamlining operations rather than expanding for the sake of size. This “better, not bigger” philosophy has guided many of the company’s recent decisions.

Alongside Tomé is a leadership team with deep operational experience. Norman Brothers leads the legal and compliance functions, keeping regulatory risks in check. Nando Cesarone oversees U.S. operations, drawing from years of logistics expertise. Brian Dykes, who was appointed CFO in 2024, is now responsible for managing the financial strategy during a more complex period for the company. On the people side, Darrell Ford is focused on HR transformation, and Kate Gutmann heads the company’s international and healthcare logistics efforts. Digital and tech innovation is being driven by Bala Subramanian, while Matt Guffey manages strategy and commercial operations. This team is steering UPS through a shifting landscape with a mix of financial discipline and long-range vision.

Valuation and Stock Performance

UPS stock has had a bumpy ride over the past year. As of early April 2025, shares closed just over $110, which is down significantly from the 52-week high of more than $150. That drop represents over 28 percent in value lost, driven by a mix of softer package volume trends, macro headwinds, and cautious investor sentiment.

The company is now valued at roughly $92 billion in market cap, with enterprise value close to $112 billion. Trailing twelve-month earnings give UPS a P/E ratio around 16, while the forward-looking multiple is closer to 14. Those figures don’t scream overvaluation—they suggest the market is pricing in modest growth, tempered by recent operational and competitive challenges.

When compared to peers, UPS still holds up as a solid, cash-flow-generating business, but the stock’s performance tells the story of recalibrated expectations. The average analyst price target sits near $136, which reflects some optimism that the worst may already be baked in. It’s clear that for now, investors are more focused on operational execution than on chasing growth.

Risks and Considerations

UPS faces a few real challenges that can’t be overlooked. One of the biggest is competition. It’s not just FedEx anymore—regional delivery firms, gig-economy carriers, and even Amazon’s own growing logistics footprint are changing the rules of engagement. That shift puts pressure on pricing and margins, especially in lower-volume environments.

Labor costs are also a major concern. UPS runs a heavily unionized workforce, and contract renewals or disputes can quickly ripple through the business. The recent labor deal brought stability, but it also brought higher costs that are going to stick around for the foreseeable future.

On top of that, UPS is shifting away from one of its largest clients by cutting volume commitments by more than 50 percent over the next year and a half. It’s a bold move that may help long-term margins, but in the short term, it’s going to leave a revenue gap that needs to be filled.

Add to that the usual macro variables—like fuel costs, global economic slowdowns, or regulatory changes—and it’s clear that the road ahead will require tight management and a little flexibility.

Final Thoughts

UPS is not in a crisis, but it’s also not coasting. The company is in the middle of a thoughtful transition, trying to evolve its business model while staying true to its roots as a logistics powerhouse. The leadership team is experienced and appears to have a clear direction, but they’re navigating a market that’s shifting in real time.

The stock’s current valuation reflects that push and pull—investors see the value, but they’re also waiting for clearer signs of growth or operational upside. For those who are drawn to steady businesses with strong cash generation, UPS still fits the bill. But it’s not a simple story. It’s one of balance, trade-offs, and long-term discipline. How well UPS executes on its strategy in the coming quarters will go a long way in determining whether the market begins to reward it with a higher premium—or continues to tread cautiously.