Updated April 2025

Union Pacific has long been one of those cornerstone companies in the American industrial landscape. If you’ve ever looked out a car window and seen a train cutting across the countryside, there’s a decent chance it was operated by Union Pacific. The company’s rail network spans 23 states in the western two-thirds of the U.S., and it moves everything from agriculture and chemicals to consumer goods and coal.

It’s not flashy, and it doesn’t need to be. Union Pacific’s business is rooted in consistency. For income-focused investors, this is a name that’s known more for quiet reliability than headline-grabbing news. But when it comes to dividends, that kind of consistency is exactly what you want.

UNP has been around for nearly 170 years. It’s weathered wars, recessions, pandemics, and everything in between. Through it all, the company has kept the trains running—and the dividends flowing.

Recent Events

Over the past year, Union Pacific’s story has been a bit of a mixed bag. Revenue has softened slightly, with a year-over-year decline of just under one percent. Not ideal, but also not shocking considering the broader freight environment. Some segments, like intermodal shipping, have seen a bit of a slowdown, while others—think bulk goods and industrial freight—have stayed more stable.

Despite that, margins remain strong. Operating margin sits above 41%, and net margin is hovering near 28%. That’s impressive, especially in a capital-heavy business like rail. What really jumps off the page, though, is return on equity—above 42%. This company knows how to squeeze real value from its assets.

Earnings per share have continued to grow, up almost 7% from the prior year, and that strength is helping to support shareholder returns. The most recent quarter didn’t include any major dividend announcements, but the company’s financial footing remains solid. They’ve been consistent, and there’s no signal they’re planning to shift gears.

Key Dividend Metrics

📈 Forward Yield: 2.26%

💵 Forward Annual Dividend Rate: $5.36

📅 Most Recent Dividend Paid: March 31, 2025

🔁 Dividend Frequency: Quarterly

📊 Payout Ratio: 47.61%

📆 5-Year Average Yield: 2.14%

⚖️ Dividend Growth Streak: 16 years

📉 Dividend Cut Risk: Low

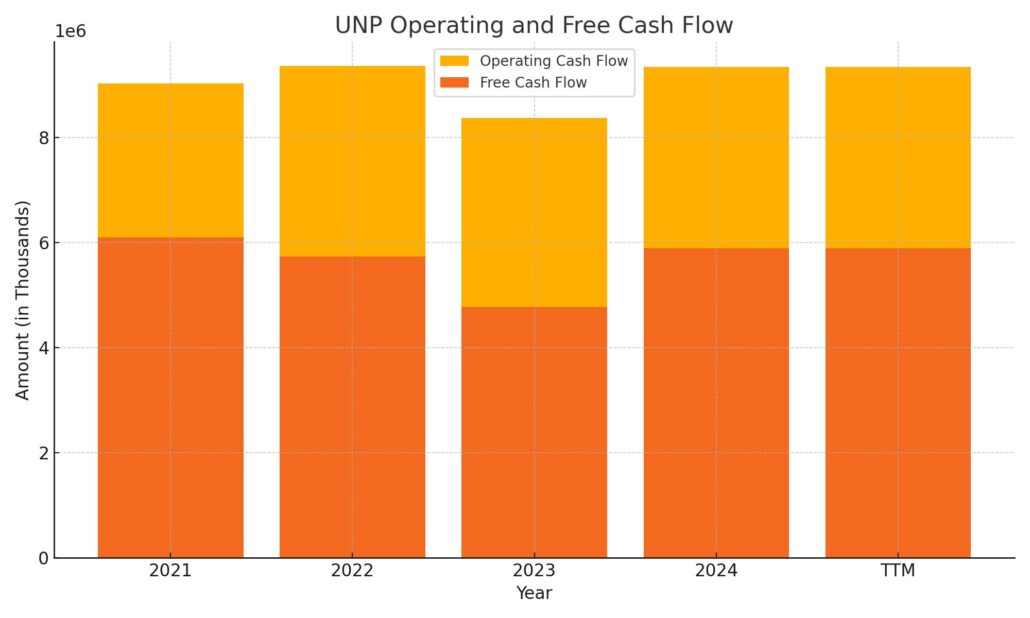

💪 Free Cash Flow (TTM): $4.62 billion

💰 Operating Cash Flow (TTM): $9.35 billion

Dividend Overview

At a glance, Union Pacific’s dividend yield sits at 2.26%. That’s not going to knock anyone’s socks off, but it’s a dependable yield that’s held up over time. It also edges out the company’s five-year average yield of 2.14%, which suggests the stock is offering decent value for income-focused investors right now.

The dividend payout ratio is under 50%, which is a good sign. It shows the company isn’t overcommitting itself and still has room to reinvest in operations and maintain financial flexibility. They’re striking a smart balance between rewarding shareholders and keeping their business running at full steam.

And that dividend schedule? As reliable as their freight service. The most recent payment hit accounts at the end of March, and the rhythm is well established. Investors can count on consistent quarterly payouts.

Union Pacific also doesn’t overreach. It doesn’t rely on huge buyback programs to keep shareholders happy. Instead, it just keeps delivering a steady dividend, quarter after quarter.

Dividend Growth and Safety

This is where Union Pacific really starts to show its long-term value. The company has been raising its dividend for 16 straight years, and there’s a clear commitment to continuing that trend. Over the last decade, the dividend has grown meaningfully—more than quadrupling in that time.

Recent increases have been a bit more measured, landing in the mid-to-high single-digit range. But even at that pace, the compound effect is real. That’s especially valuable for anyone reinvesting dividends or building an income stream for retirement.

The safety of this dividend is another strong point. With over $9 billion in operating cash flow and more than $4.6 billion in free cash flow, Union Pacific has plenty of cushion. Even with a debt load north of $32 billion, there’s no immediate concern. The company generates more than enough earnings to comfortably cover interest payments and maintain the dividend.

The current ratio is a bit below 1, but that’s fairly typical for companies like this. The real focus is on cash flow, and Union Pacific continues to deliver there.

Economic cycles do hit railroads—freight volumes aren’t immune to a slowing economy. But UNP has proven over time that it can navigate those ups and downs without missing a beat on its dividend. The management team stays conservative with capital allocation. There’s no drama, just steady performance and thoughtful stewardship.

So while the stock itself might not be the most talked-about name on the market, for income investors looking for stability, Union Pacific keeps rolling along—delivering income today and planting the seeds for growth tomorrow.

Cash Flow Statement

Union Pacific generated $9.35 billion in operating cash flow over the trailing twelve months, staying consistent with previous years and reflecting the company’s ability to convert its earnings into strong, dependable cash flow. Free cash flow came in at $5.89 billion, a notable increase from $4.77 billion the prior year, thanks to slightly lower capital expenditures and stable operating performance. This solid cash generation supports the company’s dividend payments and infrastructure investments without straining the balance sheet.

On the financing side, Union Pacific saw a net outflow of $6.07 billion. The company issued $800 million in new debt but repaid $2.23 billion, and returned another $1.51 billion through share repurchases. While share buybacks were more modest compared to prior years, they still reflect management’s ongoing commitment to capital returns. Despite continued investment outflows and steady debt servicing, the company maintained a stable end cash position of just over $1 billion.

Analyst Ratings

📉 Recently, Union Pacific Corporation (UNP) saw a shift in sentiment from UBS, where the analyst dropped the price target from $255 to $245 while keeping a Neutral rating. The reasoning behind the move centers around growing caution in the industrial freight space. Concerns are rising that inflationary pressures, particularly in labor and fuel, could outweigh gains made through pricing and mix. UBS also trimmed their 2025 earnings per share forecast from $11.80 to $11.60, reflecting those margin worries.

📈 On the more optimistic side, BMO Capital nudged its target slightly lower to $270 from $277 but kept an Outperform rating. They still see strength in Union Pacific’s underlying business model and operational improvements, though acknowledge a few near-term macro headwinds. Likewise, RBC Capital revised its price target to $261 from $276, also holding on to its Outperform rating. These slight reductions suggest analysts are adjusting for current conditions rather than losing confidence.

🎯 As of early April 2025, the average price target among analysts sits around $271.36. There’s a broad range, with estimates as high as $486 and as low as $200. Overall, sentiment remains positive, with the majority leaning toward a Buy rating on the stock.

Earnings Report Summary

Strong Bottom Line Despite Mixed Revenue

Union Pacific’s latest earnings gave investors something to feel good about. In the fourth quarter of 2024, the company posted net income of $1.8 billion, or $2.91 per diluted share. That’s a healthy 7% bump from the same time last year. Part of that included a $40 million labor expense tied to a new crew staffing agreement—so the earnings growth came even with added labor costs on the books.

Revenue for the quarter landed at $6.1 billion, which was just a hair under where it stood a year ago, slipping 1%. The decline mostly came from lower fuel surcharge revenue and a less favorable mix of business. Still, they managed to move more freight overall. Carload volume rose 5%, and they were able to squeeze more out of pricing, which helped cushion the top line.

Operational Efficiency Making a Mark

Efficiency continues to be a bright spot. Union Pacific improved its operating ratio to 58.7%, which is 220 basis points better than the same quarter last year. That’s a big deal for a company this size. And that improvement includes the cost of the new labor agreement, which had a 70 basis point impact on its own. So even with those new expenses, the business became leaner and more productive.

The railroad also saw slight gains in freight car velocity, moving cars 1% faster to hit 219 miles per day. Worker productivity improved too, up 6% to 1,118 car miles per employee. These kinds of gains don’t grab headlines, but they quietly drive long-term profitability.

Full-Year Snapshot and Looking Ahead

For all of 2024, Union Pacific reported $6.7 billion in net income and $11.09 in earnings per share—both up about 6% from 2023. The full-year operating ratio came in at 59.9%, showing the company’s consistent progress in controlling costs.

Looking to the future, management didn’t sound overly bullish, but they weren’t waving any red flags either. They’re eyeing continued earnings growth in the high-single to low-double-digit range, depending on how things shake out with the broader economy. Coal demand and other macro factors remain wildcards, but Union Pacific is sticking to its strategy and banking on improved service and cost discipline to keep things on track.

Chart Analysis

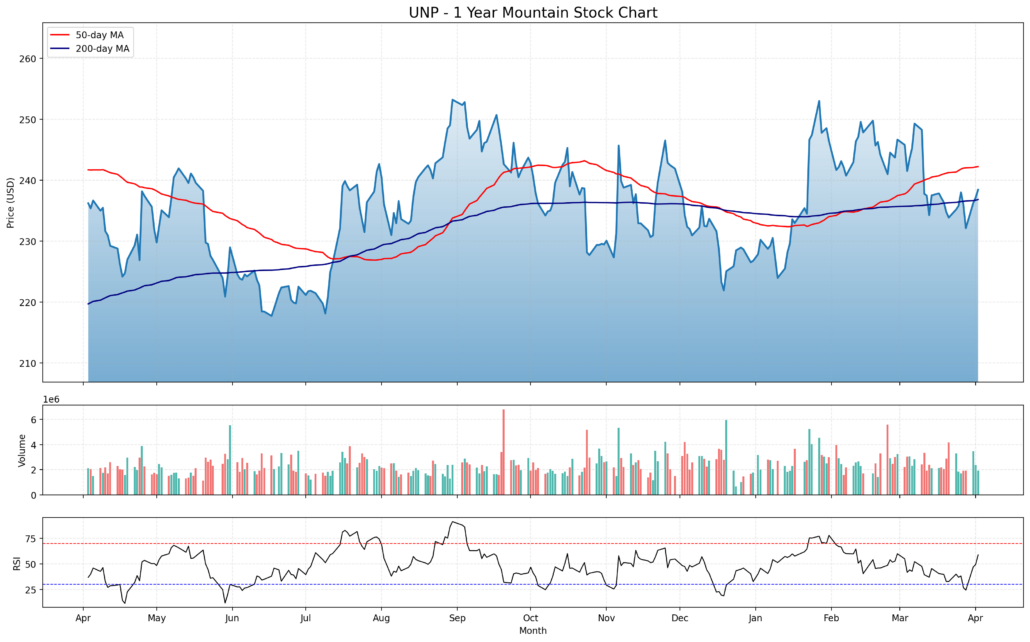

Price Action and Trend Overview

The price chart over the past year paints a picture of a stock that’s been grinding through a wide sideways range. After a soft start last spring, the price hit a bottom near $215 in June before bouncing sharply into the $250s by late summer. From there, it struggled to build momentum, testing the $240–$250 zone multiple times without much follow-through.

Recently, price has been hugging the 200-day moving average, which has flattened out—signaling a lack of strong trend direction. The 50-day moving average, after curling downward earlier this year, has begun turning back up. That crossover and shift could be worth watching, as it may hint at early strength trying to emerge.

Volume Behavior

Looking at the volume section, there’s no dramatic spike or trend that suggests major accumulation or distribution. Volume has stayed relatively steady, with the occasional uptick during selloffs and rebounds, especially around June, October, and late February. The lack of volume surges during price rallies tells us this hasn’t been a period of aggressive buying—but it also doesn’t reflect heavy selling pressure.

The balance of volume doesn’t scream urgency. That supports the idea this stock is in more of a holding pattern, not being chased up or dumped out with conviction.

RSI and Momentum

RSI has stayed mostly between 35 and 65 throughout the year, occasionally poking into overbought territory but rarely diving too far into oversold. Right now, it’s bouncing higher from a recent dip, landing just below 60. That momentum shift may reflect renewed buying interest, but it’s still far from euphoric.

It’s worth noting that RSI has shown this pattern a few times—dipping, then bouncing, without setting off major reversal signals. That kind of rhythm fits with the broader picture: a stock that’s consolidating, not sprinting.

Overall Takeaway

This chart reflects a company whose stock has been trading sideways for much of the year, with some mild technical improvement developing in the near term. The price has held key support levels and hasn’t broken down significantly. The moving averages are converging, and RSI is recovering—both of which suggest the potential for more stable footing ahead. This isn’t a high-volatility name, and the price action reflects that: steady, range-bound, and waiting for a stronger catalyst.

Management Team

Union Pacific’s leadership team blends operational expertise with a deep understanding of the industry’s long-term challenges. Jim Vena, who stepped into the CEO role in August 2023, brought with him a long track record in freight rail. Having served previously as Union Pacific’s Chief Operating Officer, he’s familiar with the company’s network and its operational needs. His return marked a shift toward sharpening efficiency and execution.

Beth Whited now serves as President. She’s spent her entire career with Union Pacific in various roles, especially within sales and marketing. Her leadership brings a strong commercial focus to the executive team, with a deep grasp of customer needs and demand trends across industries.

On the financial side, Jennifer Hamann continues to serve as CFO, a role she’s held since early 2020. Under her watch, Union Pacific has maintained its solid credit profile while balancing shareholder returns with infrastructure investment. She’s known for her disciplined approach to capital deployment.

Eric Gehringer leads day-to-day operations as Executive Vice President of Operations. He’s been key to pushing improvements in train velocity and service reliability. His work reflects the company’s ongoing efforts to enhance network performance while keeping safety at the forefront.

Valuation and Stock Performance

Union Pacific stock is currently trading around $238, with a trailing P/E ratio of just over 21 and a forward P/E under 20. This valuation puts it right in line with other blue-chip industrial names. It’s not cheap, but for a company of this caliber, the market seems to be pricing in stable cash flows and modest growth.

Over the past five years, the stock has returned nearly 85% in total, which includes price appreciation and dividends. That performance has come with lower volatility than the broader market, which says something about the strength of its business model. Year-to-date performance is slightly positive, even as other transportation names have faced headwinds tied to shifting demand.

The stock has traded in a fairly tight range over the past 12 months, with dips being met by support near the 200-day moving average. Momentum hasn’t been explosive, but long-term holders have been rewarded with a steady blend of yield and stability.

Risks and Considerations

Union Pacific isn’t immune to risk. Like any rail operator, its fortunes are tied closely to the health of the broader economy. If industrial production slows or consumer demand weakens, shipping volumes could fall. That would put pressure on both pricing and margins.

Regulatory risk is another constant in this industry. Railroads face strict oversight when it comes to safety, labor, and environmental standards. Any tightening of these regulations could raise costs or limit operational flexibility.

There’s also the risk of accidents or service disruptions. A single derailment or safety issue can have ripple effects across the entire network, not to mention potential reputational damage. Union Pacific has had its share of incidents, and while it continues to invest in safety technology and training, the risk is never zero.

Another layer of risk comes from environmental factors. Railroads are still heavy users of diesel fuel, and growing environmental pressure could lead to costly transitions or investments in alternative energy solutions. The company has made progress in reducing emissions intensity, but the road to full sustainability is long and expensive.

Final Thoughts

Union Pacific has built a reputation on reliability. The company doesn’t chase trends or overextend itself. It knows what it is—a major player in freight transportation with a focus on efficiency, long-term returns, and steady shareholder value.

The management team is experienced and seems aligned with long-term strategy. Financially, the business generates strong free cash flow, supports a consistent dividend, and maintains a balanced capital allocation model. Even during weaker demand cycles, Union Pacific tends to maintain its footing.

There are risks here, from economic sensitivity to regulatory pressures, but they’re not new. The company has navigated them before and appears positioned to do so again. For those looking for steady performance from a legacy operator, Union Pacific continues to offer a business model built for endurance.